Federal law requires all private insurance plans to cover the entire cost associated with approved COVID-19 testing so long as the test is deemed medically appropriate. Additionally, the U.S. government pre-paid for COVID-19 vaccines and required COVID-19 vaccines be made available at no out-of-pocket costs regardless of whether the vaccine recipient is insured. However, while a handful of states required or created agreements with insurers to waive COVID-19 out-of-pocket treatment costs for their fully-insured plan enrollees, there is no federal mandate requiring insurers to do so.

Earlier in the pandemic, we found that the vast majority (88%) of people enrolled in fully-insured private health plans nonetheless would have had their out-of-pocket costs waived if they were hospitalized with COVID-19. At the time, health insurers were highly profitable due to lower-than-expected health care use, while hospitals and health care workers were overwhelmed with COVID-19 patients. Insurers may have also wanted to be sympathetic toward COVID-19 patients, and some may have also feared the possibility of a federal mandate to provide care free-of-charge to COVID-19 patients, so they voluntarily waived these costs for at least some period of time during the pandemic. Our subsequent analysis found that several of these insurers were starting to phase out COVID-19 cost-sharing waivers by November 2020.

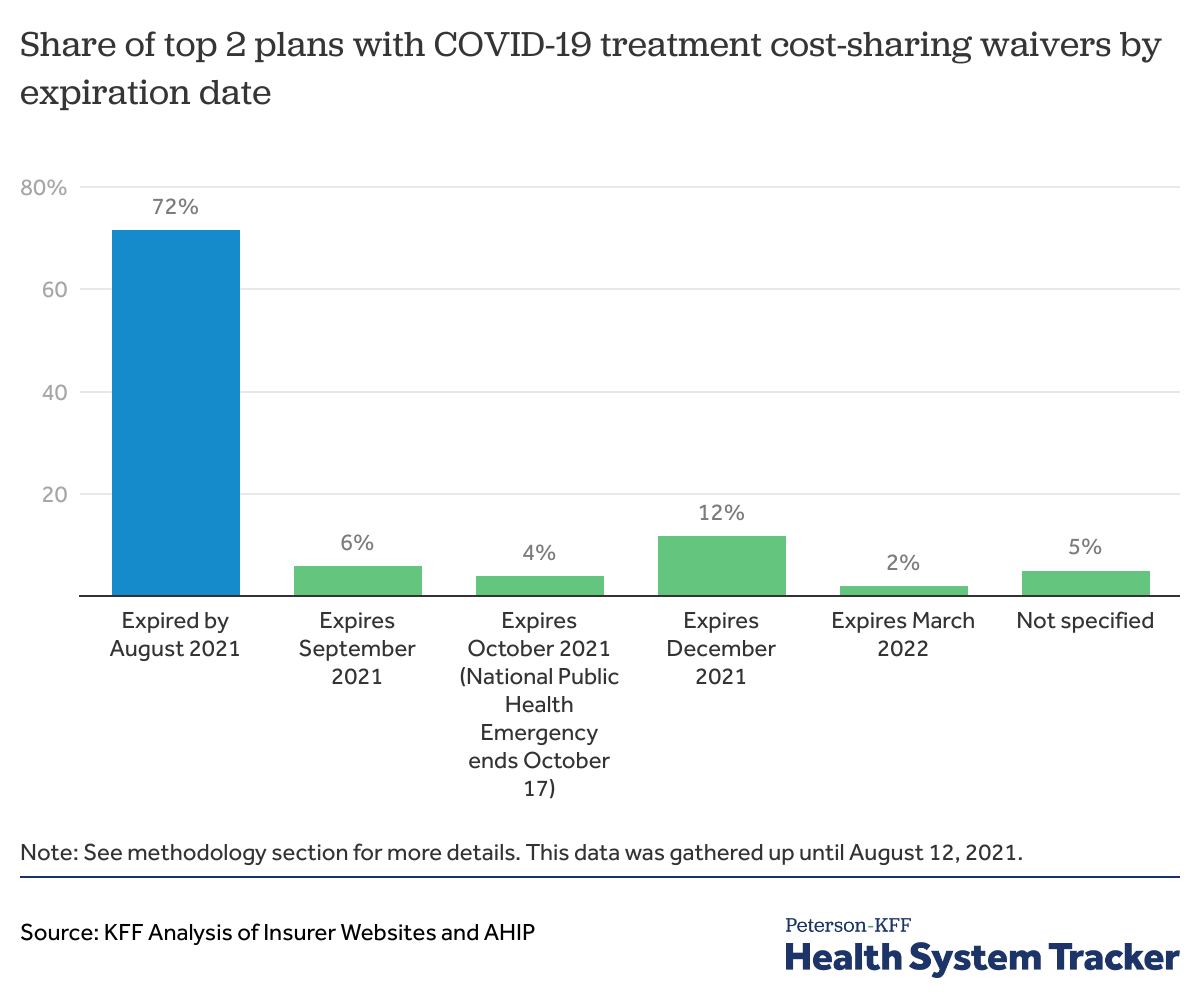

In the last few months, the environment has shifted with safe and highly effective vaccines now widely available. In this brief, we once again review how many private insurers are continuing to waive patient cost sharing for COVID-19 treatment. We find that 72% of the two largest insurers in each state and DC (102 health plans) are no longer waiving these costs, and another 10% of plans are phasing out waivers by the end of October.

