Note: This brief was published on August 6, 2025 reporting proposed 2026 rates. It was updated on January 15, 2026 to include a new table of approved 2026 rates in the Appendix.

Health insurers submit rate filings annually to state regulators detailing expectations and rate changes for Affordable Care Act (ACA)-regulated health plans for the coming year. A relatively small, but growing, share of the population is enrolled in these plans (compared to the number in employer plans), fueled by the availability of enhanced premium tax credits. This analysis focuses on individual market filings, which are generally more detailed and publicly available. These filings provide insight into what factors insurers expect will drive health costs for the coming year.

For 2026, across 312 insurers participating in the ACA Marketplaces from the 50 states and the District of Columbia, this analysis shows a median proposed premium increase of 18%, which is about 11 percentage points higher than last year. This is the largest rate change insurers have requested since 2018, the last time that policy uncertainty contributed to sharp premium increases. On average, ACA Marketplace insurers are raising premiums by about 20% in 2026. Based on a more detailed analysis of available documents from insurers in 19 states and the District of Columbia, like in prior years, growth in health care prices stood out as a key factor driving costs in 2026. Insurers cite increasing cost and utilization of high-priced drugs as well as general market factors, such as increasing labor costs and inflation, as contributing to premium increases.

In addition to rising healthcare costs, the majority of insurers are also taking into account the potential expiration of enhanced premium tax credits in their premium rate increases for the next year. The expiration of enhanced tax credits will lead to out-of-pocket premiums for ACA marketplace enrollees increasing by an average of more than 75%, with insurers expecting healthier enrollees to drop coverage. That, in turn, increases underlying premiums. Other federal policy changes, like the implementation of tariffs and the ACA Marketplace Integrity and Affordability rule were also discussed, though to a lesser extent.

ACA Marketplace insurers are proposing a median premium increase of about 18% in 2026

