Summary

Since 2021, hospitals have been required to publicly post standard charges and negotiated rates for the common health services and procedures. These price transparency requirements are intended to enable patients to compare prices and promote competition in the health care markets. Additionally, these data have been used by researchers for conducting research on prices and competition in the health industry.

In previous analyses, we looked at the Centers for Medicare and Medicaid Services (CMS) price transparency requirements, consumers’ awareness of these rules, variation in prices, and early compliance with the rule. In this analysis, we focus on the quality and usefulness of the data, examining how well the information facilitates comparison of prices for services across hospitals, and discussing the utility of price transparency data for consumers, researchers, journalists, and other users.

We find that currently the data are challenging to use for several reasons:

- Specification of what services prices correspond with is inconsistent, especially for episodes of care (e.g., negotiated rates attached to a treatment episode for a hip/knee replacement might correspond to a per diem charge instead of the entire episode).

- Data quality can vary widely, with questionably low and high values for negotiated rates (e.g., negotiated rates representing a proportion or multiplier of a rate may appear as less than one dollar).

- Crucial pieces of information for interpreting the applicability of price are missing, such as contracting method and payer class (Medicare, Medicaid, and commercial), as certain payer classes generally have lower rates.

These challenges do not result necessarily from lack of compliance with the rule; rather, these findings highlight its shortcomings in facilitating price comparisons. The complexity of using the data is largely due to a lack of standardization and specification in the reporting requirements.

Consistent specification of the following elements would improve reliability and usability of the data: the charge’s applicable hospital setting (inpatient or outpatient), charge type (facility or professional), associated charge modifiers that affect pricing or payment of a service, the time period covered, any bundles the charge is a part of, the health plan type, and how the charge differs from the base rate. To address some of these issues, CMS has provided suggestions for formatting, validation of data format, and data quality. Hospitals’ use of these resources remains voluntary.

Read more from

Price Transparency

Researchers and analysts using price transparency data collated from the machine-readable files will have to assess how the lack of consistency affects findings. Inattention to this lack of standardization could skew results. For consumers, there may be limited opportunities to price shop for care with limited providers or appointments available to them. In situations where a consumer could shop for hospital care, the complexity of reimbursement mechanisms, plan designs, and out-of-pocket cost responsibility limits price-based shopping for consumers.

Background

Beginning in the Trump administration, the Centers for Medicare and Medicaid Services (CMS) promulgated rules that require hospitals to provide the public clear and accessible information about their standard charges for the health care items and services that they provide, including prices negotiated with each health plan. Hospitals must update the information at least annually. Similar negotiated rate information from payers is required under the Transparency in Coverage rule. This brief uses price transparency information made public by hospitals.

In the preamble to the final rule, the agency (CMS) asserted that disclosing hospital prices will provide information that patients, employers, clinicians, and others need to make more informed decisions about their care, increasing market competition and driving down the cost of health services, asserting “a direct connection between transparency in hospital standard charge information and having more affordable healthcare and lower health coverage costs.”

The preamble provides support for two distinct aspects of price transparency. The first is making standard prices transparent to all market participants through a machine-readable file, so that purchasers and competitors will use information about actual transaction costs to sharpen their own negotiations, heightening price competition, and reducing costs overall. Secondly, vendors also may be able to use this information to profile the relative costs of different hospital services for consumers. To this end, the rule requires hospitals to disclose the standard charges for all the items, services, and bundled services that they have established rates for. While there is some flexibility as to how the machine-readable file is constructed, it must include for each item or service provided by the hospital in the inpatient or outpatient setting, as applicable:

- A description of each item or service provided by the hospital

- The gross charge (list prices that are not typically billed to insurers)

- Payer-specific negotiated charges clearly associated with the names of each third-party payer and plan (a negotiated rate paid by an insurer)

- The de-identified minimum negotiated charge (the minimum of all insurer negotiated rates)

- The de-identified maximum negotiated charge (the maximum of all insurer negotiated rates)

- The discounted cash price

- Any code used by the hospital for accounting or billing, including but not limited to Current Procedural Terminology (CPT) code, Healthcare Common Procedure Coding System (HCPCS) code, Diagnosis Related Group (DRG), and National Drug Code (NDC).

Hospitals have been slow to comply with the new requirements. Our previous analysis looking at the two largest hospitals in each state found that most were not providing payer-negotiated rates and, even among those that did, some did not include plan names or market information as required by the rule. The analysis identified other issues as well, including hospitals that disclosed average, median, or estimated rates rather than the required standard charge for each item and service, or requiring patients to enter personal information to gain access to the information required to be disclosed. A study by PatientRightsAdvocate.org reviewing 2,000 selected hospitals in February 2023 found that about a quarter of hospitals were following all of the price transparency rule requirements, with just under half not sufficiently identifying payer and plan names for each payer-specific negotiated rates.

Approach

For this analysis, rather than trying to assess compliance with the rule, we take a preliminary look at how well the hospital price transparency disclosures facilitate comparison of prices for services across hospitals. In this brief, we only address the machine-readable file and not shoppable services, services identified by CMS that can be scheduled by a healthcare consumer in advance. Further analysis on how well the data enable shoppable services may be discussed in a subsequent brief.

We accessed the hospital price transparency information primarily through a database compiled by Turquoise Health. We also evaluated data through hospitals’ websites. Turquoise Health periodically downloads the machine-readable files posted by hospitals and extracts key information for each item or service, including the hospital and health plan names, the rate, the service area within the hospital, and the written description. This information is put into a distributed database that they make available commercially and to the public. In addition to compiling the information posted by hospitals, they add variables that classify and clarify certain data elements; for example, they classify the market for each health plan (e.g., private, Medicaid, Medicare Advantage) from plan names that hospitals list. As of mid-November 2022, the Turquoise database had over one billion records from over 5,100 hospitals. We limited the analysis to acute-care hospitals that had at least one payer-negotiated rate, which reduced the number of hospitals to 4,140. Hospitals listing just cash or list prices were also excluded. We also downloaded the machine-readable files from several hospitals’ websites to explore how they differed in layout and to look at the challenges of compiling the information into a database.

Given the volume of data collected from the hospitals, we focus on two payer-specific negotiated prices for two types of care associated with common procedure codes:

- Hip and knee replacement (MS-DRG 470, “Major hip and knee joint replacement or reattachment of lower extremity without major complication or comorbidity”); and

- Diagnostic colonoscopy (CPT 45378, “Colonoscopy, flexible; diagnostic, including collection of specimen(s) by brushing or washing, when performed (separate procedure)”), which can be provided on an inpatient or outpatient basis.

Our analysis begins with examples of challenges we faced searching the data from the machine-readable files and attempting to make price comparisons across hospitals. We then present summary statistics for the negotiated rates in 2 cities: Chicago and Atlanta. These cities were chosen because they each have many distinct hospitals with payer-specific negotiated rates for the services we chose.

Findings

The chief difficulty in assessing the value of the price transparency data is identifying comparable items and services across hospitals. A standard price may be the price for an entire episode of care, such as a hip replacement; for a particular procedure, such as an x-ray of an ankle; for a piece of medical equipment, such as a particular stent; for a medication with dosage, such as 5mg tablet of aripiprazole; or for some other specific item or service provided by a hospital or professional working for a hospital.

Each charge is accompanied by a written description from the hospital of the item or service (or for a bundle of them), reflecting each hospital’s internal notations which are neither standard nor consistent across hospitals. In many instances, these charges are accompanied by a billing code, for which standardized descriptions are available. The challenges in comparing charges across hospitals vary with level of care. The discussion below outlines some of the challenges encountered with diverse types of searches.

Comparing episodes of care

A charge for an episode of care encompasses the total cost for a procedure, making it the most relevant to compare across providers. The rule requires hospitals to disclose standard charges for bundles of care (including per episode of care) when available, and to associate a code with the bundle if appropriate, such as a Medicare Severity Diagnosis Related Groups (MS-DRG) or an APC (ambulatory payment classification). These codes represent prospective payment amounts for inpatient and outpatient care, respectively.

Not all hospitals have negotiated rates with payers for service bundles based on MS-DRGs, so some hospitals will not have charges associated with some or many MS-DRGs. The lack of any standard charge at a hospital for a particular MS-DRG may mean that either 1) they get paid in other ways, 2) that they do have a service bundle for that type of care but did not associate it with the MS-DRG in their data disclosure, or 3) that they do not provide the care in question.

