Each year, health insurers submit rate filings to state regulators, detailing their expectations for the coming year’s health costs. These filings can provide insight into what factors insurers expect will drive health costs for the coming year, including inflation, the COVID-19 pandemic, and policy changes.

In this analysis, we reviewed rate filings from plans participating in the Affordable Care Act (ACA) Marketplaces to track what insurers say will be driving premium growth in the coming year. A relatively small share of the population is enrolled in these plans (compared to the number in employer plans), but these filings are generally more detailed and publicly available. At the time of this brief, we have compiled data from 72 insurers across 13 states and the District of Columbia. (The 13 states reviewed include: Georgia, Indiana, Iowa, Kentucky, Maryland, Michigan, Minnesota, New York, Oregon, Rhode Island, Texas, Vermont, and Washington.) These filings are preliminary and may change during the review process. Rates will be finalized in late summer.

In tracking these filings, we are looking at several factors that could drive costs in 2023, including health cost trend (which includes health sector inflation and changes in utilization), the COVID-19 pandemic, and changes in federal policies (including the possible expiration of the American Rescue Plan Act subsidies, the implementation of the No Surprises Act, and the administrative fix to the Family Glitch).

We find that insurers in this market are proposing to raise premiums by more than in recent years. The median proposed premium increase is 10% across these 72 insurers. The main contributor to premium growth is health cost trend, which reflects rising prices paid to providers and pharmaceutical companies as well as a rebound in utilization. While our analysis focuses on the ACA markets, the main premium drivers we identified (prices and utilization) are systemic and not specific to the ACA markets.

