NOTE: An updated version of this analysis is here.

While federal protections prevent most people from paying out-of-pocket for COVID-19 testing, patients may face substantial costs if hospitalized for treatment because there are no provisions that require private insurance plans to waive cost-sharing for COVID-19 treatment. A previous KFF analysis estimated that average out-of-pocket costs associated with an inpatient admission for COVID-19 treatment for patients with large employer coverage could exceed $1,300, though the amounts could be much higher for patients who are severely ill or use out-of-network services. People insured through the individual and small group markets also may face even higher levels of cost-sharing because these plans tend to have higher deductibles than employer-based plans.

Many private insurers have taken steps in recent months to mitigate out-of-pocket costs during the pandemic. For example, an earlier KFF brief looked at how many people were impacted by insurers waiving cost-sharing for telemedicine. Insurers have experienced lower-than-expected claims costs during the pandemic, as enrollees have delayed or forgone elective and less-urgent care. This has left insurers relatively profitable, which means they may owe very large rebates to consumers next year, under the Affordable Care Act’s Medical Loss Ratio (MLR) rule. By offering cost-sharing waivers insurers can essentially increase their claims costs relative to their premiums and make it more likely that they meet the MLR threshold. However, given their current financial trajectory and recent years of high profits, insurers may still owe large rebates next year even if they do take measures to lower their MLR now.

In this brief, we estimate the number of enrollees whose insurer has waived cost-sharing – out-of-pocket costs including coinsurance, copayments, and deductibles – for COVID-19 treatment. We also estimate the number of enrollees whose insurer is offering various forms of premium payment relief. To do so, we reviewed a summary of private insurers’ responses to the pandemic compiled by America’s Health Insurance Plans (AHIP). We systematically collected data from this summary and merged it onto enrollment data from Mark Farrah Associates TM in order to estimate how many individual and fully-insured group market enrollees are in plans that have waived cost-sharing for COVID-19 treatment or are offering some form of premium relief.

Importantly, our estimates do not include the substantial portion (61%) of the group market enrolled in self-insured plans through their employers. These plans are established and funded by an employer and are not always subject to federal regulation. As such, the benefit designs of these plans, including the services that they opt to cover and any associated cost-sharing, are left to the discretion of the employer. There is no source of comprehensive data on the prevalence of these policies and, therefore, they are not included in this analysis.

Related Content:

Cost-sharing waivers for COVID-19 treatment

Federal legislation enacted in March requires that all private insurance plans, including self-funded plans, cover the entire cost associated with approved COVID-19 tests so long as the test is deemed medically appropriate. However, there are no provisions that require private insurance plans to waive cost-sharing for COVID-19 treatment. Only five states (MA, NM, ID, MI, MN) and D.C. require insurers to waive out-of-pocket treatment costs for their fully-insured plan enrollees, though many insurers have voluntarily opted to waive out-of-pocket costs for enrollees who require COVID-19-related treatment.

