The high cost of healthcare can be a challenge for employers looking to provide affordable health benefit programs for workers and their families. Employers can offer markedly different health benefit experiences for workers, affecting access to care, the affordability of coverage, and the scope of benefits provided. As the cost of health insurance increases, employers continue to grapple with what types of benefits their employees want, how much to spend, and how to share costs with employees.

This brief discusses some of these differences, focusing on the costs, availability, and take-up of health benefits for workers with lower wages, and ways employers may respond to the pressures of high costs and limited resources for these workers. The analysis blends results from surveys from the Bureau of Labor Statistics and KFF Employer Health Benefits Survey, with insights from interviews and group discussions held with employers throughout the summer and fall of 2025 across the United States covering over 100 companies employing over a quarter of a million people.

Some key takeaways include:

- Health insurance compensation makes up an average of 8% of total compensation for all employees, but the dollar amounts vary by type of occupation.

- On average, around 3 in 4 employees are offered health insurance, and about 65% of those offered enroll in the benefit, but again, this varies by occupation.

- Service workers, which constitute a large proportion of lower-waged workers, are offered less in health insurance compensation and are less likely to be offered the benefit (52%). When offered, they are less likely than average to enroll.

- For employers who offer health insurance coverage options, they may offer low-premium plan options, tiered health insurance payments for lower-waged workers, or in-network options with no or low copays for care to support lower-waged workers.

- Large firms (over 5,000 employees) are most likely to offer health insurance premium supports for their lower-waged workers (29%), such as offering lower premiums to factory workers compared to “professional” workers.

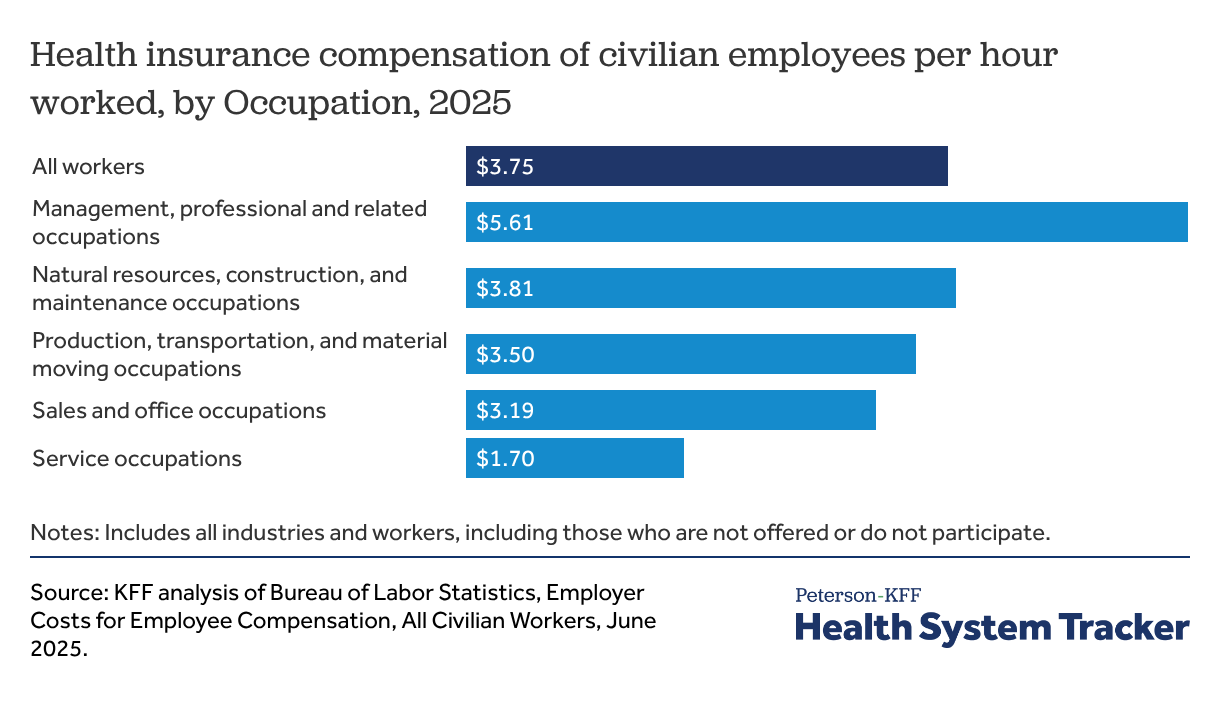

Health insurance compensation costs differ by type of occupation, with service workers receiving far smaller benefits than other occupations