Preliminary premium changes in 2023

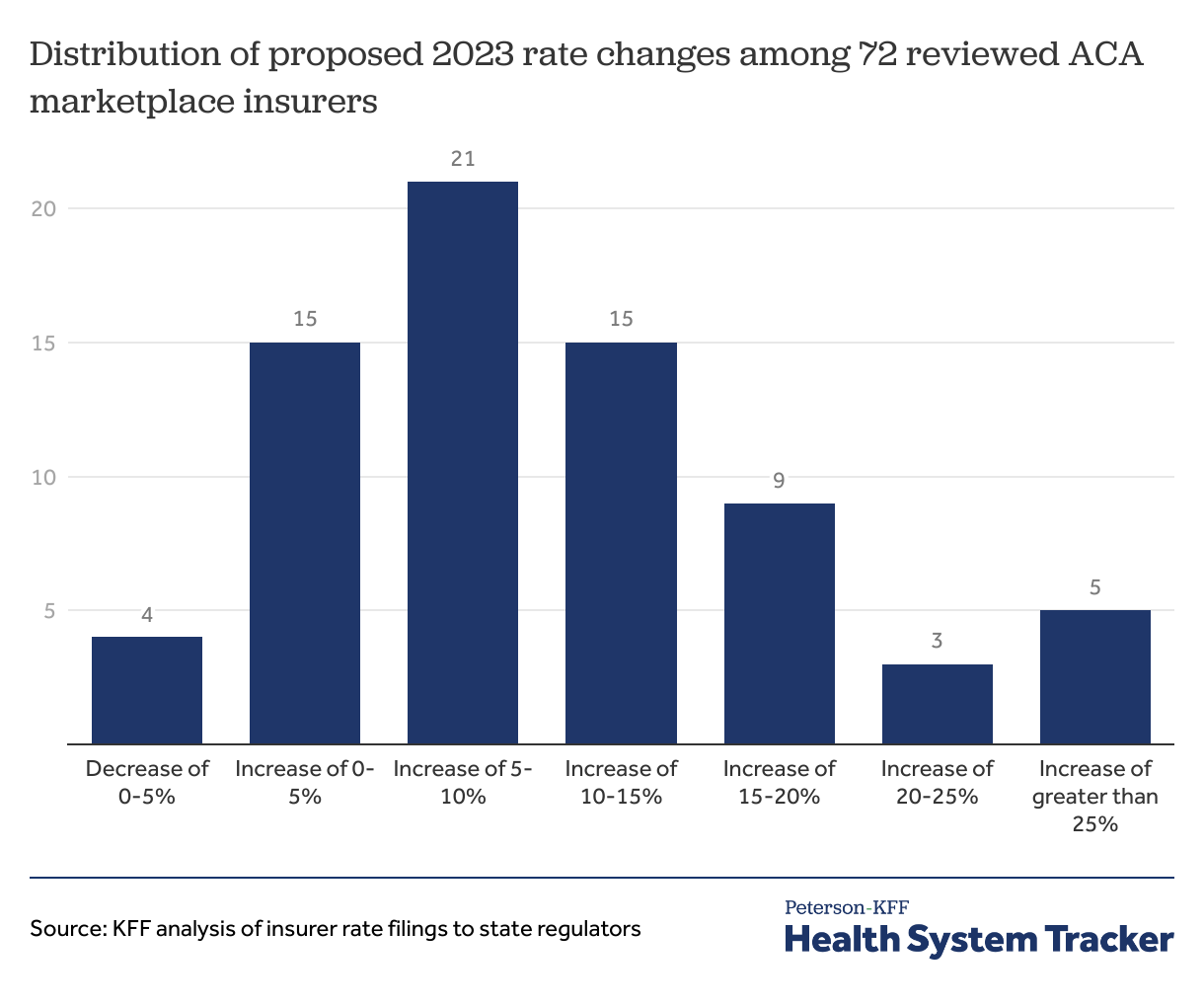

So far, we find that across 72 insurers in 13 states and the District of Columbia, the median proposed premium increase is about 10%. Most premium changes insurers are requesting for 2023 fall between about 5% and 14% percent (the 25th and 75th percentile, respectively). Compared to recent years, relatively few insurers are requesting to lower their premiums, with only 4 out of 72 insurers filing negative premium changes, and the remaining 68 insurers requesting premium increases.

Related Content:

Preliminary 2023 Marketplace filings show an average premium increase of 10%

As these rates are preliminary and we do not yet have data for every state, the actual average percent increase in premiums will not be known until early fall. It is also the case that the overall average increase in premiums is often different from the average increase in the benchmark silver plan, which is the basis for calculating subsidies for Marketplace enrollees.

Factors driving costs

In these filings, insurers describe factors they expect will have either an upward or downward impact on their costs for the coming year. Across all 72 filings, we systematically tracked key words relating to medical trend, the COVID-19 pandemic, and certain policy changes (the expiration of American Rescue Plan Act subsidies, the implementation of the No Surprises Act, and the Family Glitch administrative fix). We also searched for other key words relating to current issues like telemedicine and mental health, but we found most insurers did not reference these subjects in their filings. Insurers do not always publicly quantify all factors driving their premiums.

Inflation and utilization trends

Every year, insurers are asked to project their health cost “trend,” which is a combination of rising prices paid to hospitals, doctors, and pharmaceutical companies (inflation) and upward or downward expectations for utilization (or, the number of visits, stays, or prescriptions).

As is the case in most years, health cost trend is a key driver of premium growth in the coming year. For example, in their 2023 filings, many insurers are projecting a trend of about 4-8%.

Although insurers are primarily interested in price growth in the health sector, given the unusually high pace of inflation in the rest of the economy, there is potential for general economic inflation to flow through to the health sector. For example, Capital District Physicians Health Plan in New York warned of an imminent market correction, saying: “CPI for All goods and Services as of March 2022 was 8.5%, up 7% from pre-pandemic levels. Medical Care Services CPI in March 2020 (pre-pandemic) was 5.5% and as of March 2022 is 2.9%. This data suggests a correction is imminent as labor and supply cost increases directly impact hospitals and physician offices.”

COVID-19

Over the course of the pandemic, most insurers in recent years have described how they expect the pandemic will shape their costs for the coming year. The pandemic can have both upward effects on health costs (such as through hospitalization and vaccine administration costs), as well as downward effects (such as through suppressed utilization). Amid the uncertainty surrounding the pandemic, many insurers in 2021 and 2022 said they expected the pandemic would have a net neutral impact of 0% on their premiums, though some projected a slight negative or positive impact.

For 2023, most Marketplace insurers mentioned the pandemic, and about half of the insurers we reviewed publicly quantified the pandemic’s effect on their premiums. As was the case in past years, some insurers said the pandemic would have a slight upward effect on rates while others said it would have a slight downward effect. Of the insurers that quantified the effect of the pandemic, most said it would have only a small impact on premiums (commonly plus or minus 1-2%).