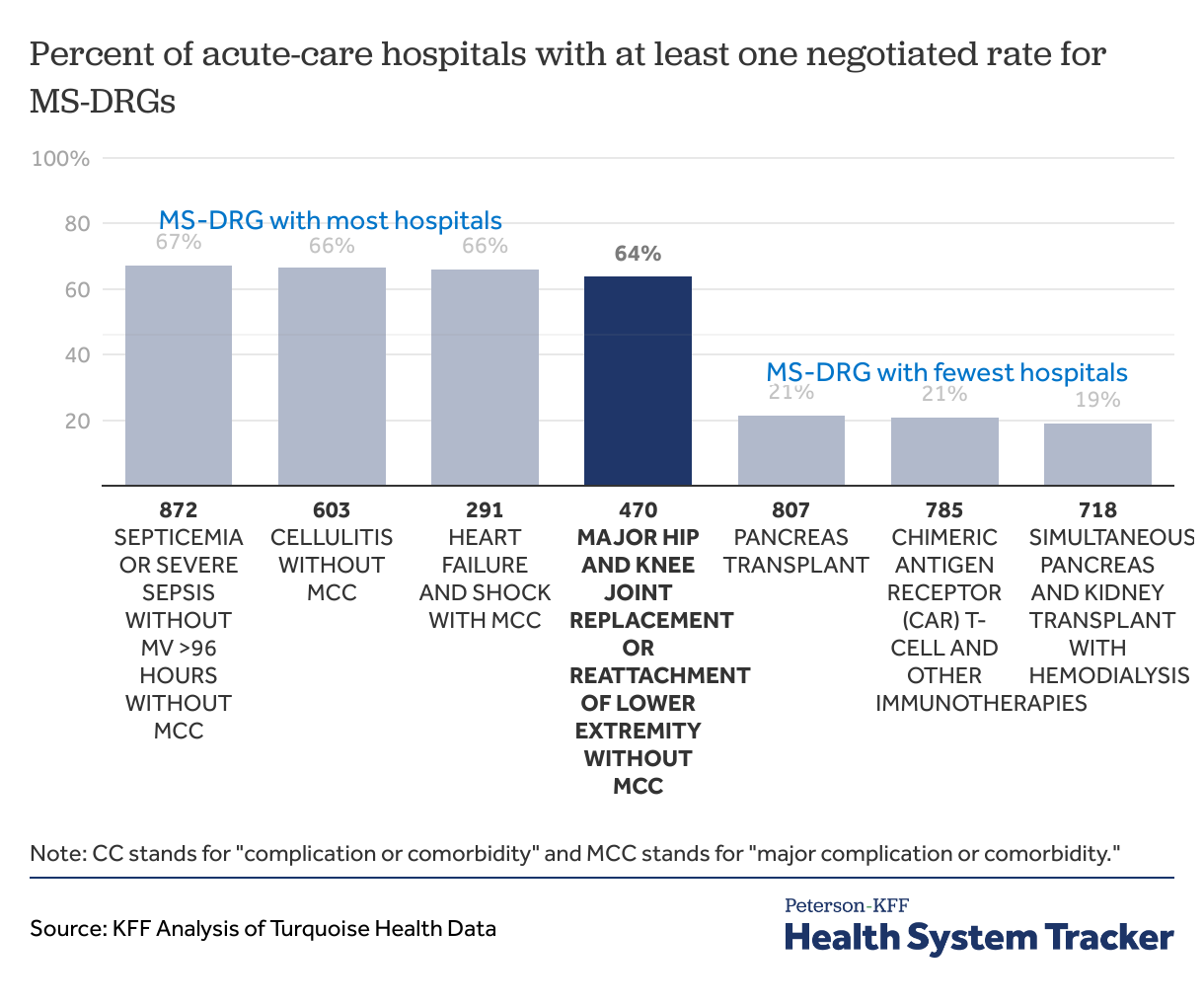

The number of hospitals reporting charges for MS-DRGs varies across MS-DRGs. The proportion of hospitals with at least one negotiated rate varied greatly, from 67% for septicemia to 19% for kidney/pancreas transplant (Figure 1). Of the more than 4,100 acute-care hospitals in the Turquoise Database with negotiated standard charges for at least one item or service, only 64% hospitals of them had at least one negotiated charge for hip and knee replacements (MS-DRG 470).

Figure 1: The number of hospitals reporting charges for MS-DRGs varies

Even when hospitals disclose negotiated standard charges for an MS-DRG, the provided description is sometimes inconsistent with the understood meaning of the episodic nature of the MS-DRG. We illustrate this with an examination of provider-furnished charge descriptions for a hip and knee joint replacement. Some charge descriptions suggest that the charges are:

- Not for the entire episode (e.g., “additional ½ hour anesthesia,” “per diem”),

- For something tangentially related (e,g., “ampicillin 10 gram solution for injection”), or

- Too vague to interpret (e.g., “IP services,” “orthopedic surgery”).

In still other cases, the description may say that the charge is a percentage of charges for the MS-DRG service and therefore not directly comparable to the total cost of hospital services typically associated with an MS-DRG.

In summary, MS-DRG codes alone may not be a sufficient way to identify similar bundles of services across different hospitals. Analysis without accounting for how distinct entries should be aggregated or compared is likely to produce incorrect statistics. Filtering the data based on certain words or letter patterns in the written descriptions may result in more comparable data but would require a subjective and iterative approach to determine which observations to drop or keep.

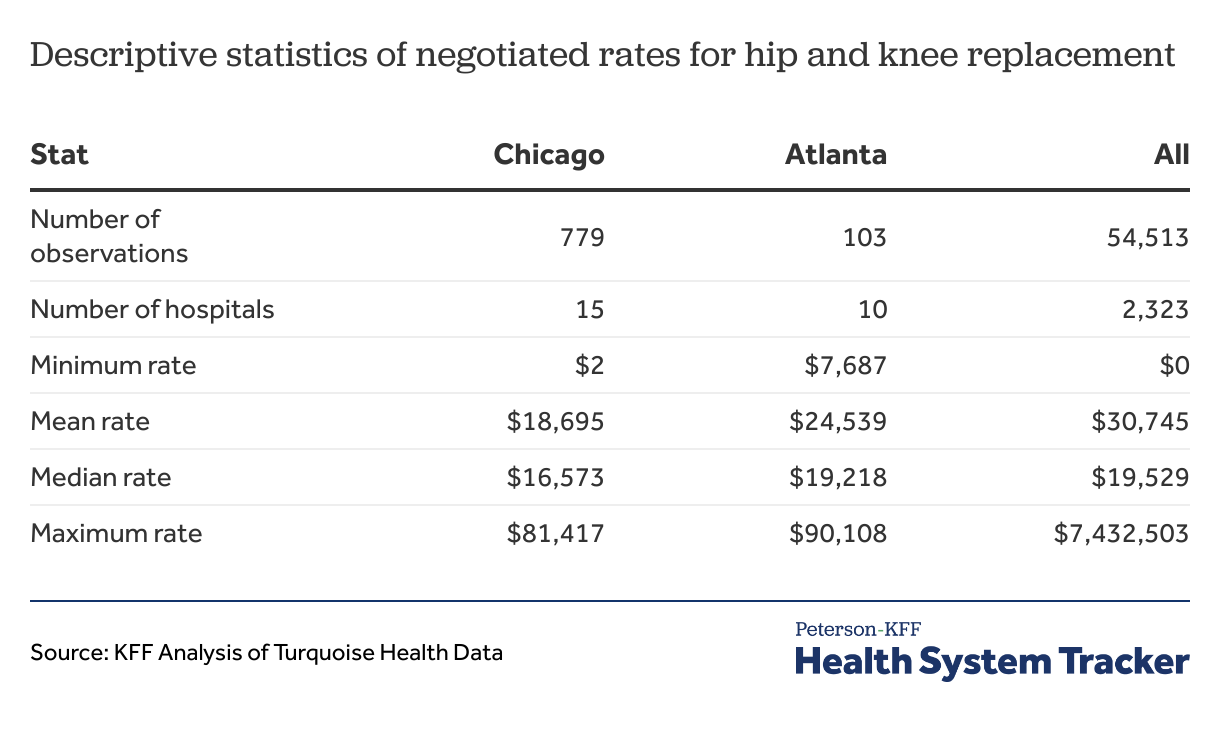

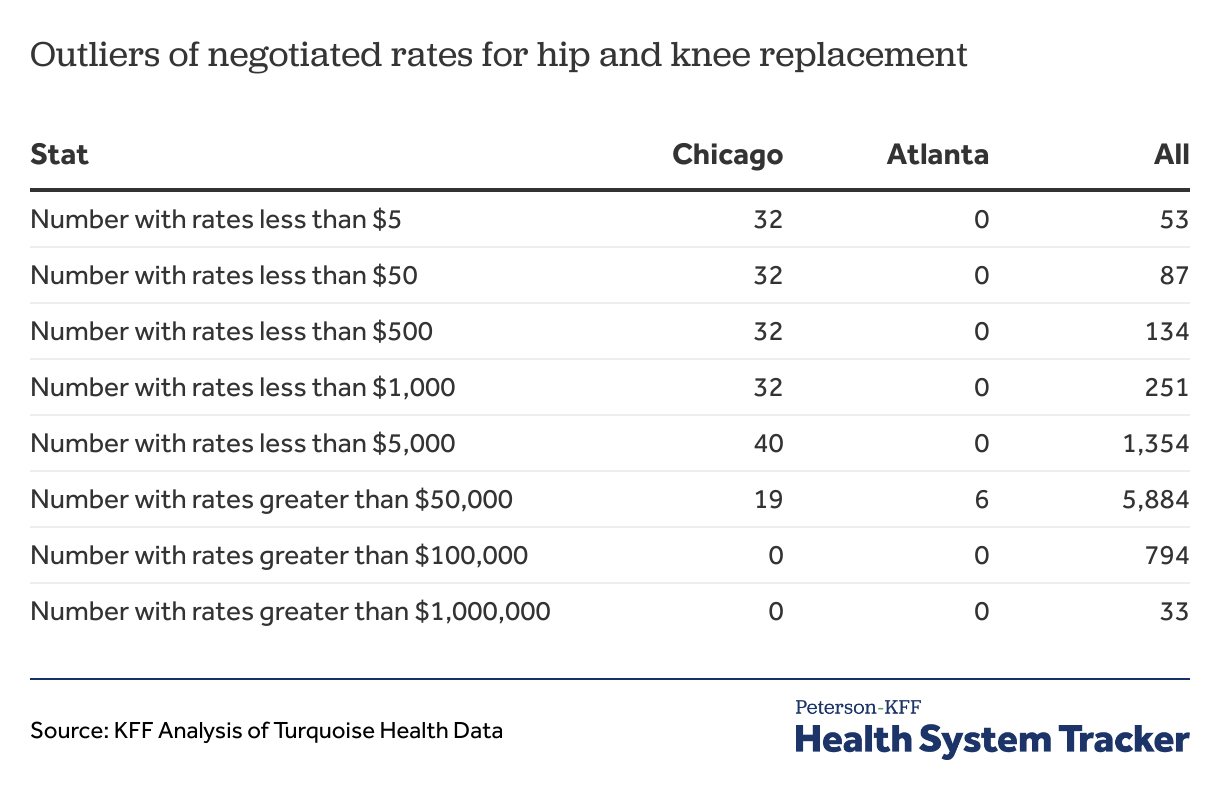

Data users should take some extreme values with a grain of salt. Even after filtering out observations that have inconsistent descriptions, very large and very small negotiated rates appear in the data. When examining charges for hip and knee replacement, we noticed that some of the negotiated rates are over $100,000 and a few are even over $1,000,000. Others seem impossibly small for an admission, with many being less than a few hundred dollars. As the charges represent negotiated rates found in agreements with health plans, the highest values seem suspect, as it is unlikely that a plan would agree to such high levels of payment. Two hospitals accounted for 31 of the 33 observed negotiated hip and knee replacement rates over a million dollars. In total 78 hospitals reported at least one negotiated rate over $100,000.

The smaller observed amounts are more prevalent and more complicated. Seventy-eight had at least one negotiated rate under $1,000, and 46 had at least one under $500. The preamble to the CMS rule recognizes that in some cases, a negotiated standard rate may be a total amount, a per diem amount, a percent of charges, or may be derived from some other calculation. The rule requires hospitals to include their negotiated rates in all these cases, but the lack of any guidance as to how to structure and label the machine-readable files means that there is no consistency in how hospitals indicate these distinct types of charges. Some low negotiated rates in the data may be aberrations, while others may be factors used to calculate the negotiated rate instead of dollar amounts.