Employer contributions to health insurance make up a significant part of employee compensation, averaging $3.75 per hour worked, or 7.8% of total compensation (across employers that do and do not offer health benefits). These amounts vary considerably across the workforce, with differences across industries and occupations, as well as firm size, wage levels, and other characteristics of the employer. For example, employer contributions for health insurance average $5.61 per hour for workers in management, professional, and related occupations, but only $1.70 per hour for those in service occupations.

Access to and take-up of health benefits

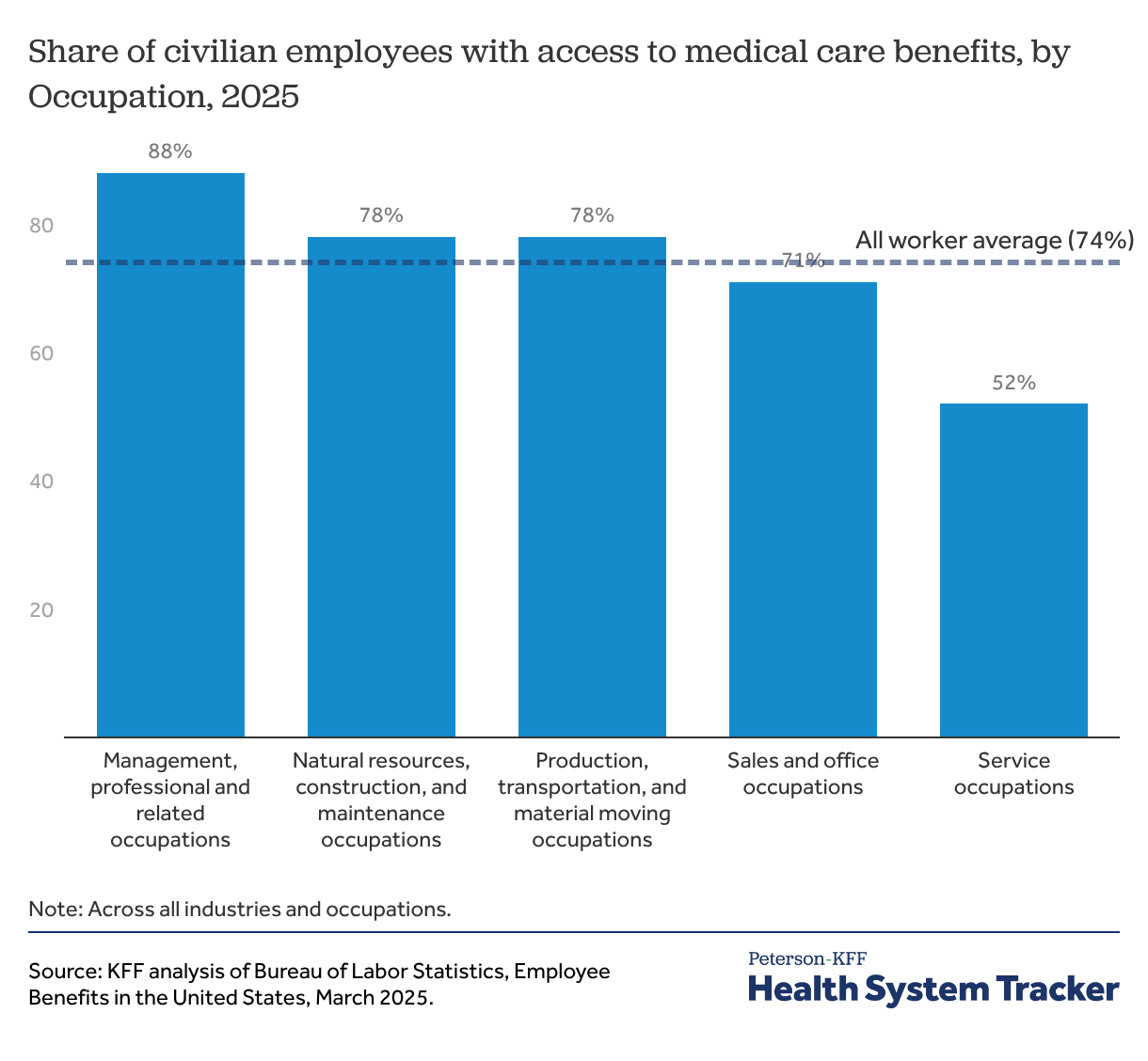

Health benefits are available to about 3 in 4 workers, but access varies significantly by occupation

