In this analysis, we explore trends in prices for health services over time in the U.S. (A related chart collection shows trends in prices and utilization in the U.S. and comparable countries). We find that prices have increased for a variety of health services more rapidly than general economic inflation, particularly for the privately insured. Additionally, there is wide geographic variation in the prices paid for the same services across major metropolitan areas in the U.S.

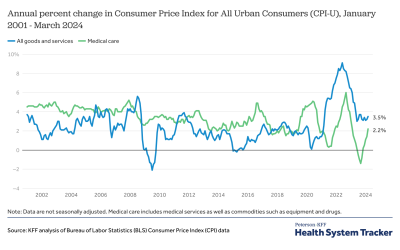

Prices for healthcare have grown faster than prices in the general economy

Since the end of 2007, healthcare prices have grown 21.6%, while prices in the general economy (measured by the GDP deflator) have grown 17.3%.

Prices for inpatient hospital care have grown rapidly for privately insured patients

A price index is a standardized measure of how average prices have changed over time. Prices for inpatient care have risen more rapidly for patients with private insurance when compared to prices for patients with Medicare or Medicaid. Between Mid-2014 and first quarter 2018, inpatient prices for patients with private insurance rose about 13 percent compared to about 3 percent for patients with Medicare and Medicaid, and about 6 percent for the general economy.

Prices for inpatient hospital stays are higher and have grown faster for private insurance than those for Medicare or Medicaid

This recent faster growth in inpatient prices for the privately insured is the continuation of a longer trend. This chart, which updates and refines data presented here, shows that inflation-adjusted private prices for hospitals stays are higher than prices paid by public programs and have been growing much faster. In 2015, hospital inpatient prices for private patients were 68 percent above those for Medicare patients

The average price of laparoscopic appendectomy procedures has increased far faster than other prices in the economy

The increase in private prices can be seen in the cost of some common inpatient procedures. In our analysis of employer claims data, we refer to “prices” as the weighted average of actual expenditures made for a given service by insurers and enrollees in the large employer market. The average price paid by large employer plans for an inpatient admission for a laparoscopic appendectomy increased by 136% between 2003 and 2016, much faster than general price increases over the period (28%).

The average price of knee replacement has increased faster than general inflation

There is a similar story for inpatient admissions for full knee replacements, where the average price paid by large employer plans increased by 74% between 2003 and 2016, compared to 28% increase in overall inflation.

There is large variation in the prices for common procedures

As others have shown, there is considerable variation around average price paid for the same procedures. In 2016, while the average price paid by large employers for an admission for a full knee replacement was $34,063, 25 percent of admissions had a price of $24,734 or less and another 25 percent had prices higher than $39,786. Ten percent of admissions had prices in excess of $52,181 (53% above the average).

For laparoscopic appendectomies, the average price paid for an admission was $20,192 in 2016; 25 percent of admissions had prices of $12,088 or less while another 25% had prices of over $24,847. Ten percent of admissions had prices in excess of $35,308 (75% above the average).

Related Content:

The average price of full knee replacements varies considerably across markets

Average price paid by large employer plans for full knee replacements varied considerably across markets. This figure plots average prices in metropolitan statistical areas (MSAs) with more than 125 full knee replacements in the MarketScan data for 2016. For example, the average price of a full knee replacement in the New York City area ($50 thousand) is more than twice the price of the same procedure in the Louisville, Kentucky area ($23 thousand). The national average was $34,063.

The price of office visits has risen consistently since 2003

Prices for outpatient office visits also grew much faster than general price inflation over the 2003 to 2016 period, rising from an average price of $60 to $101 or 69% compared to a 28% increase in overall inflation. Office visits are coded at five different levels (with other modifiers), depending on the scope of the services and level of complexity of medical decision making.

Prices increased for all levels of outpatient office visits, including the least severe/complex cases (Level 1) and most severe/complex cases (Level 5)

Outpatient visits with the highest level of acuity (the most severe and most complex cases) are coded as Level 5, while visits with for straightforward, minor conditions are coded as Level 1. Average prices increased for each of the five levels. From 2003 – 2016, the average price for Level 1 visits increased by $21 or 85% (compared to 28% of general economic inflation) and the average price for Level 5 visits increased by $62 or 52%. The average price of Level 3 visits, which are the most common, increased by $30 or 54% from 2003 – 2016.