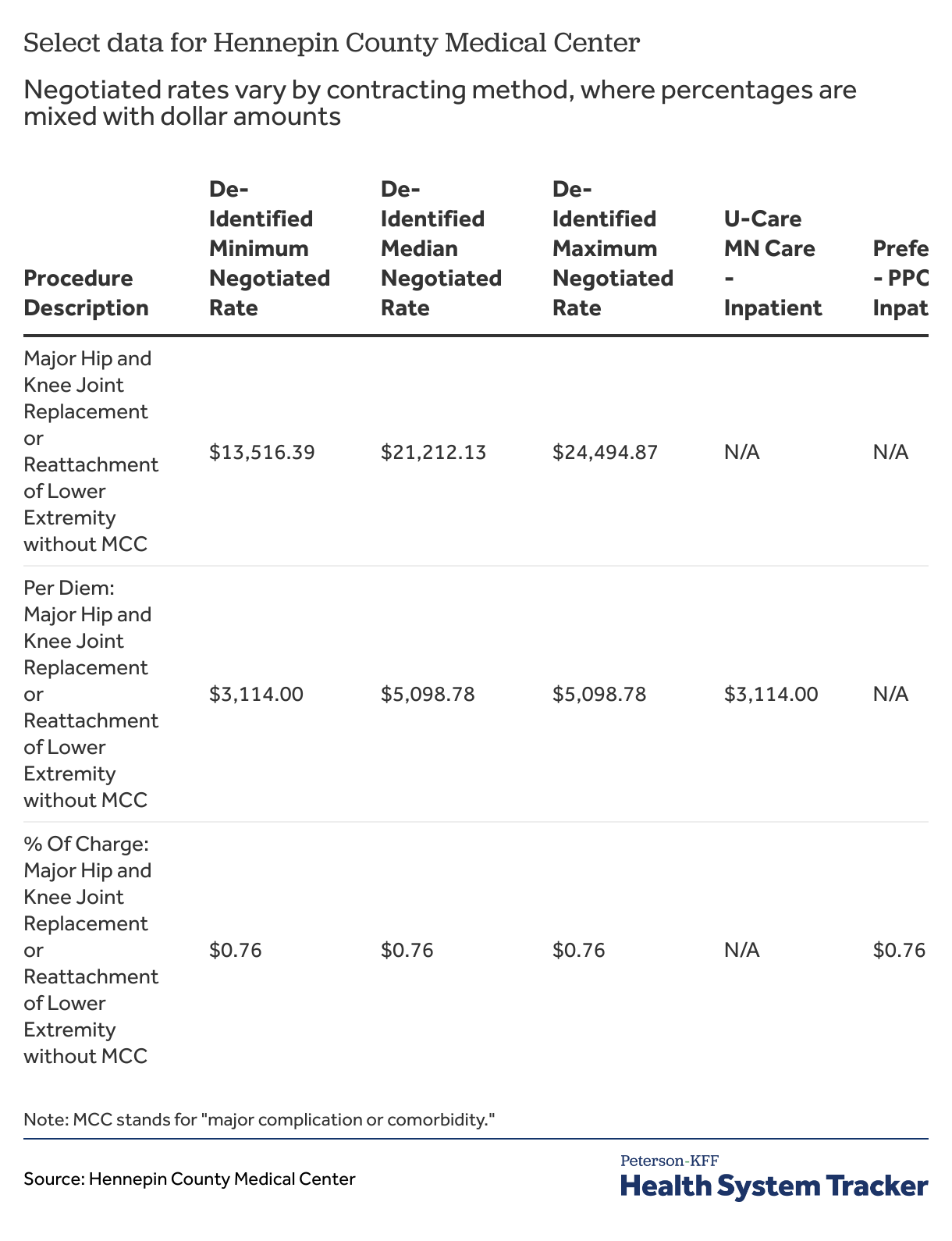

Data downloaded from two different hospitals that have one or more very low rates for hip and knee replacements help to demonstrate the challenge here. Table 2 shows information from three rows of data from the machine-readable file posted by Hennepin County Medical Center. One row has negotiated rates based on a total charge, one based on a per diem charge, and one based on percent of charges. As these three charges are all associated with the same code, the only way to differentiate them is to examine the non-standardized charge descriptions, which have the terms “per diem” and “% of charges” before the description of the service. In this case the “$0.76” in the third row for “Preferred One Premium Inpatient” plan should probably have a percentage sign and represents the share of some charge that has been negotiated with the payer.

Table 2: Negotiated rates vary by contracting method, where percentages are mixed with dollar amounts, as shown from Hennepin County Medical Center data

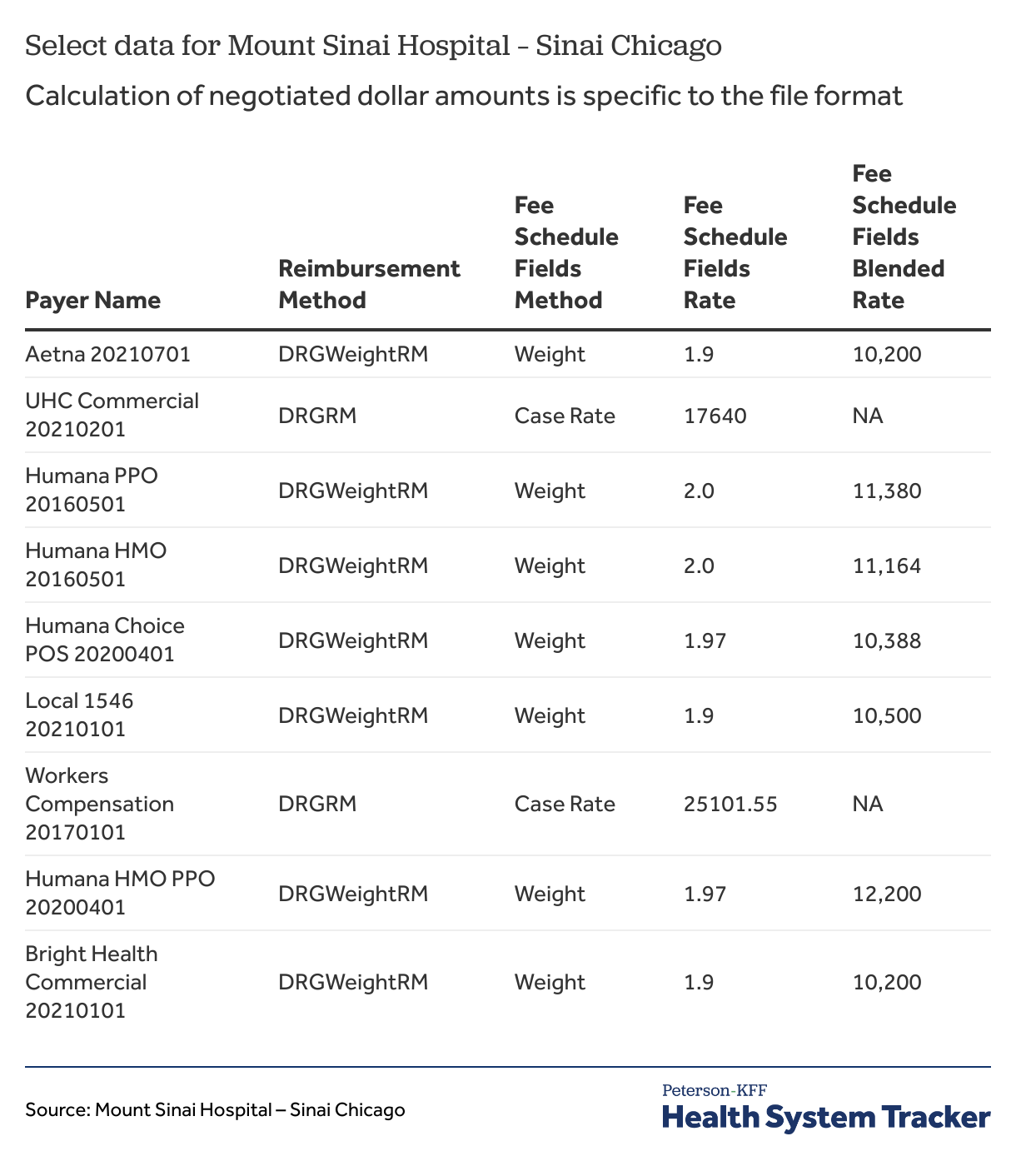

Table 3 shows selected observations from the machine-readable file posted by Mount Sinai Hospital in Chicago, also for hip and knee replacement. In this case, the hospital includes two rate columns and a column for reimbursement methods that shows that these payers have negotiated a DRG-weighted reimbursement. A likely interpretation is that the negotiated rate is the product of the fee schedule fields rate and the fee schedule fields blended rate (e.g., for Aetna, 1.90 x $10,200), but there is no way to be sure other than contacting the hospital. The inclusion of both dollar amounts and factors (percentages) in the same column and reliance on several additional columns to calculate the total rate pose a challenge to creating a correct data set. This is further complicated by non-standardized labeling of columns and unclear documentation of the required calculation to arrive at the negotiated rate dollar amount.

Table 3: Calculation of negotiated dollar amounts is specific to the file format, as shown from Mount Sinai Hospital – Sinai Chicago data

Without clear specifications for the machine-readable file and thousands of hospitals posting machine-readable files each able use its own format and labels, it is difficult to construct an analytic file with comparable information. One way to gain more context is to obtain the original files to investigate how the columns are used, but this does not scale well. Routine statistical operations, such as calculating percentiles and trimming small and large amounts, have to be carefully evaluated considering the heterogeneity of documentation of negotiated rates.

As a final point about episodes of care, there are many millions of charges in these files that do not have any type of discretely documented code associated with them. It is possible that some hospitals have rates for service bundles that can only be identified through the written descriptions provided by hospitals. This can be a challenge because the descriptions hospitals use are neither consistent nor complete. However, with no uniformity across hospitals in the way that this information is structured or labeled, it is difficult for an analyst to capture unless they are focused on only a few hospitals.