Many firms of all sizes do not offer health benefits to part-time workers, and many smaller firms do not offer health benefits to any employees. Even in larger firms, newer employees may be ineligible for health benefits during probationary periods, which can last up to 90 days. On average, 74% of civilian workers had access to health benefits at their jobs in March 2025; this ranged from 88% of workers in management, professional, and related occupations to only 52% in service occupations.

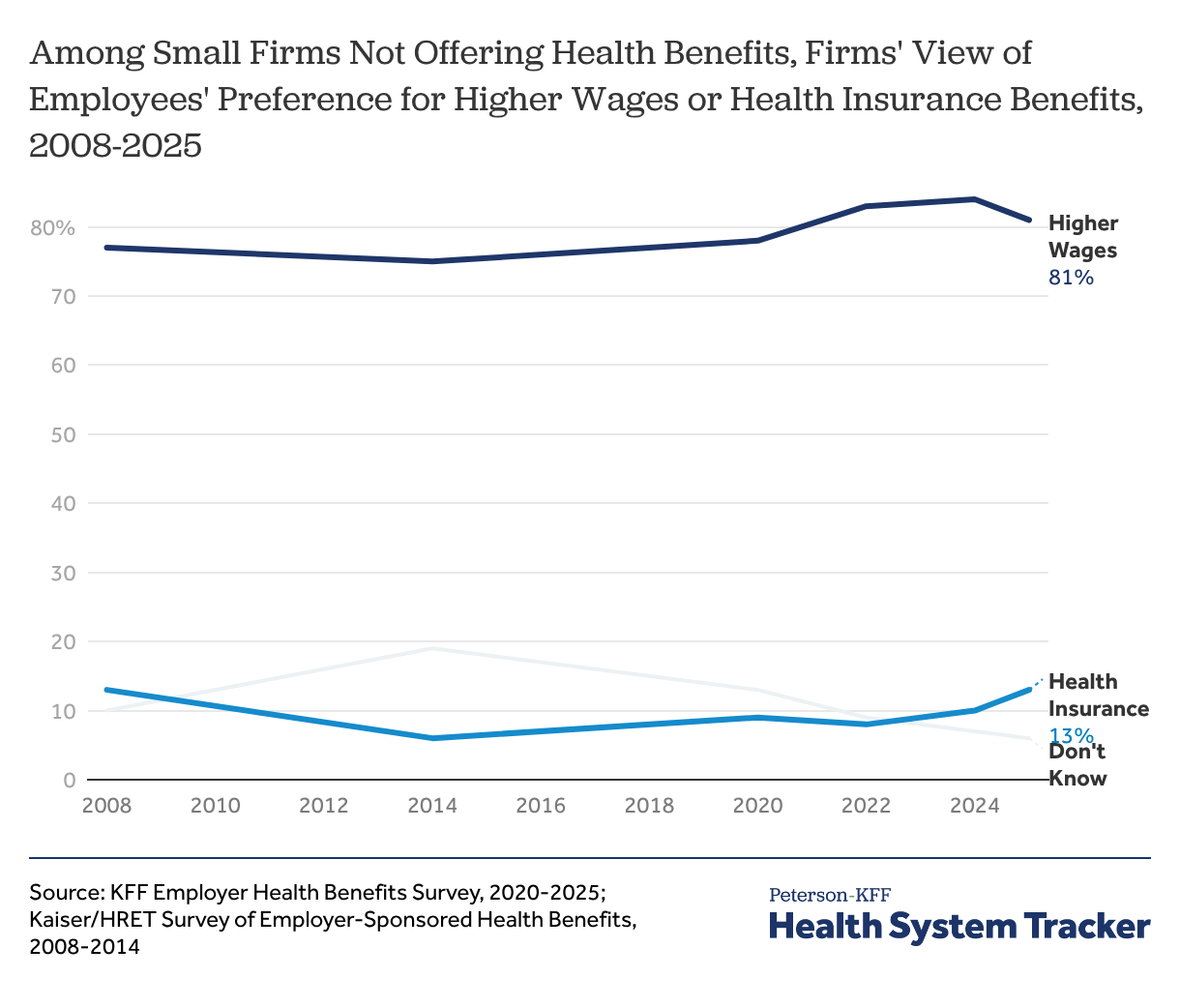

Small employers not offering health benefits believe that employees would rather have more money than health benefits