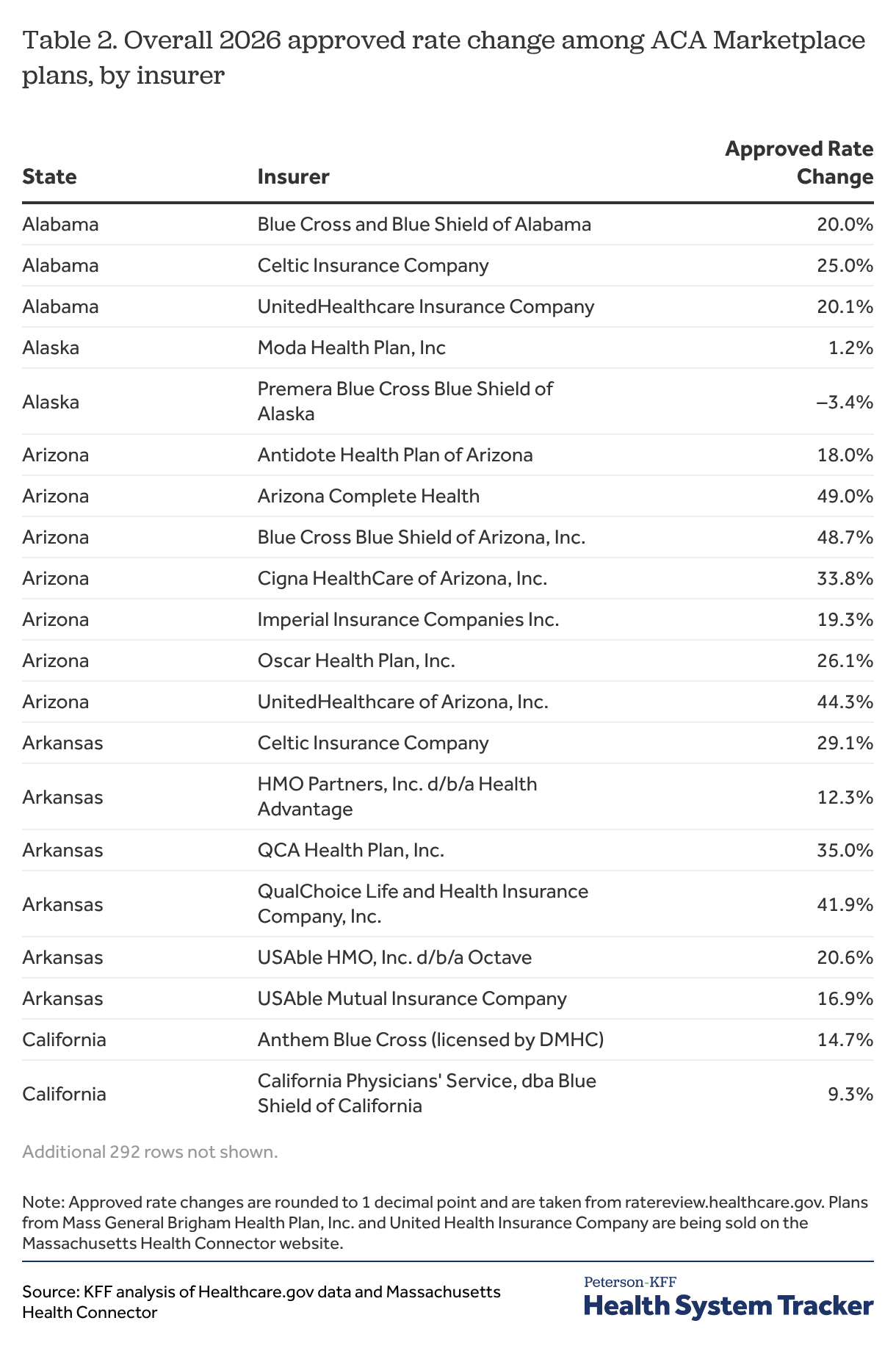

Among the 312 ACA Marketplace participating insurers nationally, premium changes range from -10% to 59%, but most proposed premium changes for 2026 fall between about 12% and 27% (the 25th and 75th percentile, respectively). Of the 312 insurer filings, 4 insurers proposed decreasing premiums. At the other end of the spectrum, 125 insurers requested premium increases of at least 20%. These filings are preliminary and may change during the rate review process. 2026 rates will be finalized in late summer. A table in the appendix shows proposed premium increases by state and insurer.

Related Content:

There are a number of ways to assess premium changes in this market. In this analysis, a premium increase for a given insurer is its enrollment-weighted average of rate changes across all of its products within a state (i.e., bronze, silver, gold and platinum plans). These weighted average premium changes differ from the percent change in the benchmark silver plan, which is the basis for federal subsidies. In 2025, the median proposed rate increase was 7%, while the average increase in benchmark silver premiums was 4% in 2025. The vast majority of ACA Marketplace enrollees (92% in 2025) receive a subsidy and may not expect to face these premium increases depending on the plan they select. However, the potential expiration of the enhanced premium tax credits would decrease financial assistance across the board for all subsidized enrollees, leading to a more than 75% increase in average out-of-pocket premium payments. All else equal, premium increases generally result in higher federal spending on subsidies.

What is driving 2026 premium changes?

Figure 1 above shows premium changes for 312 insurers across all 50 states and DC. For the subsequent sections, this analysis focuses on a subset of rate filings (105 insurers across 19 states and the District of Columbia), reviewed in more detail to better understand the factors driving premium changes in 2026. Across the 19 states and DC reviewed in this section, insurers have somewhat lower proposed rate increases, with a median of 15%.

Rising healthcare costs

Trend

As in in most years, rising healthcare costs – both the price of care and increased use – are driving increasing rates. The costs of health care services like hospitalizations and physician care, as well as prescription drug costs tend to go up every year, and insurers often raise premiums to cover their increased costs. For 2026, insurers commonly say the underlying cost of health care (medical trend) is similar to last year’s reported 8%.

“The increasing cost of medical care is a significant driver of the rate change. This filing reflects the projected claims expenses increasing approximately 10% annually. About 7% of this increase is due to cost and utilization changes.” – Regence BlueCross Blue Shield of Oregon (Washington)

“The underlying claim costs are expected to increase from 2024 to 2026, which is reflective of anticipated changes in the prices of medical services, the frequency with which consumers utilize services, as well as any changes in network contracts or provider payment mechanisms.” – Cigna HealthCare of Georgia, Inc. (Georgia)

Inflation

A small number of insurers have also cited general economic inflation as a driver of higher administrative and internal operating expenses. This inflationary environment places healthcare systems and providers under increasing financial strain, which contributes to increases in premiums.

“Blue Cross VT base administrative charges are increasing as compared to the 2025 approved rates, mostly due to inflationary pressures (see section 3.8.7), increasing premiums by 0.2 percent for individuals and 0.4 percent for small groups.” – Blue Cross Blue Shield of Vermont (Vermont)

Labor costs, contracting, and provider consolidation

A number of insurers also cite healthcare labor costs – driven by persistent clinical workforce shortages and broader inflation – as a meaningful contributor to rising healthcare costs and 2026 premium increases. Providers are seeking higher reimbursement rates in negotiations, citing elevated staffing costs and continued post-pandemic financial difficulties, which insurers incorporate into their trend assumptions.