Comparing procedure or service codes

Most of the negotiated rates in the data released by hospitals are for specific items or services (e.g., a specific procedure such as an MRI, a specific piece of medical equipment like a stent, a specific prescription drug) rather than for service bundles, and many of these are associated with standardized procedure or product billing codes with meanings that are the same across providers (i.e., CPT, HCPSC, NDC). There also are standardized modifiers for HCPCS and CPT codes that provide additional information when the code would not otherwise describe the care provided. For example, for a procedure with both a professional and a technical component, such as an MRI, a claim with modifier 26 indicates that the claim is just for the professional part and a modifier of TC indicates that the claim is just for the technical part. Some, but far from all, hospitals have included modifiers when associating CPT or HCPCS codes with some of their standard charges.

Using a procedure or product code is generally a good starting point for comparison within or across hospitals, although there are limitations and considerations with this approach. One limitation is that hospital encounters often involve multiple items and services, so any specific code gives only part of the picture about what a particular encounter may cost. This is particularly true for inpatient admissions where there are likely to be many discrete items or services provided to a patient. Additionally, these codes do not include auxiliary fees charged for hospital services provided, such as hospital room and board charges and operating room charges. Due to the heterogeneity in the machine-readable files, some negotiated charges appear to be for certain supplies, medical devices and services but are not associated with codes. Formulating searches relying on words and word fragments alone may not be a very productive approach with all the varied abbreviated descriptions in the observations, particularly if searching over many hospitals.

Much like MS-DRGs, the written descriptions accompanying procedure or product codes can contain important information about the scope of the service provided. This information can be particularly appropriate for services where both a facility and a professional charge are expected. In data from the roughly 4,100 hospitals examined, there are over 490 distinct written descriptions for diagnostic colonoscopy (CPT 45378) among the negotiated rates.

While most of the descriptions contain the words or abbreviations for “colonoscopy” and “diagnostic,” in other cases there are ambiguities:

- Some descriptions are difficult to interpret (e.g., “Additional CPT Code-NRV 750,” “52 Looping – 52,” “27703,” “none”)

- Some may not be comparable to the other observations (e.g., “G0071 Telephone only services by RHC/FGHC 5 min,” “Per Minute 45378,” “Diagnostic Colonoscopy per 15 minutes”).

Many others indicate that the charge is only for a portion of the procedure or that additional criteria may apply to the charge. Examples of these include:

- Hospital/facility charges or physician/professional charges or suggestive abbreviations (“HC,” “HCHRG,” “OR” or “PF,” “PR,” “PRO,” “SURGN”);

- Different charges for people depending on classification as high risk; or

- Negotiated rates for procedures that were aborted (e.g., not proper pre-surgery preparation).

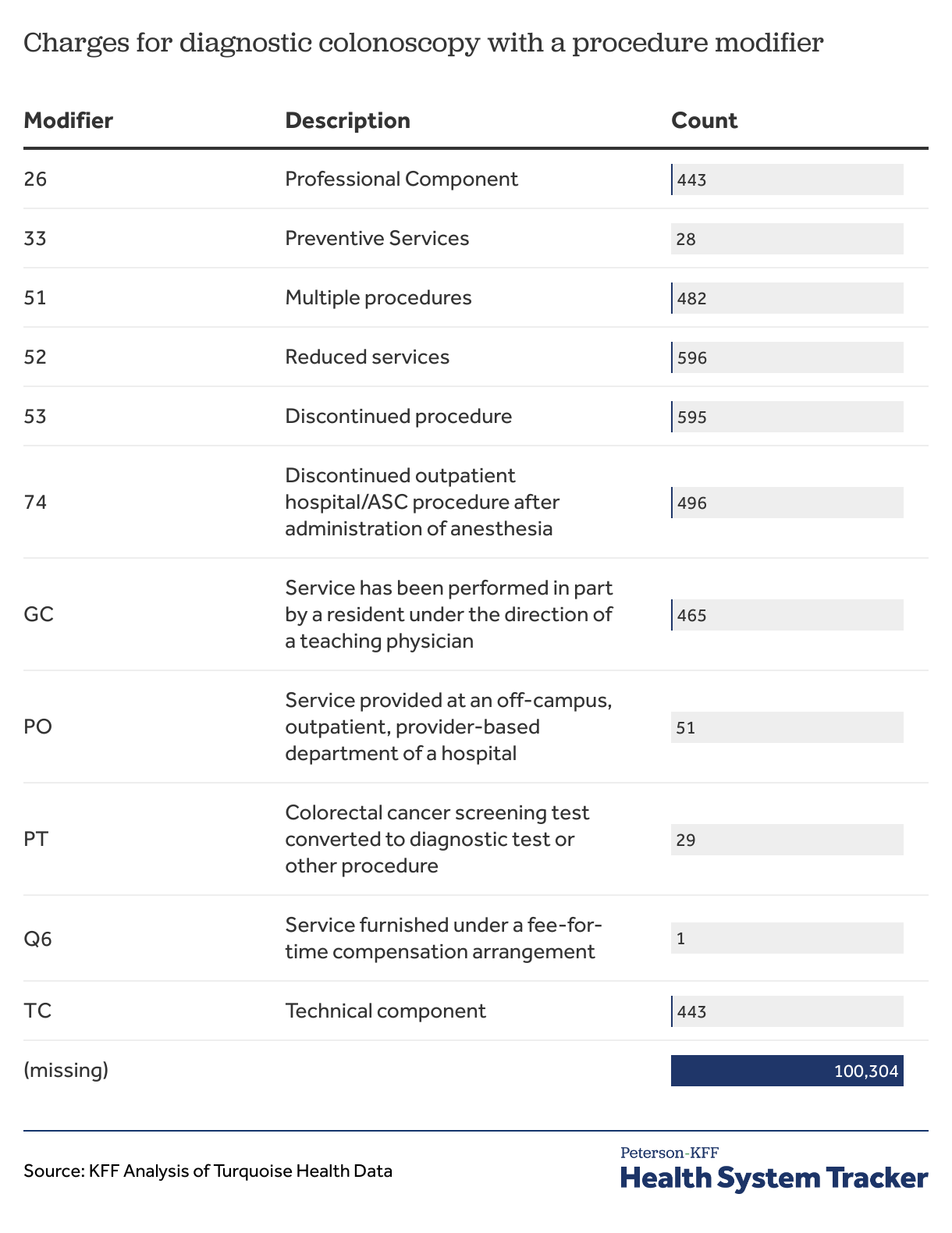

As noted above, CPT/HCPCS codes have modifiers that provide additional information related to a coded item or service that affect pricing and payment. However, few hospitals (23) included a modifier for any of their observations for diagnostic colonoscopy. An examination of the machine-readable files reveals that some hospitals do not even include a field for modifiers in their data disclosures. This means that the absence of a modifier is not necessarily a meaningful factor. Of more than 103,900 negotiated rates for diagnostic colonoscopy, over 100,300 do not have an associated modifier (Table 4). This suggests that, as with MS-DRGs, written descriptions associated with CPT or HCPCS codes are necessary to understand the service the charge applies to.

Table 4: Procedure modifiers are mostly missing

Hospitals may have different charges for the same code based on where in the hospital the item or service is provided. The rule specifically requires hospitals to include all standard charges for inpatient and outpatient services, although it does not specifically require that the charges be labeled as inpatient or outpatient. Some hospitals include this information in their data files, but others do not.

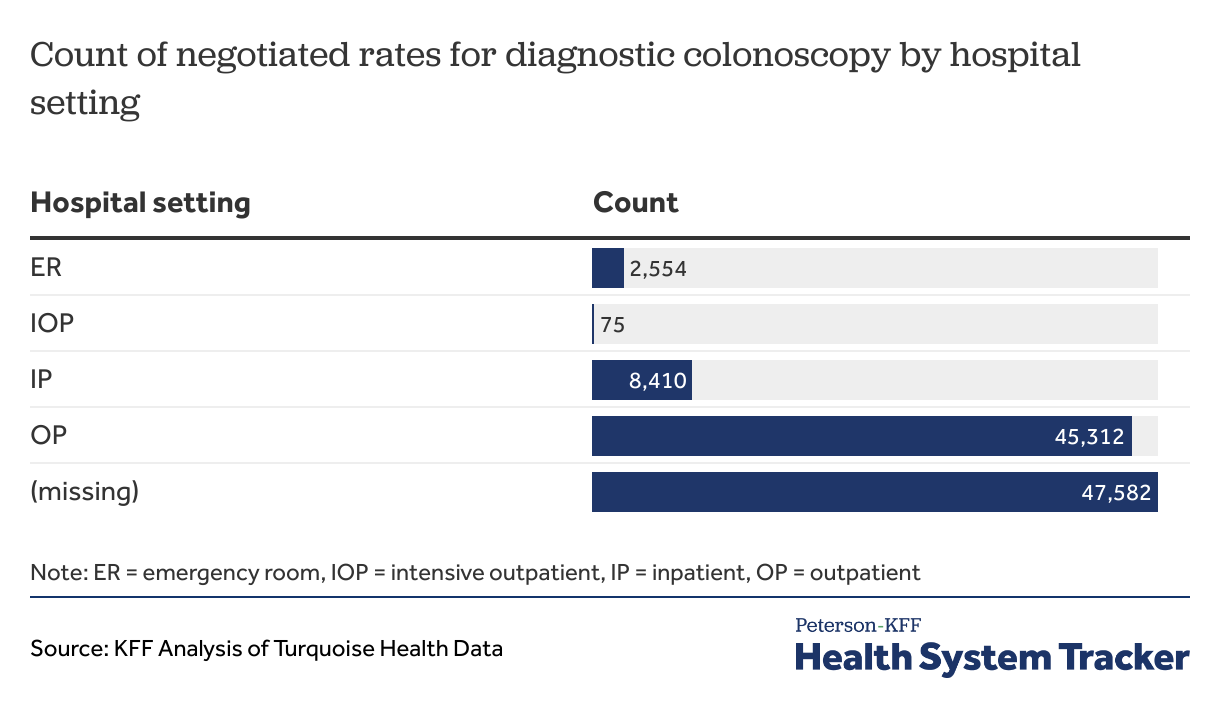

Table 5 shows the number of negotiated rate observations for diagnostic colonoscopy, separated by hospital setting. The Turquoise Health database stores this information, but a large majority of the negotiated rates for diagnostic colonoscopy do not have a specified service area. This can be an issue for interpreting prices of items and services that are delivered in both inpatient and outpatient (or other) settings. For example, the costs for diagnostic colonoscopies are much higher on average in inpatient settings than in outpatient settings. In some cases, the revenue code associated with a negotiated rate may provide additional information. For example, a few of the negotiated rates have a revenue code of 982, indicating that they are outpatient professional fees. As with the modifiers, however, a large share of the observations for this code do not include a revenue code, so it cannot be used to help classify many of the observations. Charge descriptions from the data rarely appear to include information about whether a negotiated rate is for an inpatient, outpatient, or other setting inside of a hospital.