Several insurers noted that utilization of care is expected to rebound after having been suppressed during the early pandemic. For example, in Washington state, Regence Blue Cross Blue Shield “expects non‐COVID‐19 utilization and claims levels to return to trended pre‐pandemic levels.”

Fidelis Care in New York “expects a significant decrease in costs associated with [COVID-19] treatment, but an increase in costs associated with vaccines and boosters.” They go on to say, “it is projected that insurers will be responsible for ingredients costs as well as increased billing due to fewer ‘mass vaccination’ programs.”

Similarly, between the rollout of child vaccines and boosters for adults, Excellus Health Plan in New York expects 25% of the population to receive a vaccine or booster in 2023. Excellus also “expects to be liable for the ingredient cost in addition to the administration cost of the vaccine” with the expected lack of federal funding for vaccines.

Policy changes

There are several federal policy changes that have the potential to affect premiums in 2023, including the expiration of the American Rescue Plan Act subsidies, the implementation of the No Surprises Act and the administrative fix to the Family Glitch.

The most significant potential policy change is the expiration of the American Rescue Plan Act subsidies. These subsidies provided temporary assistance for ACA Marketplace enrollees to pay for their premiums, boosting the amount of the subsidy for those who were already eligible and expanding subsidy eligibility to millions of middle-income people, many of whom were previously priced out of the markets.

Just under half of the insurers we reviewed quantified an effect of the expiration of ARPA subsidies on 2023 premiums. Of those insurers that publicly quantified an impact, about half said the expiration of ARPA would have a neutral impact, while the other half said it would have a slight upward impact on their costs (often no more than around 1%).

For example, Excellus Health Plan in New York said the expiration of ARPA subsidies would have a nearly neutral impact on rates (0.2%), saying, “The population that is most likely to drop without these enhanced credits have better morbidity and substantially lower cost than those unlikely to move. This shift in the population would impact both expected claims and risk adjustment amounts.”

In Michigan, Oscar Insurance Company said, “due to the uncertainty related to the potential extension of the expanded APTC subsidies, Oscar assumed they are due to expire at the end of 2022, which is expected to decrease market membership and subsequently increase market morbidity. The expiration of the subsidies has a premium impact of +1.7%. Should the subsidies be extended, it would decrease the rates by 1.7%.”

Only a couple insurers mentioned the implementation of the No Surprises Act, which prohibits most instances of surprise balance billing and only one insurer mentioned (though did not publicly quantify the impact of) the implementation of the family glitch fix. Of the two insurers that quantified the effect of the No Surprises Act, both said it would have a 0% impact on their premiums.

Discussion

After a few years of virtually flat premiums in the ACA marketplaces, it appears 2023 rates may rise significantly. Although this brief is just an early look at preliminary rate filings, so far, the pattern emerging is that most insurers are requesting premium increases in the high single digits or low double digits.

A substantial share of the increase in premiums is from rising health prices and utilization of health care, with the pandemic and policy changes having a relatively small impact on premiums. The rising prices and utilization insurers foresee in the ACA market are not necessarily specific to the ACA markets and therefore could affect premiums for employer-sponsored coverage as well.

Although the COVID-19 pandemic has had an enormous impact on the U.S. health system and society more broadly, for the third straight year, many insurers are projecting the pandemic will have a net neutral or only slight impact on health costs and premiums.

There are several federal policy changes that have the potential to impact premiums, particularly in the ACA markets. The most commonly mentioned by insurers is the potential expiration of American Rescue Plan Act subsidies. If these subsidies expire, out-of-pocket premium payments will rise sharply, which could cause some healthier enrollees to lose coverage. Some insurers said the expiration of these subsidies would have a slight upward effect on their premiums, but also said that if Congress extended the subsidies before rates are finalized, the insurers would reverse that increase. Congress is currently considering an extension of these subsidies, but it is unclear if they will act before 2023 premiums are locked in.

Other policy changes are not having much of an effect on 2023 premiums. The Congressional Budget Office projected the No Surprises Act would have a slight downward effect on premiums of 0.5% to 1%, however, both this year and last year, we find that insurers are generally refraining from attributing premium changes to the new law.

The Peterson Center on Healthcare and KFF are partnering to monitor how well the U.S. healthcare system is performing in terms of quality and cost.