“Like other payers, Moda is experiencing pressures on multiple fronts related to health care worker labor shortages. With providers experiencing post-pandemic inflationary pressures, they are seeking increases that generally exceed previous years’ requests.” – Moda Health Plan (Oregon)

“Physicians and hospitals are facing economic pressures caused by supply chain shortages, overall inflation and continued workforce challenges. As a result, providers are seeking higher reimbursement for their services.” – Health New England, Inc. (Massachusetts)

In a handful of filings, insurers also point to provider consolidation, through hospital mergers and acquisitions, as contributing to higher contracted prices for services and reduced innovation due to increased provider market power.

“Many systems are asking for large increases for services (some requesting and receiving double-digit annual increases) and have shown a willingness to allow our contracts to expire. Because of the limited competition and regional monopolies, some health care providers have achieved, there is reduced market pressure for these systems to innovate new, more efficient practices.” – LifeWise Health Plan of Washington (Washington)

GLP-1s and specialty medications

Growing demand for GLP-1 drugs such as Ozempic and Wegovy is contributing to increased prescription drug spending. Insurers in the ACA Marketplace frequently apply utilization management policies like prior authorization and quantity limits to manage the high costs of GLP-1 drugs, which are used for diabetes treatment and weight loss. Several insurers point to continued high utilization of GLP-1s (which gained popularity in recent years) as a driver of increased trend and premiums.

“We expect utilization and script mix to increase by 18 percent in 2025 and seven percent in 2026. These trends are mostly driven by oncology and anti-diabetics, including significant growth in GLP-1 medications such as Ozempic.” – Kaiser Foundation Health Plan of Washington (Washington)

“MVP has seen rapidly increasing utilization of Glucagon-like peptide-1 (GLP-1) drugs throughout 2024. This is caused by rapidly increasing demand and has been exacerbated by supply shortages (themselves caused by that increased demand). Across all of MVP’s Vermont commercial population, total allowed costs for GLP-1 drugs (inclusive of both anti-diabetic and anti-obesity categories) have risen approximately 25-30% per quarter for each quarter of 2024, and the 4th quarter of 2024 is now nearly double the total cost of the drugs in 2023.” – MVP of Vermont (Vermont)

In response to the high costs of these medications, some insurers are beginning to remove coverage for GLP-1s for weight loss purposes, contributing to a decrease in premiums. This would impact some of the 45.8 million adults under 65 with private insurance, in both individual and employer plans, who are clinically eligible for these drugs and are obese.

“In 2024, five GLP-1 drugs accounted for over $300 million in spend. Drug makers’ prices for these medications have led to an unsustainable increase in the cost of coverage for our members. In response, BCBSMA is affirming its commitment to affordability and discontinuing coverage of GLP-1 medications for weight-loss indications in 2026. This change has an effect of reducing premium rates in 2026 by approximately 3% for our Merged Market members.” – Blue Cross Blue Shield of Massachusetts (Massachusetts)

Beyond GLP-1s, other high-cost specialty drugs like biologics and gene therapies are also increasingly prevalent and are contributing to rising premiums in 2026. Some insurers explicitly cited specialty drugs as a key driver of rising healthcare costs or pharmacy trends. These drugs and treatments are often characterized by high prices, a small number of users, and a lack of more affordable alternatives, all of which are placing mounting costs on both insurers and consumers.

“High Rx cost trends are driven by the increased prevalence of specialty drugs in the market, new specialty drugs expected to be introduced, the high cost per specialty prescription, and the lack of low-cost substitutes for these drugs.” – BridgeSpan (Oregon)

“Even with the exclusion of anti-obesity GLP-1 coverage, the pharmacy trend remains above double digits. This is largely due to a shift in utilization toward brand-name and specialty drugs, including some newly approved high-cost cell and gene therapies.” – WellSense Health Plan (Massachusetts)

“However, the savings trend associated with generics is being eclipsed by another trend around the rising cost and utilization of specialty medications including biologics…Specialty medications are used by approximately 2 percent of our members, but they account for more than 50 percent of total drug spend.” – Excellus Health Plan, Inc. (New York)

Tariffs

Tariffs could potentially put upward pressure on the costs of pharmaceuticals and medical supplies, driving premiums upward in 2026. However, there is considerable uncertainty about how these trade policies will impact medical pricing, and insurers vary in how (or if) they factor tariffs into their rate development.