Table 5: Most charges do not specify service setting

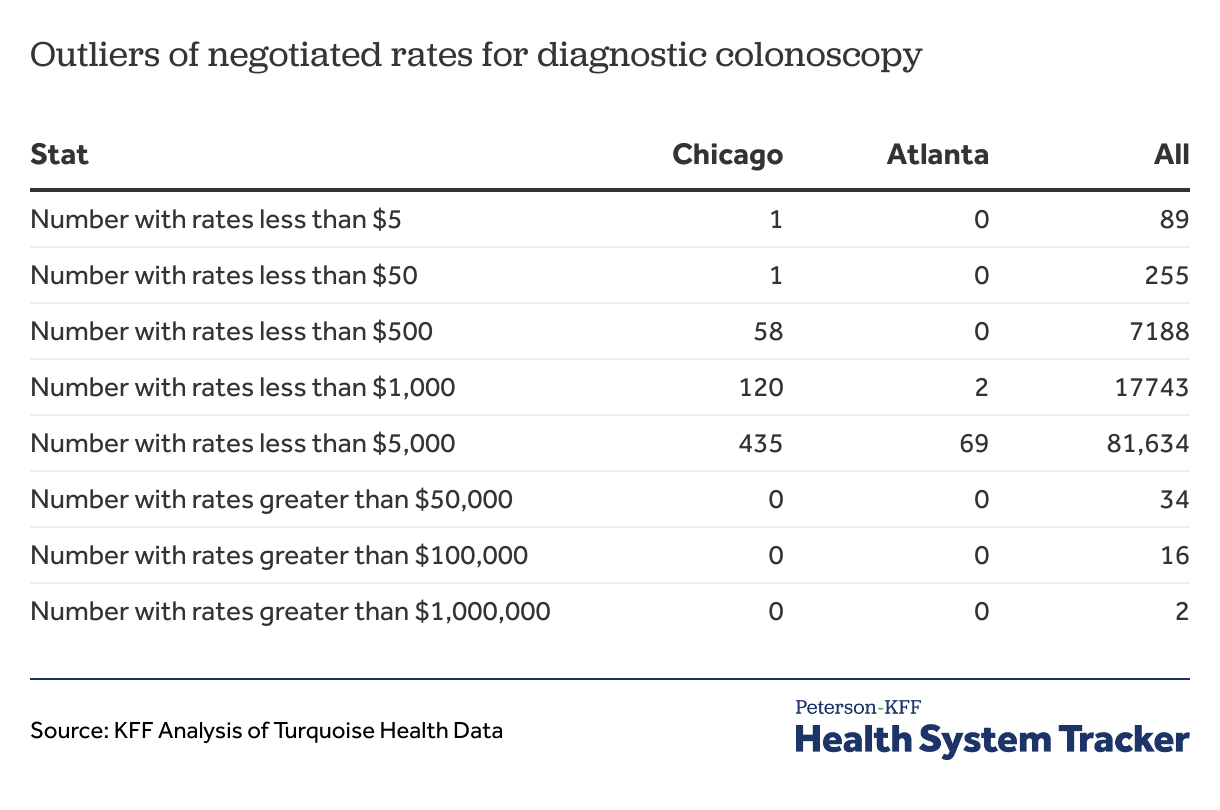

As was seen with bundled services, searching by CPT/HCPCS codes also can result in many observations with negotiated rates that are outside a believable range. Among CPT 45378 charges, there are 123 negotiated rates of less than $10, and 34 that are over $50,000. Even considering some of the issues previously mentioned, such as the difficulties of distinguishing among hospital, professional, and total charges, the extreme low and high amounts raise questions, and those using the data may need to investigate them further.

Assessing health plan types

Rates are negotiated by different types of health plans for different health insurance markets, such as commercial coverage, Medicare Advantage, or Medicaid managed care, which are known to have different levels of hospital payment rates. This means that the expected distribution of rates for any service may be multi-modal, where rates negotiated with Medicaid managed care plans are relatively low and those negotiated with commercial plans are relatively high. There are also differences in negotiated rates with workers compensation carriers, auto insurers, transplant plans, and other programs like Tricare. Examples of these differences are shown in the next section.

Although the rule requires hospitals to include the name of a health plan with each negotiated rate, it does not require hospitals to designate the plan’s market, and it is not always obvious from the plan name. Plans with names that include words like “Medicare,” “Medicare Advantage,” “Commercial,” “Marketplace,” “Medicaid,” and “CHIP” are relatively straightforward to classify. However, many others do not have descriptive words such as these, and quite a few have abbreviations such as “MA” or “MAP,” which may refer to Medicare Advantage plans but could refer to medical assistance plans (i.e., Medicaid).

Additionally, hospitals sometimes include contracts with public agencies (e.g., County of Los Angeles Dept. of Mental Health Uninsured, Covid-19 HRSA Uninsured) as health plan names, likely because they have negotiated rates for one or more items or services with that agency. Analysts may want to consider if and how to incorporate these plans into their analyses.

A related issue is that each hospital uses its own way of referencing each health plan with whom they have negotiated rates, so that even in a local market, different hospitals will have different names for the same health plan. And because each hospital may have multiple negotiated rates with each of the major carriers (e.g., Cigna, Aetna, UnitedHealthcare, Blue Cross and Blue Shield), comparing prices from the same plan across different hospitals can be challenging and requires examination of the plan names used by each hospital and making judgments about which match. It is easier to make comparisons across hospitals at the carrier level (e.g., Cigna, Aetna), although each of the major carriers may have multiple plans in multiple market segments (e.g., commercial, Medicare Advantage, Medicaid managed care) so price comparisons may still be affected by the relative market mixes of the carriers in the markets being examined, as prices vary systematically across segments.

Illustration comparing hospitals in Chicago and Atlanta

In this section we try to give a more accessible look at the data by focusing on the results for two codes in hospitals in two cities. The figures and tables in the appendix examine the negotiated rates for hip and knee replacement and diagnostic colonoscopy for hospitals in Chicago and Atlanta that have negotiated rates for those codes. National estimates for each code are also presented. In each case, we filtered out observations where the descriptions did not match the code but did not investigate or trim outliers. Rates are top-coded at $100,000 for hip and knee replacements and $25,000 for diagnostic colonoscopy in figures showing the distributions for all hospitals to constrain the range for display in a meaningful way.

Hip and knee replacement (MS-DRG 470)

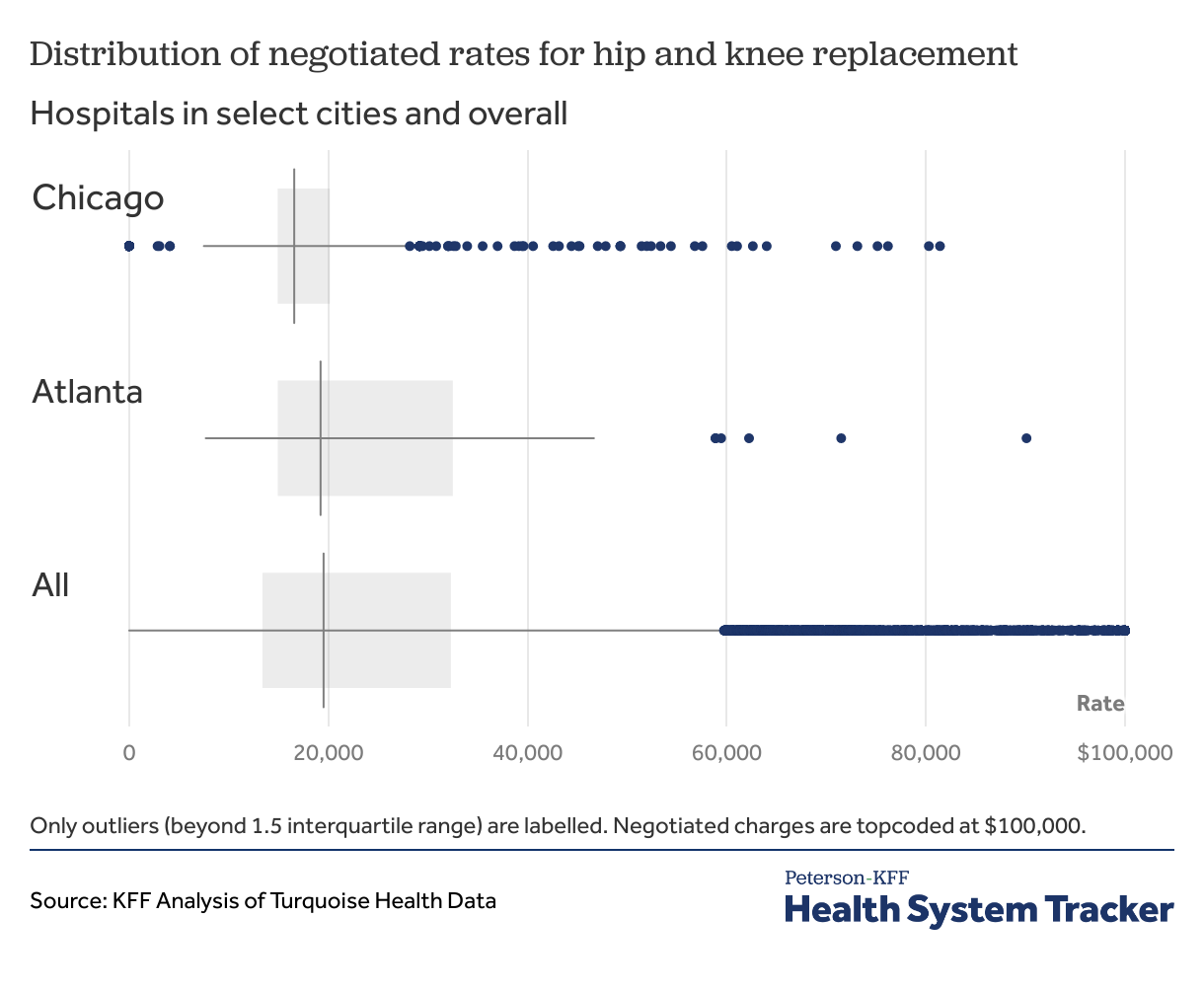

Figure 6 shows the distributions of negotiated rates for hip and knee replacement for Chicago, Atlanta, and nationally. The areas inside the boxes show the ranges between the 25th to 75th percentiles (the interquartile range) in each location, the vertical lines inside the boxes show the median values, and the dots show the most extreme values. The national distribution and the distribution for Chicago have extreme low and high values that seem questionable. The low values for Chicago are likely not dollar amounts — they appear to be factors to apply to a base rate rather than final rates. The higher values are more difficult to explain, as a payer is unlikely to prospectively negotiate a six- or seven-figure amount for a straightforward service.