The price and complexity of billed outpatient office visits increased over the past decade

The share of office visits coded as Level 4 (moderate to high severity) increased, while the share coded as Level 3 or lower complexity/severity decreased over the 2003 to 2016 period. The share of office visits coded as Level 3 dropped from 60% to 52% while the share coded at the higher level-4 increased from 19% to 36% over this period. The share of visits at the lower level-2 also decreased, from 14% to 7%, over the period.

The average price of outpatient visits varies considerably across markets

Average price paid by large employer plans for outpatient visits varied considerably across markets. This figure plots the average price in the largest 25 reportable metropolitan statistical areas (MSAs) with more than 1000 outpatient office visits in the MarketScan data for 2016. For example, the average price for an outpatient office visit in the Minneapolis, Minnesota area ($158) is more than twice the average price in the St. Louis, Missouri area ($78). The national average was $101.

The average price of lower back MRIs increased slower than inflation

Not all services have rapidly rising prices. The average price paid by large employer plans for an outpatient MRI of the lower back rose only about 14% between 2003 and 2016, about one-half the increase in general price inflation over the period (28%). The prices here include the cost of the MRI itself and the professional cost of interpreting the result.

The average price of lower back MRIs varies considerably by location

Average price paid by large employer plans for a lower-back MRI varied depending on the location in which it occurred. This figure plots average prices in the largest 25 reportable metropolitan statistical areas (MSAs) with more than 750 MRIs in the MarketScan data for 2016. The average price for a lower-back MRI in the Chicago, Illinois area ($1,123) is more than twice the average price in the Baltimore, Maryland or Farmington Hills, Michigan areas. The national average was $894.

Average MRI prices are higher and variation is greater in hospital settings than in other clinical locations

For outpatient MRIs of the lower back, there was a considerable difference between the average price paid by large employer plans of an MRI conducted in a physician office ($610) and those performed in a hospital ($1,335). There also was considerable variation around each of these averages: for office-based MRIs, 25 percent were priced at or below $397 (65% of the average for office-based procedures). For those performed in a hospital, 25 percent were priced more than $1,800 (35% above the average for hospital outpatient procedures).

Methods

We analyzed a sample of claims obtained from the Truven Health Analytics MarketScan Commercial Claims and Encounters Database (MarketScan). The database has claims provided by large employers (those with more than 1,000 employees). This analysis only includes costs for services covered by large employer plans. We used a subset of claims from the years 2003 through 2016. In 2016, there were claims for almost 20 million people representing about 23% of the 85 million people in the large group market.

Weights were applied to match counts in the Current Population Survey for large group enrollees by sex, age, state and whether the enrollee was a policy holder or dependent. People 65 and over were excluded. We also limited claims to fee-for-service claims (excluding claims collected on an encounter basis). With these limitations, the number of enrollees in the sample varied from about 628,000 in 2003 to over 18 million in 2016. For all averages, the top and bottom 0.5% of claims are excluded.

Midway through 2015, MarketScan claims transitioned from ICD-9 to ICD-10. While both systems classify procedures, they do not precisely crosswalk. Below is a summary of which codes we included:

Related Content:

Total knee replacements are the cost of all services associated with an inpatient admission in which the principal procedure was ICD-9 code 81.54 or any of the subsequent procedures under the ICD-10 headings 0SRD and 0SRC. In addition, admissions without a principal procedure but in which the claim includes CPT code 27447 are included. Admissions with a total cost of less than $500 are excluded.

Laparoscopic appendectomy are the cost of all services associated with an inpatient admission in which the principal procedure was ICD-9 code 47.01 or ICD-10 code 0DTJ4ZZ. In addition, admissions without a principal procedure but in which the claim includes CPT code 44970 are included. Admissions with a total cost of less than $500 are excluded.

Outpatient MRIs include the cost of outpatient claims with a CPT code of 72148. In addition to claims for professional services, some claims include facility fees. In cases in which no other professional services are provided on the date of service, facility fees were included in the cost of the MRI. In order to ensure that we are capturing the cost of performing the MRI and not associated services, claims in which all the cost in a day have a procedure modifier 26 are excluded. MRI with a total cost of less than $25 are excluded.

The cost of an outpatient office visits, is a weighted average of the cost of CPT codes 99211, 99212, 99213, 99214 and 99215. These visit codes are for established patients but vary in complexity and duration. Visits with a cost of less than $5 are excluded.

The Peterson Center on Healthcare and KFF are partnering to monitor how well the U.S. healthcare system is performing in terms of quality and cost.