Health benefits are part of total compensation for employees, which means that there can be a trade-off for employers between providing health benefits and providing higher wages. Workers in lower-paying jobs may prefer, or need, to receive as much of their compensation as possible in wages in order to meet their day-to-day needs. Among smaller firms (200 or fewer workers) that do not offer health benefits in 2025, when asked about the tradeoff between health benefits and wages, 81% said that their employees would prefer an additional $2 per hour in wages rather than health insurance at their job. To the extent that there is a tradeoff between employer contributions for health insurance benefits and wages, rising premiums and employer premium contributions may also suppress wage growth.

Employers’ decision to offer benefits may also be affected by financial penalties for failing to offer coverage. Under the Affordable Care Act (ACA), employers with more than 50 full-time employees can face penalties for not offering health insurance meeting affordability and minimum value standards to their full-time employees.

“People just don’t sign up because they can’t afford even their part of the premium, so we get creative. We’ve partnered with One-to-One Health and have their text[-based health] care, which is a really great telehealth program that’s for all of our full-time staff and their spouse and children. It’s cheaper for us to pay the penalty than provide [comprehensive] health insurance that our staff could afford.” -HR Manager, large non-profit

“The [comprehensive] plans are just getting significantly worse in order for the employer and the employee to be able to possibly afford it.” -VP Employee Benefits, health insurance broker

Related Content:

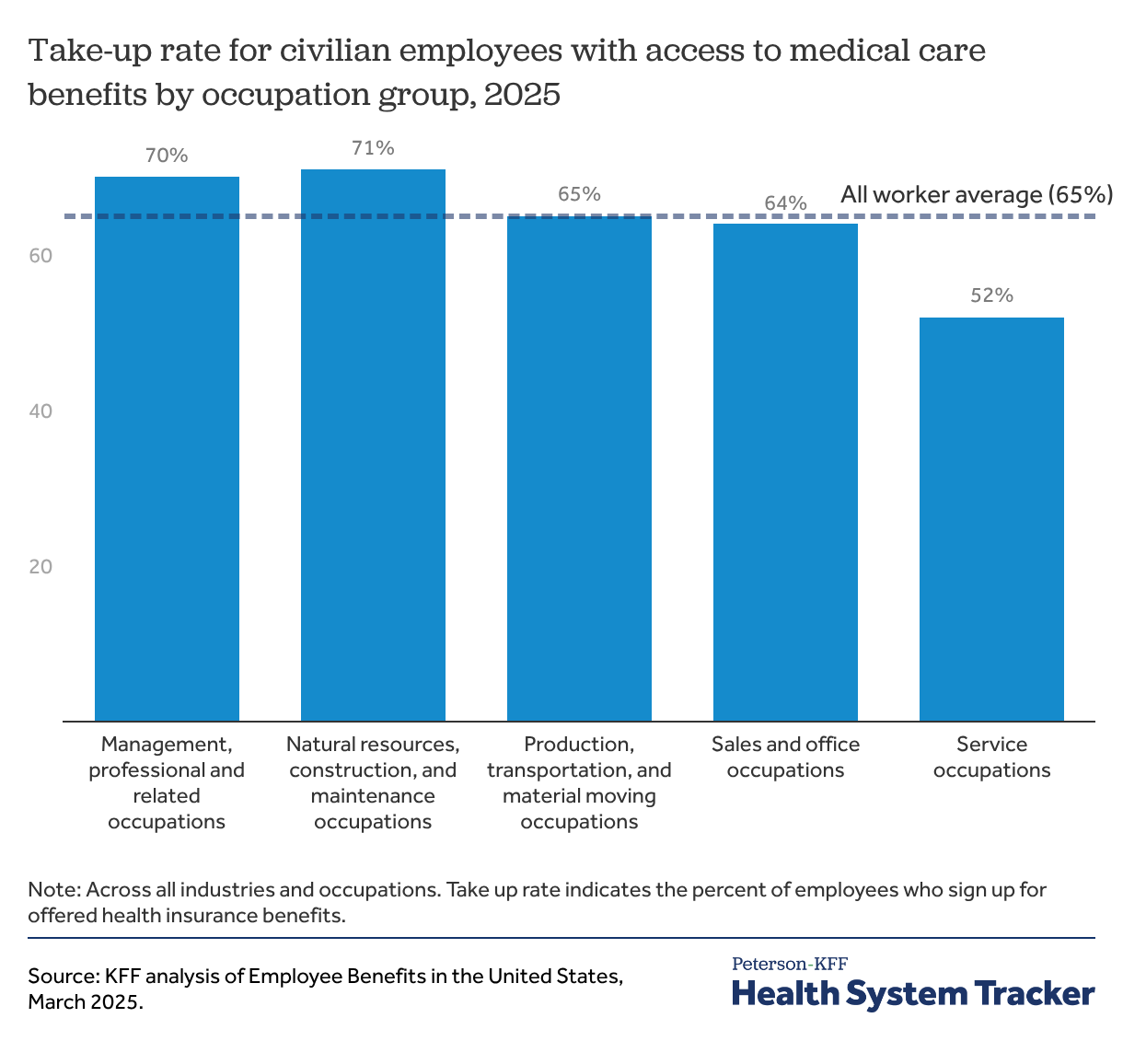

A majority of employees (65%) sign up for the health insurance that they are offered at work

Even when workers are offered health benefits at their job, some do not take up coverage. On average, 65% of workers with access to health benefits at their jobs took up the coverage they were offered in March 2025; this ranged from 71% of workers in natural resources, construction, and maintenance occupations to 52% of workers in service occupations. Some workers may already have coverage, such as job-based coverage through a spouse or parent, or coverage through Medicare or Medicaid. Others may not think that they can afford the coverage that they are offered.

“We have some hourly employees in particular [who] just choose not to be insured. One thing we are currently dealing with is to consider a sort of free health care plan with a higher deductible that basically just says you have something in case of more or less a catastrophic health condition. So it’s basically a minimum essential coverage plan just to be able to say at least we have … the peace of mind that they have the coverage in case of something very significant [like an accident or illness].” -HR Professional, large services organization

“You have a lot of people who are choosing just not to have coverage because they don’t want to pay the premiums. They can’t afford it. They can’t afford the premiums.” -HR Director, insurance consultant

“Prior to [creating a tiered health insurance plan], if you would have polled our team, I would guess that less than half, especially the lower-income market, would have had [health insurance coverage].” -Vice President of HR, large manufacturer

Related Content:

Related Content:

Workers in lower-wage occupations have particularly low access and take-up rates

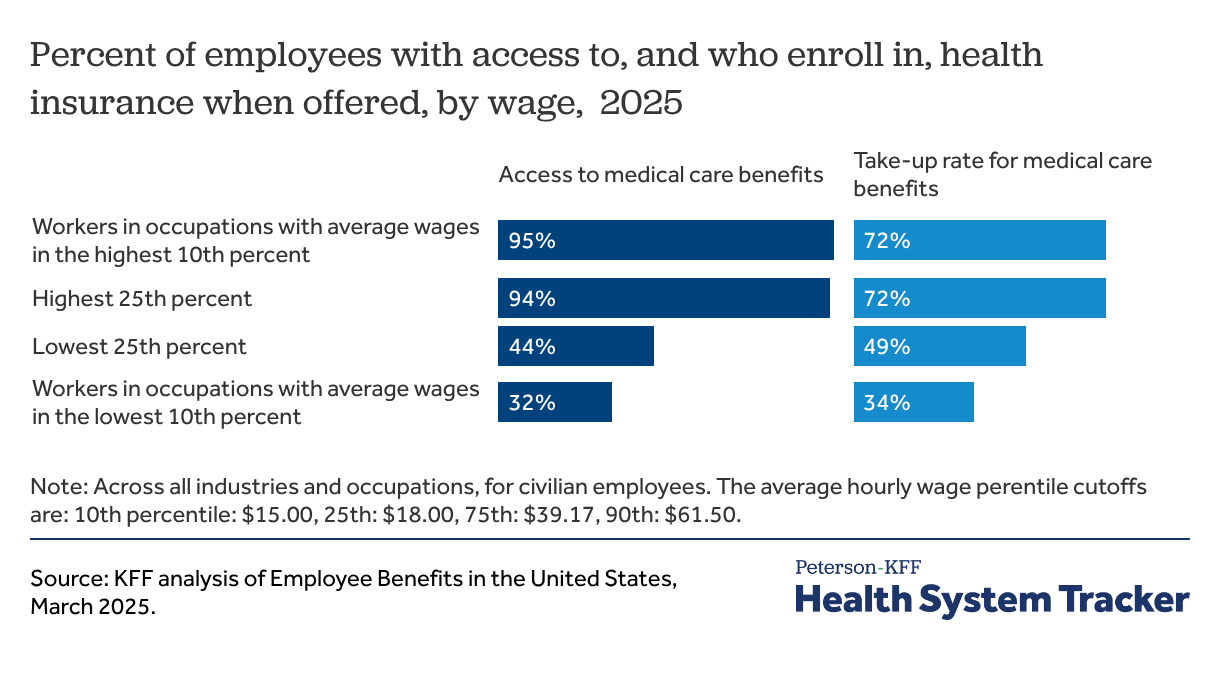

Workers in occupations with relatively low average wages are much less likely to have access to health benefits at their jobs and, even when they do, they are much less likely to enroll. While over 90% of those working in the occupations in the top quartile of average hourly wages (corresponding to more than $48.27 per hour) had access to health benefits at work in March 2025, fewer than half (44%) of workers in the lowest quartile of average hourly wages (corresponding to less than $22.63 per hour) did so.

Workers in these lower-wage occupations also are less likely to take up health benefits when they are offered. Among workers with access to health benefits at their job, only 49% of those in occupations in the lowest quartile of average wages chose to enroll in the offered coverage, compared to at least 70% of workers in the top two quartiles. Those in service occupations were less likely to enroll in their offered medical care benefits compared to other occupations.

Assessing health insurance affordability for lower-waged workers

Participation in job-based coverage is tied to how affordable the coverage is. There are several aspects to consider when assessing affordability: can the worker afford the contribution for self-only coverage; can they afford the additional contribution to cover family members (when it is offered), and can they afford the out-of-pocket costs if they or their family members use their coverage. This latter factor includes both the cost-sharing for covered benefits (e.g., deductibles and out-of-pocket limits) as well as the comprehensiveness of the coverage (e.g., does the plan meet the standard for “minimum value” and cover the essential health benefits?).