Figure 6: Negotiated rates for a hip and knee replacement vary greatly within and between markets

The impact of extreme values may matter more when looking at or within certain geographic locations or when trying to understand the reasonable range of negotiated rates for a service or procedure more generally. Making an informed judgement about the validity of these outlier values may require inspection of the machine-readable files of the hospitals in question for additional context to validate specific charges.

The distribution of negotiated rates of Chicago also differs in shape from that of Atlanta. Chicago has lower median negotiated rates, and the mid-range values – those between the 25th and 75th percentiles – are much closer together (i.e., the box is thinner). Understanding why the distributions differ can be challenging, as there are over 800 negotiated rates for just these two cities.

Analyzing differences in rates by coverage type can clarify whether differences across markets or across hospitals occur within a coverage type or are a result of different mixes of coverage across the markets or hospitals being compared.

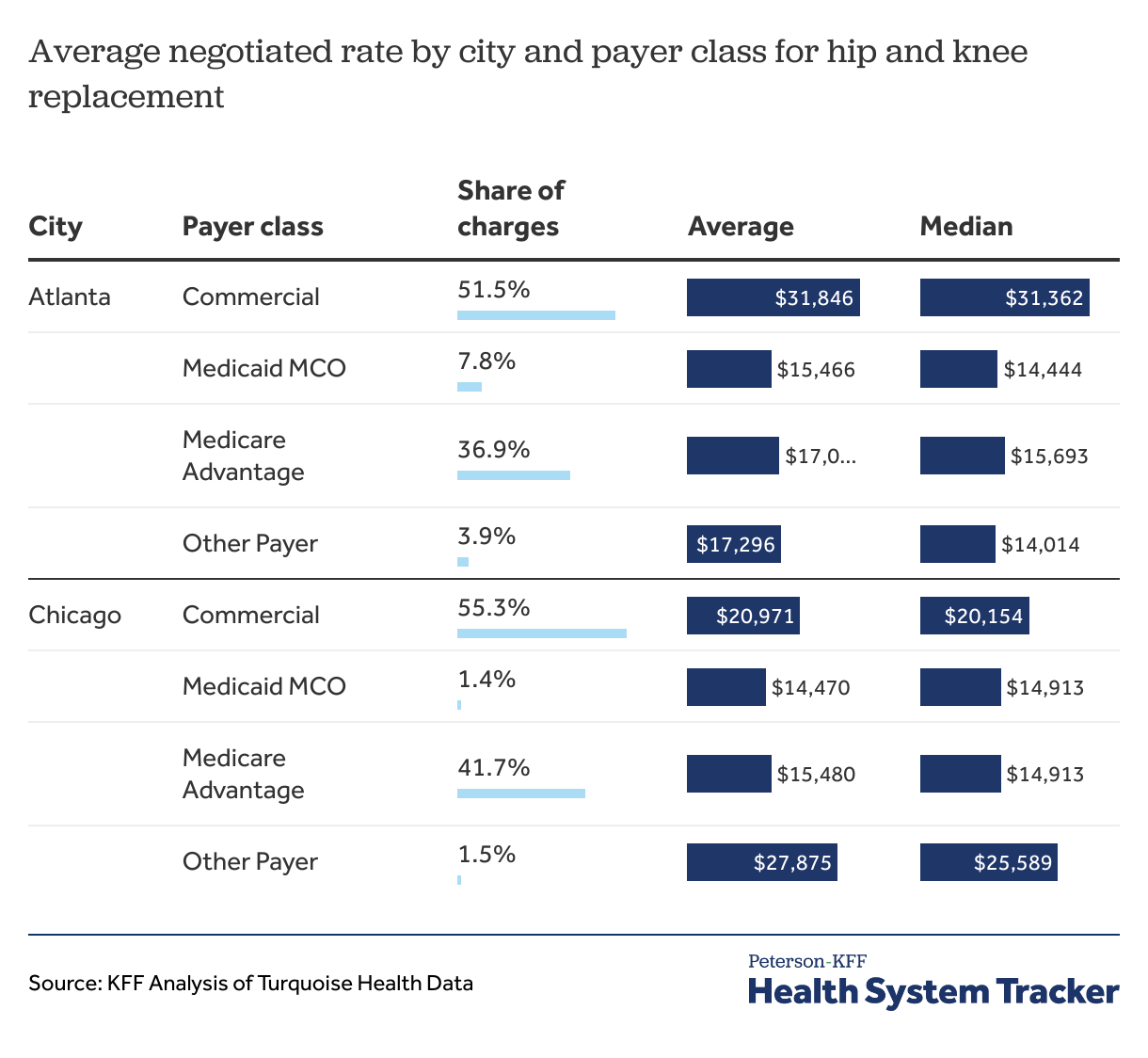

Turquoise Health categorizes each health plan into one of 12 payer classes/insurance markets, including cash and list prices which we are not including in this analysis. Table 7 shows the average and median negotiated rates for hospitals in Chicago and Atlanta, segmented by insurance market. The number and share of negotiated rates for each segment is shown as well. In this case, the commercial share of negotiated rates is roughly the same in each market, as is the combined share of Medicare and Medicaid plans, so market mix is unlikely to explain differences in rates across the two markets. Instead, the difference in average and median rates is largely within the commercial plans: the average negotiated rate in Atlanta is approximately $10,900 higher than the average rate in Chicago and the median negotiated rate is roughly $11,200 higher.

Table 7: Commercial negotiated rates for hip and knee replacement are generally at the higher end of the range

This last point demonstrates another important consideration in using the hospital transparency data to compare rates across hospitals or locations: Calculating statistics based on the number of negotiated rates gives more influence to hospitals that report a large number of rates. Hospitals that provide more granular information in their file (e.g., specified rates for more revenue codes, even when the rate does not vary between revenue codes) may be more heavily weighted in analysis, depending on the technique employed. A large hospital with one negotiated rates will count less in computing an average or a median than a small hospital with five negotiated rates.

This factor helps explain the shape of the distribution of rates in Chicago: hospitals associated with AMITA Health account for 74% of the individual negotiated rates overall, including 59% of the commercial rates and 98% of the Medicare rates. With its large share of observations, AMITA’s rates influence the average negotiated rate for the area. The relatively low commercial negotiated rates at these hospitals, combined with the large number of Medicare rates that are not very far off the commercial rates, result in the tight distribution shown in Figure 6.

In contrast, the negotiated rates in the Atlanta area are more evenly distributed among the hospitals, where the maximum contribution is 25% of the observations. Although the impact of the disproportionate number of rates at certain hospitals can be mitigated (such as employing a weighting scheme), the distribution of observations by provider should not be overlooked.

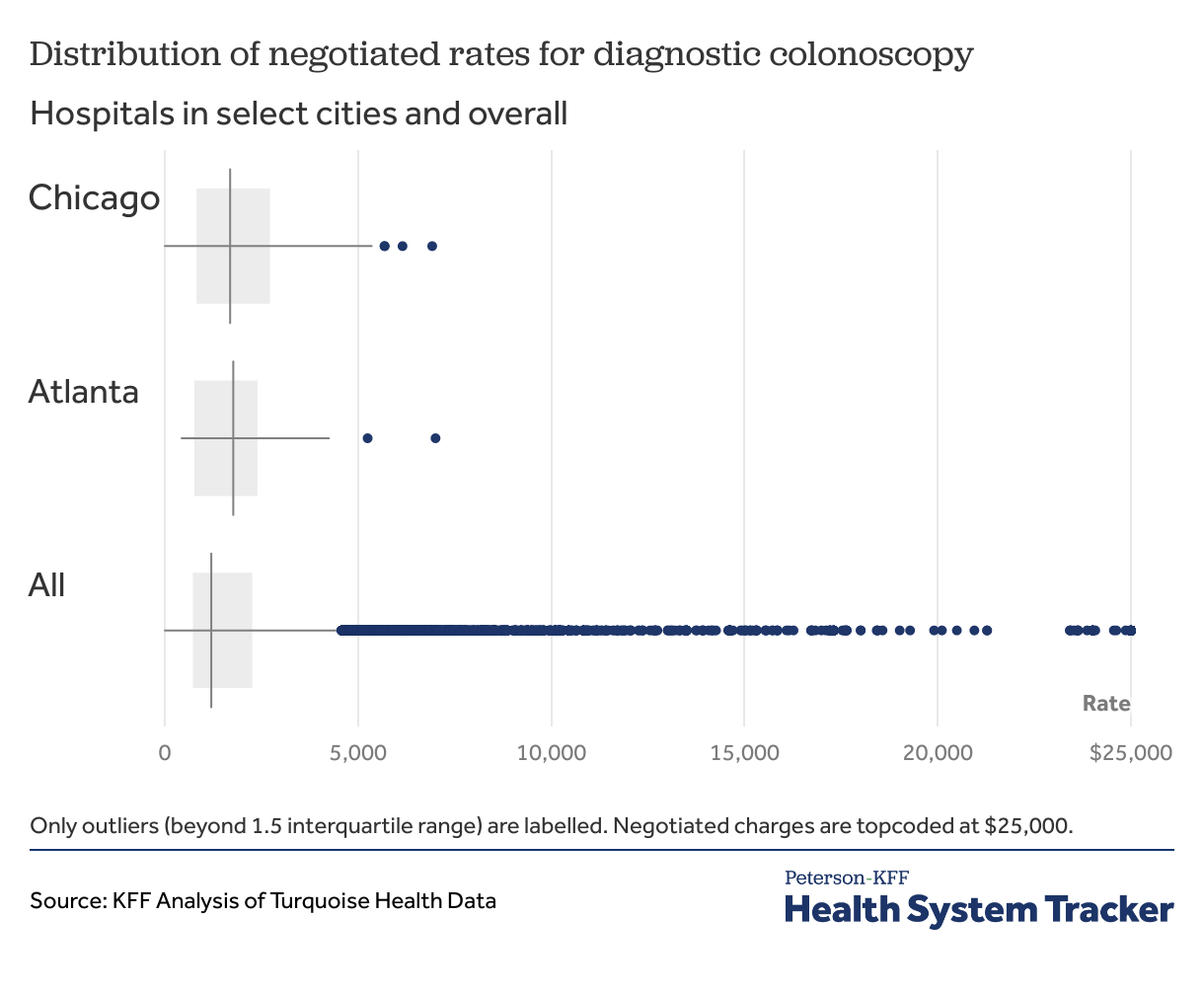

Diagnostic colonoscopy (CPT 45378)