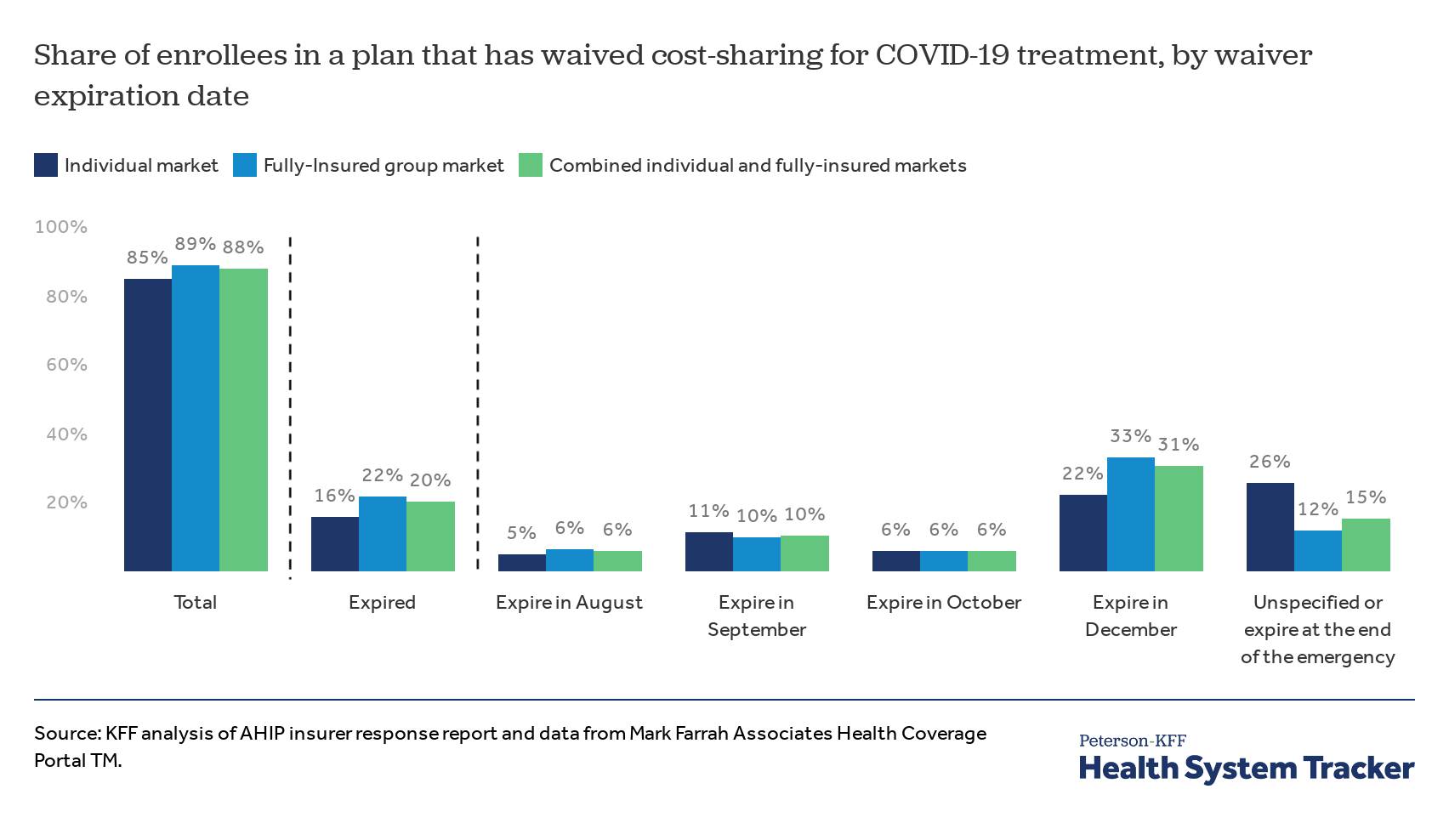

A substantial majority of individual and fully-insured group market enrollees are in plans that have waived cost-sharing for COVID-19 treatment, though some waivers are expiring

Across all individual and fully-insured group plans, 88% of enrollees are in a plan that has at some point during the pandemic waived out-of-pocket costs for COVID-19 treatment. However, 20% of enrollees in these markets are in plans where that waiver has already expired and another 16% are in plans where it is currently set to expire by the end of September, leaving just 52% of enrollees with COVID-19 treatment cost-sharing waivers in October and beyond. (Some plans have extended expiration dates already, and others may do so as their expiration date approaches). About a third (31%) of enrollees in the individual and fully-insured group markets are in plans that have waived cost-sharing on COVID-19 treatment for the remainder of the year, and another 15% are in plans where the expiration date of the waiver is unspecified or tied to the end of the designated public health emergency. Notably, most of these waivers only apply to COVID-19 treatment received from in-network providers or facilities and consumers who are treated out-of-network may be forced to pay the entire cost of their treatment.