A handful of insurers acknowledge the possibility of cost increases due to tariffs, but say they are not adjusting their 2026 rates at this time. One insurer cites a lack of clear evidence and timing around implementation.

“The 2026 individual rate filing does not include an adjustment for the impact of potential tariffs. This is a dynamic situation with proposed tariffs changing on an almost monthly basis. Therefore, we are not accounting for new tariffs until the situation becomes more stable.” – Kaiser Foundation Health Plan of the Northwest (Oregon)

Other insurers are taking a more cautious approach by applying modest upward adjustments to their trend assumptions to hedge against potential cost increases, particularly in pharmaceutical manufacturing and distribution. On average, insurers that cite tariffs as a factor are raising premiums an additional 3 percentage points higher than they would be without these new tariffs.

“New tariffs on goods imported into the United States could have large impacts on medical cost and utilization trends; however, the anticipated impacts for 2026 are uncertain at this time. This filing assumes the CPI-U released in September will be 0.5% higher than the CPI-U released in April for purposes of developing facility cost trend factors. We also estimate a 3% increase to Pharmacy cost trends. There are no other tariff considerations factored into this filing.” – Blue Cross Blue Shield of Rhode Island (Rhode Island)

Federal policy changes

Expiration of enhanced premium tax credits

Uncertainty over federal policy changes has forced insurers to make some assumptions when developing their rates for 2026. Commonly mentioned by insurers is the impact of the expiration of enhanced premium tax credits, which are scheduled to sunset at the end of 2025, unless extended by Congress. The majority of insurers have assumed that enhanced tax credits will expire at the end of this year, driving rates an average of 4 percentage points higher than they otherwise would be. These increased rates are due to insurers anticipating that some healthier members will leave the ACA Marketplaces when their subsidies decrease, creating an enrollee base that is less healthy and more expensive on average.

“An adjustment of 1.044 was applied to account for the expiration of enhanced premium subsidies passed under ARPA and extended by the Inflation Reduction Act (IRA). Due to the expiration of the enhanced premium subsidies effective 1/1/2026, UHC anticipates a decline in enrollment due to higher post-subsidy premiums. Healthier members are expected to leave at a disproportionately higher rate than those with significant healthcare needs, increasing market morbidity in 2026.” – Optimum Choice – United HealthCare (HMO) (Maryland)

Uncertainty over whether enhanced tax credits will be available in 2026 has led some insurers to calculate rate increases for each scenario. In other states like Illinois, Maryland, Rhode Island and Washington, insurers submitted a second set of rate filings that assumed the enhanced tax premium credits would be extended (which are not reflected in our analysis of average premium increases). For example, Neighborhood Health Plan of Rhode Island proposed a 16% increase in an alternate filing that assumes enhanced tax credits will continue, compared to a 21% rate increase in their primary filing. Regulators in other states, like Indiana and Michigan, did not mandate a complete set of alternate rates but still requested that insurers provide the rate impact if enhanced tax credits continue within the primary rate filings. In Connecticut, insurers were instructed by state regulators to file rates assuming that enhanced tax credits would continue. Even so, insurers in Connecticut still provided rate impact information for the opposite scenario.

“Anthem has included a 3.7% morbidity impact that will need to be applied to the rates in the event of enhanced subsidy expiration.” – Anthem Health Plans (Connecticut)

2025 Marketplace Integrity and Affordability Rule

Some insurers also mention the ACA Marketplace Integrity and Affordability rule, which was initially proposed in March and finalized in June. Most insurers that estimate the ACA Marketplace Integrity and Affordability Rule’s impact on rate filings say it will have a small effect, if any.

“On March 10, 2025, the Centers for Medicare & Medicaid Services (CMS) issued the “Marketplace Integrity and Affordability Proposed Rule” which revises standards in enrollment, including eligibility of enrollees and the timing of open enrollment periods. MVP has analyzed the rule and believes that these standards will encourage lower-cost, healthier members to be more likely to forego coverage. This will increase costs on the individual market as a whole. As a result, MVP has adjusted their market wide index rate by a factor of 1.0025…” – MVP Health Plan, Inc. (New York)

A small number of insurers expect that provisions in the rule will push healthier enrollees out of the ACA Marketplaces, leading to a less healthy and higher-cost enrollee base. Other insurers noted the rule’s changes to the de minimis actuarial value (AV) thresholds, which could increase cost sharing for consumers, when developing their rates. In Washington, insurers were specifically instructed not to account for the provisions of the then-proposed rule in their rates.