Figure 8: Negotiated rates for colonoscopy vary greatly within and between markets

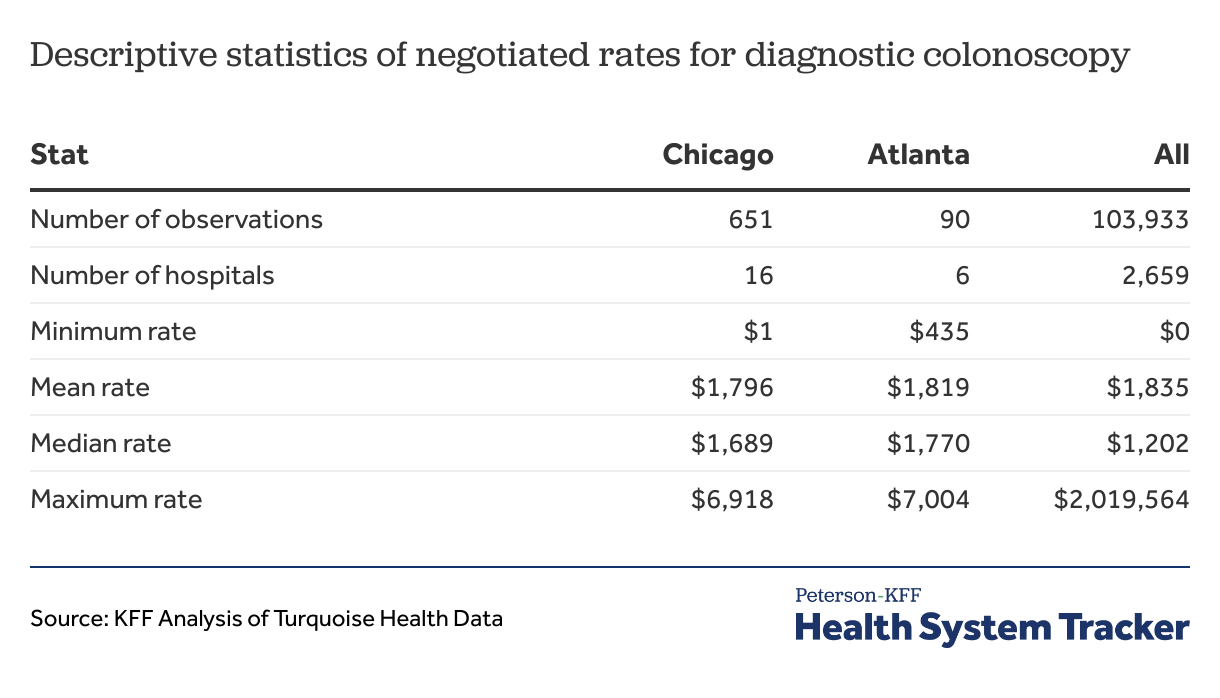

Figure 8 shows the distribution of negotiated charges from the Turquoise Health Data for diagnostic colonoscopy in Chicago, Atlanta and nationally, top-coded at $25,000. In general, the distributions in Chicago and Atlanta look similar, with similar median values. Neither city has any of the extremely high values seen in the national distribution. There are, however, several additional factors to consider when examining the charges in these two markets.

Of the 22 hospitals with negotiated charges in these two cities, eight have more than one negotiated charge for the same health plan. Possible explanations include different charges by services area in the hospitals (e.g., inpatient or outpatient) or different services coded with the same charge.

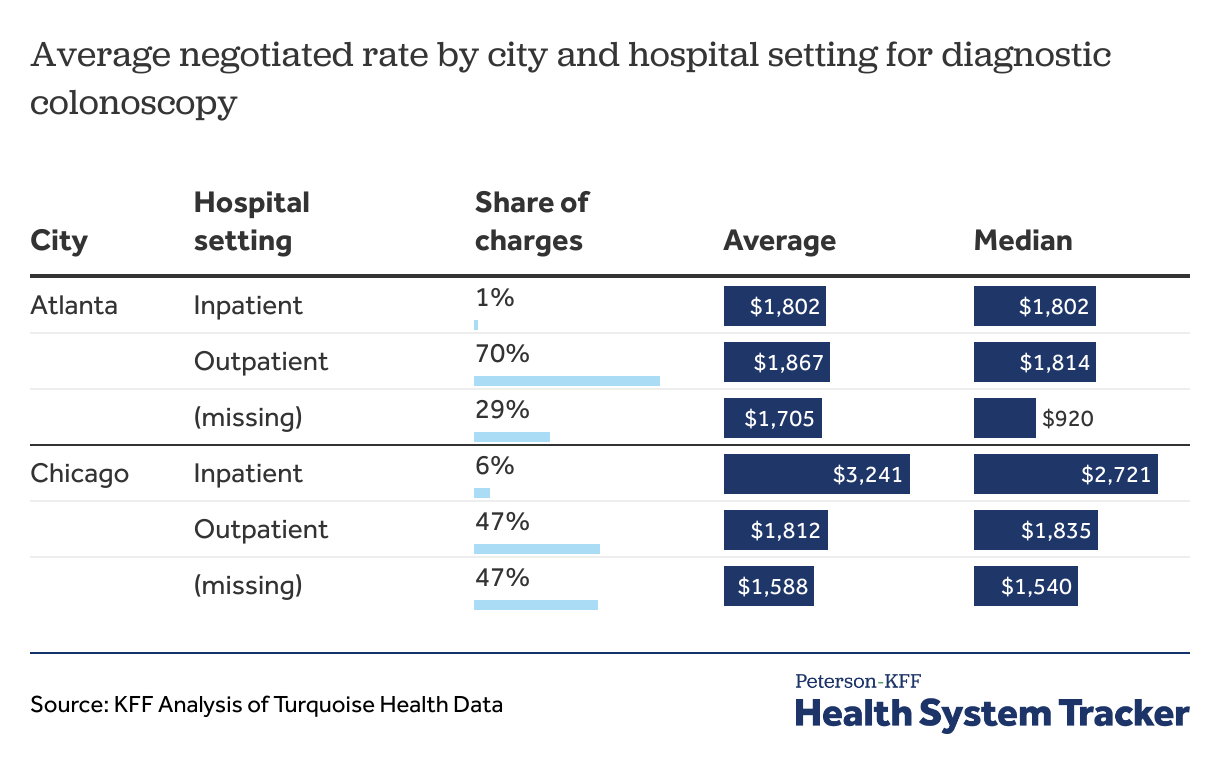

Table 9 shows the average and median charges for each city by hospital setting. Hospital setting is missing for approximately half of the negotiated charges, complicating the interpretation of the data. In fact, service area is missing from all the negotiated charges in one hospital in Atlanta and in eight hospitals in Chicago.

Table 9: Service area is missing from many negotiated charges

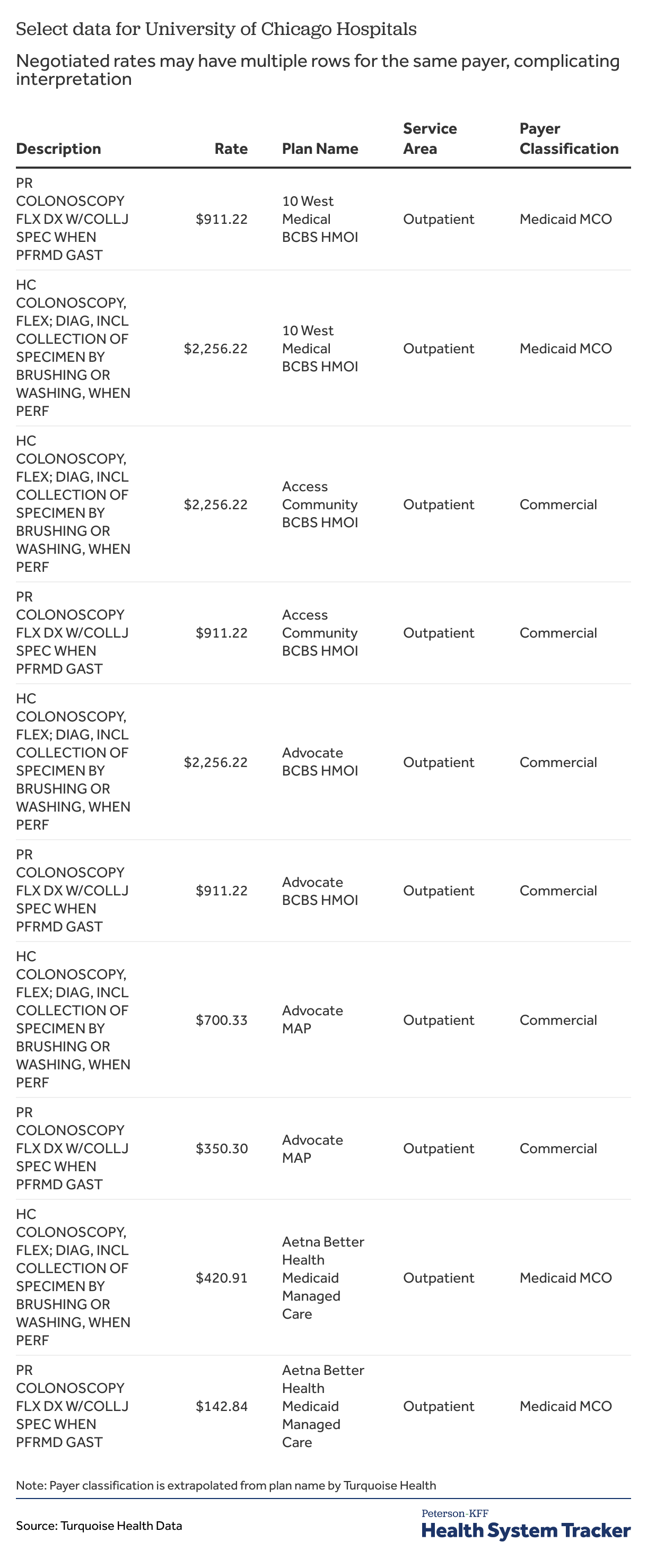

In at least one hospital, the multiple negotiated rates per plan are for different types of services. As we noted above, many services, including diagnostic colonoscopy, have both professional and facility components. Table 10 shows several observations for this charge from the University of Chicago Hospitals. There are two rows for each health plan, one suggesting a hospital charge and the other a professional charge.