Nearly three-quarters of the largest health plans are no longer waiving cost-sharing for COVID-19 treatment

Across the two largest health plans in each state and D.C. (102 plans), 73 plans (72% of 102 plans) are no longer waiving out-of-pocket costs for COVID-19 treatment. Almost half these plans (50 plans) ended cost-sharing waivers by April 2021, which is around the time most states were opening vaccinations to all adults. Of the 29 plans still waiving cost-sharing for COVID-19 treatment, 10 waivers are set to expire by the end of October. This includes waivers that tie to the end of the federal Public Health Emergency, which is currently set to expire on October 17, 2021, though may be extended. Another 12 plans state that their cost-sharing waivers will expire by the end of 2021. Two plans specified end dates for COVID-19 treatment waivers in 2022 and 5 plans did not specify an expiration date.

All of the 102 plans we reviewed (two largest plans in each state) had waived cost-sharing for COVID-19 treatment at some point since 2020. (These health plans represent 62% of enrollment across the fully insured individual and group markets).

Related Content:

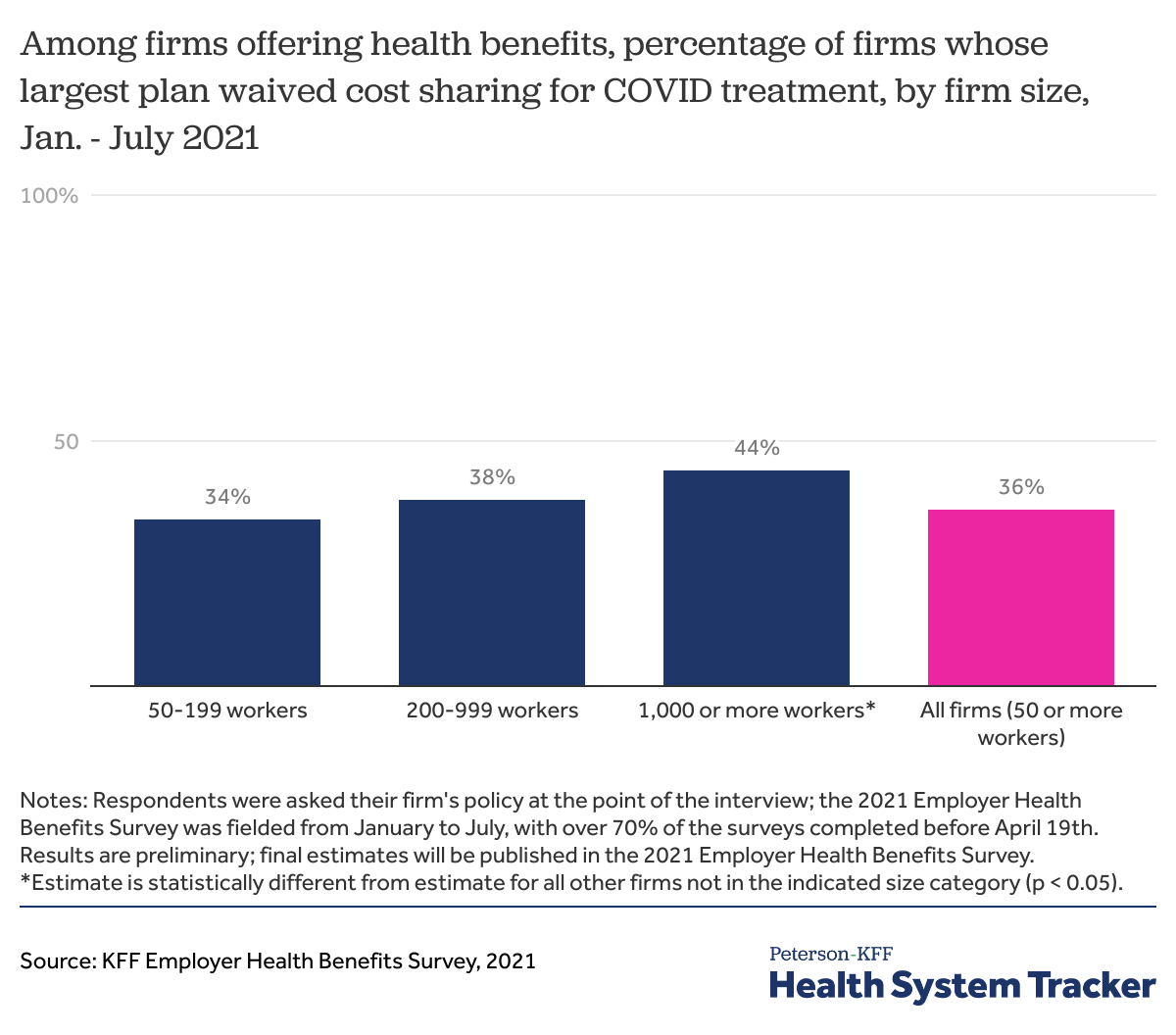

In early 2021, about one-third of employers said their largest plan waived COVID-19 treatment costs

Many employers offering self-funded and fully insured health plans to their employees also reported waiving COVID-19 treatment cost sharing based on preliminary results from the 2021 KFF Employer Health Benefits Survey (EHBS), which was fielded between January and July 2021 with over 70% of the interviews completed before April 19th when vaccines became available for most adults. Since this survey was conducted earlier in the year, many of the waivers may have already expired by the time of this report.

Based on preliminary results from the 2021 EHBS, 36% of firms (with 50 or more employees) reported that their largest plan waived cost sharing for COVID-19 treatment at the time of the survey. Larger firms with 1,000 or more workers were more likely to waive COVID-19 treatment cost-sharing for enrollees than smaller employers.

This survey includes both self-funded employers and those buying fully insured coverage. Before this survey, there was no way to know whether self-funded employers were also waiving these costs as the decision was not up to the insurer administering the plan. In the survey, we see that self-funded employers were similarly likely as employers purchasing fully-insured plans to offer waivers for COVID-19 cost sharing.

Discussion

Motivated by high profits, ACA medical loss ratio rebate requirements, public health concerns about managing the pandemic, and concern over a federal mandate to cover COVID-19 treatment costs, many insurers offered financial relief to their enrollees amid the coronavirus pandemic, primarily through waived COVID-19 treatment costs and less commonly through premium credits or reductions.