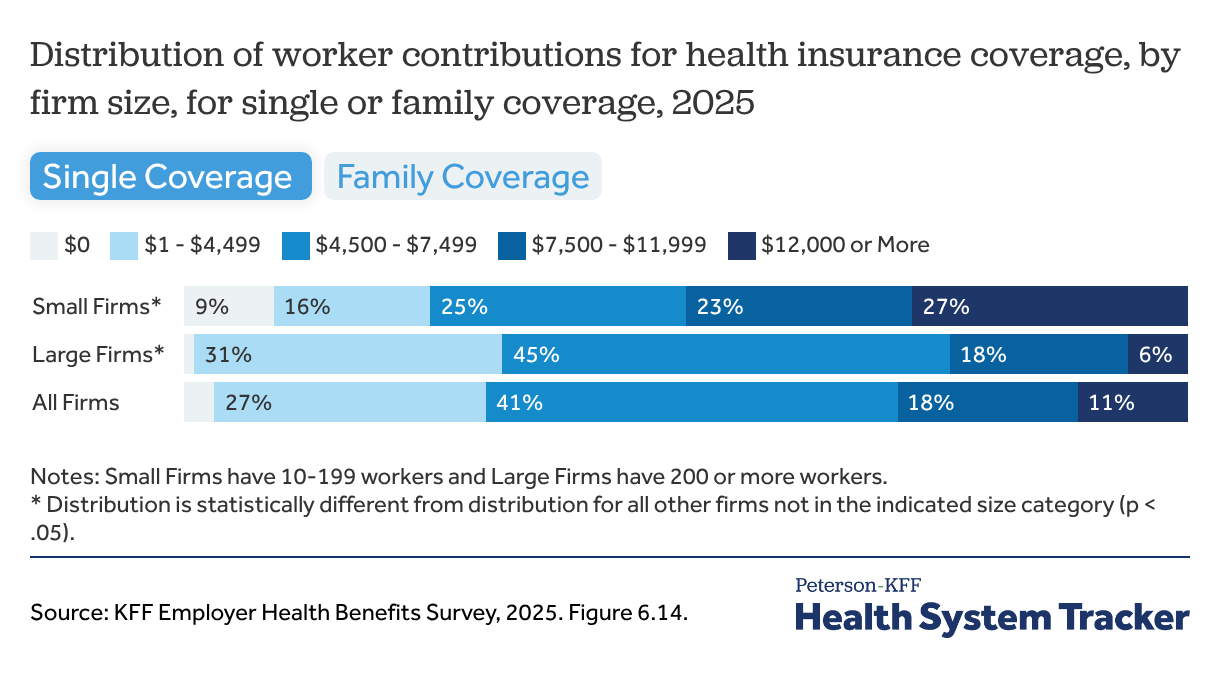

Small firms are both more likely to offer $0 premium plans to their employees and the most expensive plans for single coverage, compared to larger firms

The average annual contribution in 2025 for self-only coverage was $1,440, with considerable variation around the average: 12% of covered workers were able to enroll in self-only coverage with no required contribution while another 12% had an annual contribution of $2,500 or more. This average amount, while a relatively modest expense for many workers, is 9.5% of the earnings for a full-time minimum-wage worker in many states.

The contribution amounts for family coverage can be considerably higher: The average annual contribution amount for covered workers for family coverage in 2025 was $6,850, but 27% of covered workers (including about a third of covered workers in firms with fewer than 200 workers) were in a plan with an annual family contribution amount of $12,000 or more.

Employers hear from their employees that the high price of premiums is a barrier to enrollment, particularly for hourly, lower-waged workers.

“We do an annual benefit survey, like what do you care most about? And it’s premium, premium, premium.” -Director of Total Rewards, large retail firm

“We have about 30 out of 240 people that are a lower wage hourly and we’re trying to explore how to offer something with lower premiums without, you know, being non-compliant.” -VP Human Resources, large manufacturer

Related Content:

“The affordability [of health insurance] continues to go down… There’s always like a significant difference between the salaried employees and the hourly employees. And that’s the hardest part…You have to offer a couple plans because there’s one for the salaried people that are making significantly more, but then you try to get the hourly employees on [insurance] and they may still wave [the benefit] even though you’ve factored in the affordability factor. They’re living paycheck to paycheck. So even if it’s only $120 per paycheck that takes groceries off the table… From the employer standpoint, what’s the next best thing? Now we go from a $5,000 deductible to an $8,000 [deductible].” -VP Employee Benefits, health insurance broker