“An adjustment has been included to reflect the anticipated impact of the proposed CMS Program Integrity Rules, which largely tighten the eligibility requirements for maintaining premium tax credits. These changes are expected to further magnify the enrollment deterioration beyond the impacts of premium tax credit expiration. Average morbidity of the individual risk pool will thereby worsen due to the coverage lapses of relatively healthy individuals.” – Fidelis (New York Quality Healthcare Corporation) (New York)

“Additionally, these rates assume that CMS’ Marketplace Integrity and Affordability rule, published in the Federal Register on March 19, 2025, is finalized as proposed – including key rule changes regarding open enrollment, special enrollment periods, and annual eligibility redeterminations. Rates also reflect benefit designs and cost-sharing structures aligned with the revised de minimis actuarial value (AV) ranges specified in the proposed rule for the 2026 plan year.” – Celtic Insurance Company (Illinois)

The Republican budget reconciliation package

The Republican budget reconciliation legislation, formerly known as the “One Big Beautiful Bill,” was signed by President Trump in early July. Though the law itself was rarely mentioned by name in the insurer rate filings, some insurers made specific references to provisions in the legislation — namely, the potential funding for cost-sharing reductions. While funding for cost-sharing reductions was ultimately not included in the law, uncertainty led some insurers to calculate rate increases for both scenarios.

“The estimated average change in rates that would be required if funding is provided for CSR payments is a decrease of 11.4% from the 2026 submitted rates. This adjustment would have no significant variation across plans and areas. The assumption change that leads to the decrease in rates is the use of standard silver variant AVs for CSR membership to project the post-CSR payment plan paid liability, opposed to using the full CSR variant AVs for this membership in the absence of CSR payments. Additionally, the statewide average premium was assumed to decrease by 9% percent which leads to a deterioration in our risk transfer estimate.” – Coordinated Care Corporation (Indiana)

In Michigan, in particular, insurers were instructed to submit additional rate filing documentation accounting for the impact of funding for cost-sharing reductions.

“As CMS has noted, there remains significant uncertainty regarding potential Congressional action or inaction, and multiple legislative outcomes could materially impact premium rates for Plan Year 2026. To address this uncertainty, UHC, as directed by DIFS, is submitting a set of rates and associated assumptions that reflect a scenario in which CSR payments are federally funded and enhanced premium tax credits under ARP and IRA expire.” – United Healthcare Community Plan (Michigan)

A handful of filings also mentioned other policy changes (changes to the Federal Medical Assistance Percentage (FMAP) and end of Medicaid expansion) that could be related to reconciliation. While the majority of insurers did not mention the Republican budget package in their rate filings this year, as provisions from the law begin to be implemented in the coming years, there is a potential for it to drive premiums upward.

Other potential drivers of premium changes

There are other factors not previously mentioned in this analysis that may play a role in premium changes. However, the following factors had little to no impact on premiums for 2026.

COVID-19

More than two years after the end of the federal public health emergency, most insurers no longer factor COVID-19 into their rate filings. When COVID-19 is mentioned, insurers generally say there is no impact on their 2026 premiums.

No Surprises Act

Implemented in 2022, the No Surprises Act protects patients from unexpected bills for select out-of-network services by allowing them to pay in-network cost-sharing rates. Of the reviewed insurer rate filings, none mentioned the No Surprises Act.

Price transparency

Both the Biden and Trump Administrations have taken steps to enhance healthcare price transparency, which could affect provider and insurer negotiations. However, insurers did not meaningfully mention any impact of these transparency measures on their 2026 premiums.

Methods

Proposed rates were collected from ratereview.healthcare.gov, California Department of Managed Health Care, and insurer rate filings for 312 insurers across 50 states and Washington, DC. Additionally, 105 insurer actuarial memoranda were collected from state rate review websites (or in the case of Georgia, provided directly by the state regulator) and were reviewed to understand the factors contributing to rate changes. These 105 insurers were from the following Marketplaces: Connecticut, the District of Columbia, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Maine, Maryland, Massachusetts, Michigan, Minnesota, New York, North Carolina, Oregon, Rhode Island, Texas, Vermont, and Washington. Insurer actuarial memoranda were systematically evaluated for key words related to, but not limited to, medical trend, COVID-19, Medicaid redeterminations, Inflation Reduction Act enhanced tax credits, tariffs, the ACA Marketplace Integrity and Affordability Rule, federal CSR funding, surprise billing, specialty medicine, telehealth, price transparency, market consolidation, and diabetes or weight loss drugs. Recorded medical trend values are annualized and do not include leveraging.

Appendix

The Peterson Center on Healthcare and KFF are partnering to monitor how well the U.S. healthcare system is performing in terms of quality and cost.