Earlier in the pandemic, relatively few COVID-19 patients would have been billed for their hospitalization because of the voluntary waivers extended by private insurers and employers. But as vaccines have become widely available to adults in the U.S. and health care utilization has rebounded more generally, health insurers may no longer face political or public relations pressure to continue waiving costs for COVID-19 treatment. As more waivers expire, more people hospitalized for COVID-19 – the vast majority of whom are unvaccinated – will likely receive significant medical bills for their treatment.

The typical deductible in employer health plans is $1,644, and our earlier analysis found that large group enrollees hospitalized with pneumonia (requiring similar treatment to those hospitalized with COVID-19) paid an average of over $1,300 out-of-pocket. Although this is a large amount to most patients, and could be an incentive to get vaccinated, it still only represents a fraction of the cost born to society for these largely preventable hospitalizations. Unvaccinated COVID-19 hospitalizations cost the U.S. health system $2.3 billion in June and July 2021.

Methods

We used the 2019 Mark Farrah HHS MLR Reporting data to identify the top two plans with the largest combined individual and fully-insured plan enrollment in each state and D.C. We systematically reviewed whether each of the 102 plan provided cost-sharing waivers for COVID-19 treatment and when the waivers expired using each insurer’s COVID-19 resources webpage and relevant press releases.

Many insurers referenced “treatment” broadly in context of cost-sharing waivers. However, there were instances when the form of treatment was specified. We used the cost-sharing waiver expiration date for hospitalizations and emergency room visits when the insurer reported different cost-sharing waiver expiration dates for antibody treatment and for hospitalizations and emergency room visits. If the information could not be located on the plan’s website, we pulled information from the insurer’s parent company’s website and made phone calls to insurers when necessary.

In instances where we could not locate information from insurer or parent company websites, we deferred to the America’s Health Insurance Plans (AHIP), the trade association representing private insurers, summary that was last updated as of April 8, 2021. If a date of expiration was unavailable for insurers that said they were waiving treatment costs, we categorized the plans as “not specified.”

The annual KFF Employer Health Benefits Survey (EHBS) for 2021 was conducted between January and July of 2021 and included almost 1,700 randomly selected, non-federal public and private firms with three or more employees. The methods for the 2021 EHBS are similar to those used in 2020. In 2021, we asked firms if they currently waived cost-sharing for treating enrollees who become infected with COVID-19. A full description of the 2021 methods, finalized data, and findings on other topics such as health insurance premiums and firm offer rates will be released in the fall of 2021. The results described above are preliminary.

The Peterson Center on Healthcare and KFF are partnering to monitor how well the U.S. healthcare system is performing in terms of quality and cost.