Included in these estimates are enrollees who live in one of the five states or the District of Columbia that currently mandate all state-regulated insurers to waive cost-sharing for COVID-19 treatment, although the expiration dates of these mandates vary by state. Combined, these states account for 7% of the individual market and 9% of the fully-insured group market. Roughly 80% of enrollees in either market are in a plan that voluntarily waived cost-sharing for COVID-19 treatment at some point during the pandemic.

Premium relief

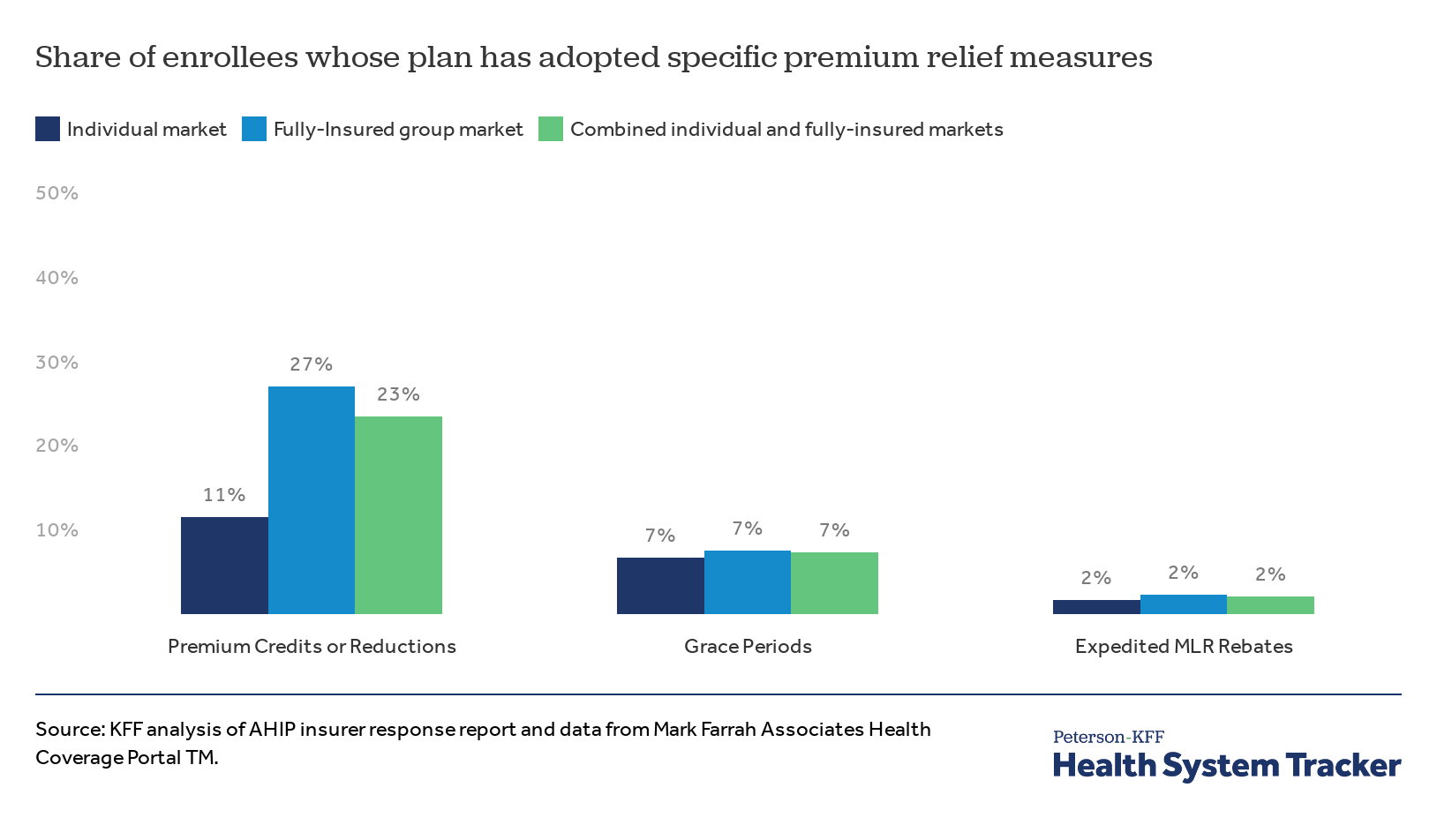

Insurance companies are thus far quite profitable due to a rapid decline in overall healthcare utilization and spending since the start of the pandemic. Insurers are generally not allowed to reduce premiums owed in the middle of a plan year; however, CMS recently released guidance allowing individual and small-group insurers to temporarily offer premiums credits to enrollees. Now, 11% of the individual market enrollees and 27% of fully-insured group market enrollees are in plans offering some form of premium credit or reduction.

Most individual market or fully-insured enrollees had not benefited from premium relief measures as of late July

Insurers may also provide grace periods where individuals who do not pay their premiums on time do not face immediate cancellation of their policy. About 7% of enrollees in both markets are receiving grace periods to pay their premiums. A vast majority of these affected enrollees (representing 6 of the 7 percentage points) live in one of the three states that currently require grace periods for premium payments, whereas plans that have voluntarily instituted grace periods represent only 1 out of 7 percentage points.

The Affordable Care Act (ACA) requires individual and small-group insurers to spend at least 80% of their income from premium payments on health services, calculated on a three-year rolling average basis. If health insurers do not reach this threshold, referred to as the Medical Loss Ratio (MLR), they must reimburse their policy holders through rebates in the following plan year. Typically, rebates are not sent out until the fall after the plan year from which they are calculated, but CMS released guidance in June that allows health plans to “prepay” rebates to policy holders in order to help reduce the costs of premiums, and further clarified in an August 4th memo that the rebates can be in the form of premium credits or reductions. By the end of July, 2% of individual and fully-insured group market enrollees were in plans that had expedited rebate payments to qualifying enrollees.