Table 10: Negotiated rates may have multiple rows for the same payer, complicating interpretation, as shown from University of Chicago Hospitals’ data

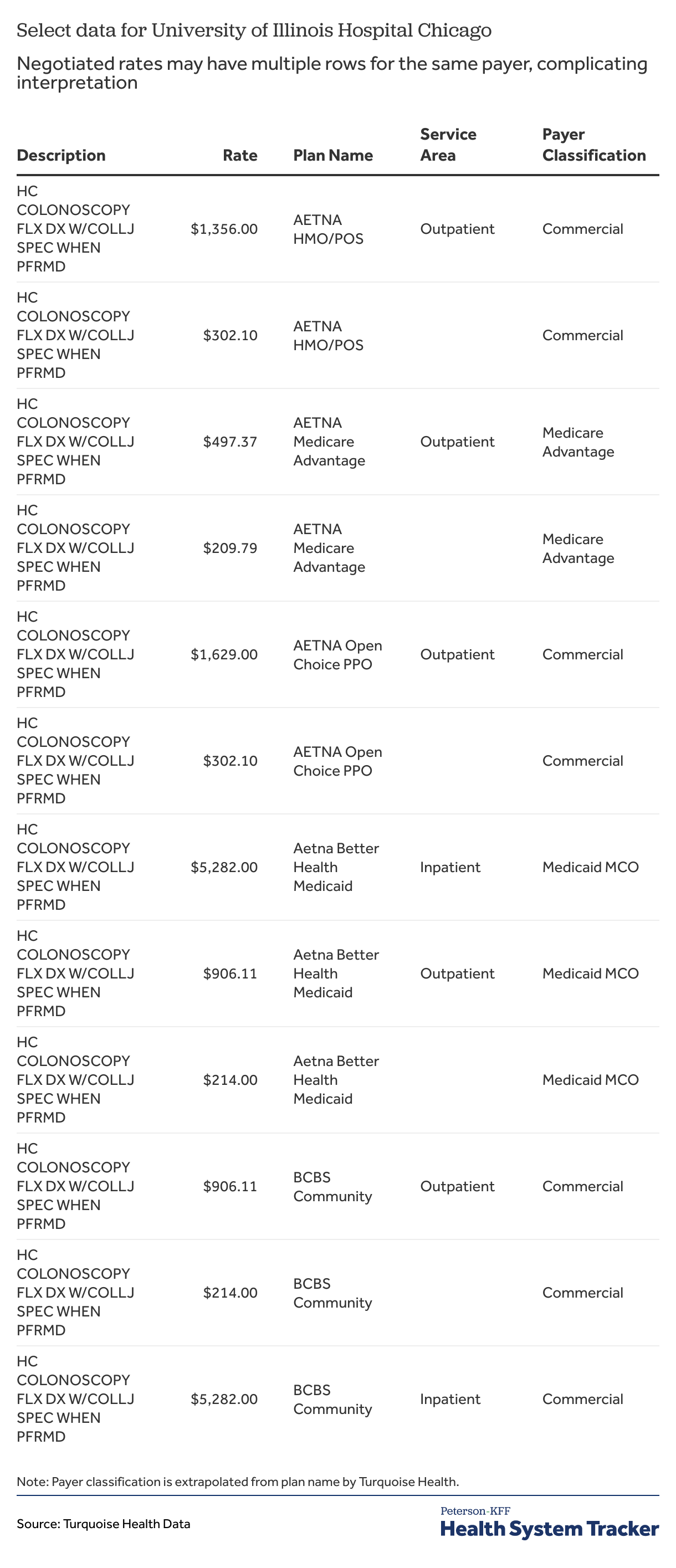

Observations from another hospital, the University of Illinois Hospital, show two or three hospital charges for each health plan (Table 11). In some cases, there are separate charges for different hospital service areas, but in all cases, there is a separate much lower hospital charge that is not labeled with a service area. Inspection of the machine-readable file confirms that each row corresponds to a different rate class (facility/professional) and rate type (per case, fee schedule) combination. Two additional hospitals, Mount Sinai and Holy Cross Hospitals in Chicago, have two negotiated charges for many health plans, but the descriptions are the same for each charge and there is no service area or other information in the Turquoise Health data to clarify how the two charges relate to one another. Examination of the source machine-readable file from Mount Sinai shows that the rates may refer to non-overlapping time periods, but this is not standardly specified from all hospitals.

Table 11: Negotiated rates may have multiple rows for the same payer, complicating interpretation, as shown from University of Illinois Hospital data

Another factor to consider when examining the charges for these two cities are the much lower than average rates for two related hospitals: Mount Sinai and Holy Cross Hospitals in Chicago. The average and median negotiated rates in these hospitals are less than one-half of those of the next lowest priced hospitals. These hospitals have a rather complex format in their data files, so it is possible that there is additional information on these charges in the original data that is not ingested into the Turquoise Health data set. Or, it may be the case that the two charges for most health plans for this code are additive, which would bring the total more in line with the low end of the other hospitals in the Chicago market. In any case, these low charges may warrant additional investigation, and illustrate how analytic results can be misleading without delving into the details of the data.

Discussion

The price transparency rule has made a very large volume of new information on hospital prices available to the public. Requiring that the data be available in a downloadable format means that researchers can gain access to and explore the information for select hospitals, and that entrepreneurs, such as those at Turquoise Health, can create larger databases bringing together information from hospitals posting machine-readable files. This is an unprecedented opportunity for the public to learn more about how hospital prices vary within markets and across different payers.

Much of the discussion of the hospital transparency data has focused on whether hospitals are complying with the rule and making data available to the public, a reasonable first step in assessing the data. In this brief, we took a different approach—focusing on the usefulness of the data that is available. We examined negotiated prices for two common procedure codes to demonstrate some of the challenges associated with using this information. We identified situations where data were ambiguous, missing, or difficult to find. Lack of clarity in what services are included in a charge, how prices are defined and presented, and how plans are identified make it difficult to compare prices across or even within hospitals and regions.

The issues discussed above result primarily from the way the rule is crafted, particularly from the lack of specificity and uniformity about what should be included with each charge in their machine-readable files and how that information should be laid out. There are no standards for what needs to be included in the description or whether codes should include commonly used modifiers. Although providers are required to include de-identified minimum and maximum negotiated charges, lack of standardization for how these are labeled in the data result in difficult isolation of these values for use in further analysis.

To improve usability of the data, additional information about the context and scope of each charge would be important. Some of the challenges in interpreting the price transparency data can be addressed by uniformly requiring additional data elements to accompany each charge. The following characteristics are examples of elements that would assist in analysis:

- The hospital setting applicable for the charge, e.g., whether it is an inpatient or outpatient charge. Although the rule requires that charges be disclosed for each item and service delivered in an inpatient or outpatient setting, it does not specify that the service area be associated with the charge. Some home hospitals do include this information for each charge, but the number of instances where that information is missing or not applicable in the Turquoise Health Data suggests that not all hospitals do include or it or that it is difficult to find in their machine-readable files.

- Whether the charge is a facility or professional charge. As discussed above, many codes have one or more professional components and one or more facility components. These could be bundled into one charge or charged separately. It is difficult to understand or use a charge in a comparison without knowing this information.

- Whether the code for a charge is associated with a modifier or not. CPT/HCPCS codes have common modifiers that provide additional context to the charge that explains why the code does not adequately describe the service that is being provided. Including this information would provide additional context to understand if a charge is different from other charges associated with the same code. In characterizing prices associated with a procedure, charges corresponding to an aborted procedure (identified with a modifier) could then be analyzed separately as needed.

- The type of charge, in particular whether it is a per case charge, a per diem charge, or a percent of charges (and if so, what charge is it a percent of). To compare like charges to like charges, you need to know what they represent, but this information is not always easy to find or access in hospital downloadable files, if it is there at all.

- Whether the charge is a bundled rate or not. Some charges are for more than one service and some are not. While this information should be apparent for some codes, such as for MS-DRGs, there are instances where hospitals have associated charges for just anesthesia services with an MS-DRG. There also are charges that some hospitals associate with an MS-DRG that are per diem charges or even a percent of some other charge. A more specific set of data elements specifying these parameters would allow users to have a better understanding of what the charge is for.

- The contracting method, whether a charge is the total charge or a base rate. In some cases, a negotiated charge is calculated by multiplying an identified base rate by one or more factors. Factors may be based on the characteristics of the enrollee using the service, such as their age, gender, or a risk characteristic. Comparing charges based on case rates to those based on base rates can be misleading if the factors used with the base rates are large.

- The type of health plan with which the rate is negotiated. Evaluating a charge is difficult without knowing the plan market, as charges for commercial plans are generally higher than charges for public plans, such as Medicare Advantage plans and Medicaid managed care plans. The type of plan is not always apparent from the plan name and many carriers have multiple types of plan in a location. There is no central database of health plans, much less of plans categorized by plan type, so undertaking to classify them by type can be a significant undertaking. This is particularly challenging when analyzing multiple markets or trying to derive national estimates. Turquoise Health categorizes each plan into one of 12 groups, which is one of several advantages to using their database. As this is information that hospitals have (or could easily have), however, this is a data element that could easily be included in the machine-readable file.

CMS has recently published price transparency resources, including data dictionaries and data format layouts, to support submission in one of three machine-readable formats. The specifications described in these address many of the issues raised here by inclusion of some of the suggested elements. However, hospitals’ use of these resources remains voluntary. Until there is more standardization in how machine-readable files are organized and made available, analysis of these data will be challenging. More fundamental issues surrounding what is included in a negotiated charge remain.

While not perfect, the price transparency rule succeeds in moving toward having data available to understand the breadth and variation of negotiated charges between payers and providers. However, it is important that researchers and analysts using price transparency data collated from the machine-readable files assess how inconsistent and complicated formats affect data integrity, as well as how the lack of consistency in the data can result in unreliable findings.

Appendix

The Peterson Center on Healthcare and KFF are partnering to monitor how well the U.S. healthcare system is performing in terms of quality and cost.