Discussion

Motivated by higher-than-expected profits and some state requirements, many insurers have acted to offer financial relief to their enrollees, primarily through reduced COVID-19 treatment costs and less commonly through forms of premium relief and waivers on out-of-pocket costs for telehealth use. That said, many of these cost-sharing waivers have either expired or soon will, meaning more privately insured people will be exposed to high out-of-pocket costs associated with COVID-related treatment and hospitalization. Consumers who seek treatment for COVID-19 from out-of-network providers are also likely to face high costs for care, since most of these waivers only cover treatment from in-network providers. Also, 61% of covered workers are in self-insured plans that are not necessarily covered by these waivers. Self-funded employers ultimately decide whether to waive cost-sharing or not. Some insurers have said that self-funded employers could opt-out of the waived out-of-pocket costs, whereas other insurers allow employers to opt-in. It is not clear how many self-funded employers have waived these costs.

Importantly, because of the substantial drop in overall healthcare utilization during the last several months, insurers are still on-track to see considerable profits by the end of this year. This continued profitability means that, even with these cost-sharing waivers and premium relief measures, insurers may still owe enrollees substantial MLR rebates next year.

Methods

We reviewed a summary of private insurers responses to the pandemic, put together by America’s Health Insurance Plans (AHIP), the trade association representing private insurers. We systematically collected data from this summary as of July 31. For plans included in the AHIP summary, we merged on enrollment data as of the first quarter of 2020. Enrollment data were reported to the National Association of Insurance Commissioners (NAIC) and compiled by Mark Farrah Associated TM. Individual market enrollment may contain trace amounts of CHIP enrollment. State actions on cost-sharing and premium policies were sourced from KFF’s tracker of State Data and Policy Actions to Address Coronavirus, which is updated daily.

The Peterson Center on Healthcare and KFF are partnering to monitor how well the U.S. healthcare system is performing in terms of quality and cost.