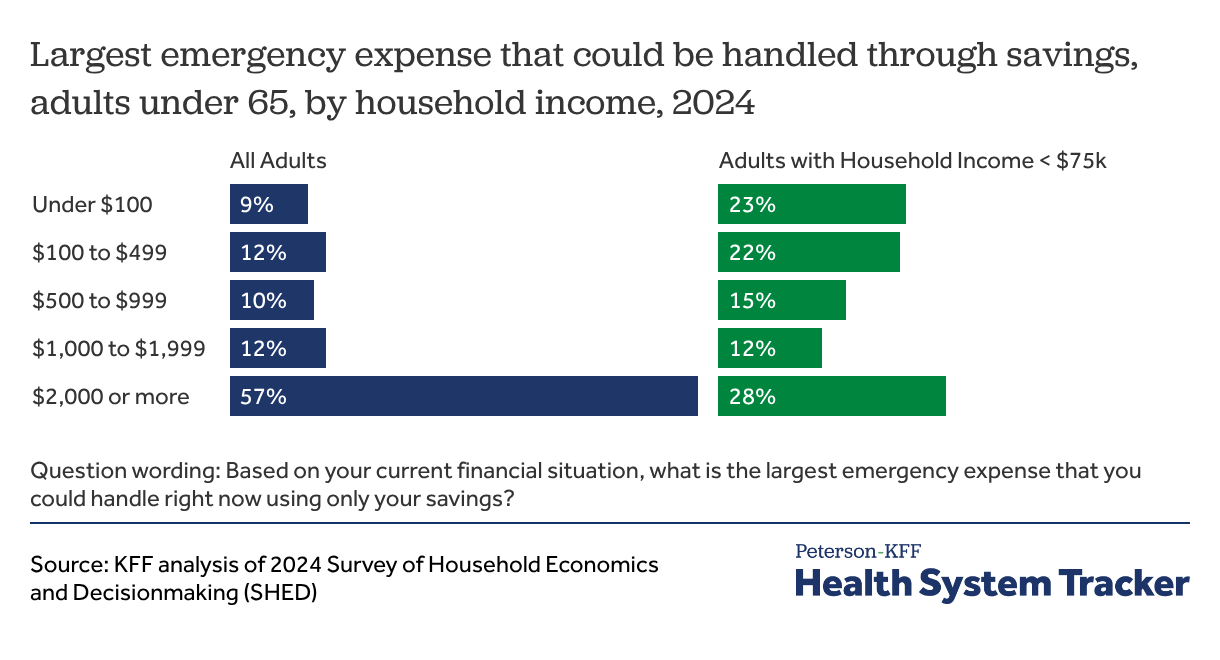

One-third of all adults under 65 and two-thirds of adults with household incomes under $75,000 report having less than $2,000 available for an emergency

In addition to required premium contributions, workers with job-based coverage can face thousands of dollars in cost-sharing if they need a significant amount of care. The average general annual deductible amount for workers with self-only coverage and a deductible was $1,886 in 2025, and 34% of covered workers were in a plan with a deductible of $2,000 or more, including 19% in a plan with a deductible of at least $3,000. Many covered workers also face significant additional cost-sharing for hospital stays or outpatient procedures. For example, 65% of covered workers faced coinsurance if they were hospitalized in 2025, with an average coinsurance rate of 20% of the hospital costs in addition to any general annual deductible.

Even a few thousand dollars of out-of-pocket costs can place significant strains on household finances. In an October 2024 survey conducted for the Board of Governors of the Federal Reserve System, only 3 in 5 adults under age 65 with job-based coverage reported that they could handle an emergency expense of $2,000 or more using only their savings. This percentage falls to only 27% for these adults in households with incomes under $75,000 (about half the overall U.S. population).

Employer strategies to improve affordability for lower-wage workers

There are several strategies that employers use to improve affordability for lower-wage workers, including offering lower-priced, less generous plan options for workers and reducing contribution amounts or cost-sharing for workers based on their wage levels. The first approach helps workers enroll in coverage but may expose them to high out-of-pocket costs if they need significant levels of healthcare. Subsidizing contributions for lower-wage employees may help them afford more comprehensive plan options that otherwise might be difficult for them to afford.

In the focus group discussions, many employers reported offering different plan levels to try and accommodate different portions of their workforce.

“For 2026, we are adding a value plan. We have your standard PPO traditional plan, you have our HRA, which is our richest plan, and then the business came to us and said we really need to try to get more into our associates’ take-home pay. I came up with this value plan. The concern that we have is we don’t want people just choosing the value plan if that is not the best plan for them, so we did our best with the education as far as our open enrollment guide, which is in print right now and we’ll be doing employee meetings.” -Director of Total Rewards, large manufacturer

Related Content:

“When it comes to affordability it, to some degree, will depend on what the service is. We offer two different plans: a higher-cost plan and a lower-cost plan to meet the needs of our population.” -Director of Safety, Health, and Wellness, large manufacturer

“We don’t offer specific plans for [low-wage workers such as store associates], but we have really made an effort to try to offer low-premium options. But a lot of them have told us they like our PPO plan, which is the plan with the higher premiums and then the copays, because it is predictable. They know when they need to go [to the doctor] they aren’t going to worry about [the costs of] that care.” -Benefits Manager, large retailer

“We have two different types of insurance plans. We have the base plan, which is the more expensive plan where you may have a set copay, but you’re paying more for that monthly premium. Or you have the high-deductible health plan. And whether it be someone that is making less money working on the line or even our executives, I would say the majority of our company is switching over to the high-deductible plan because the way they have it set is they get so much money in the card [as an employer contribution] every six months. I don’t know how much it is, around $500 individual, $750 family every six months. And then the actual out-of-pocket deductible is not that much different between a high-deductible insurance carrier and a basic plan.” -Occupational Health Manager, large manufacturer

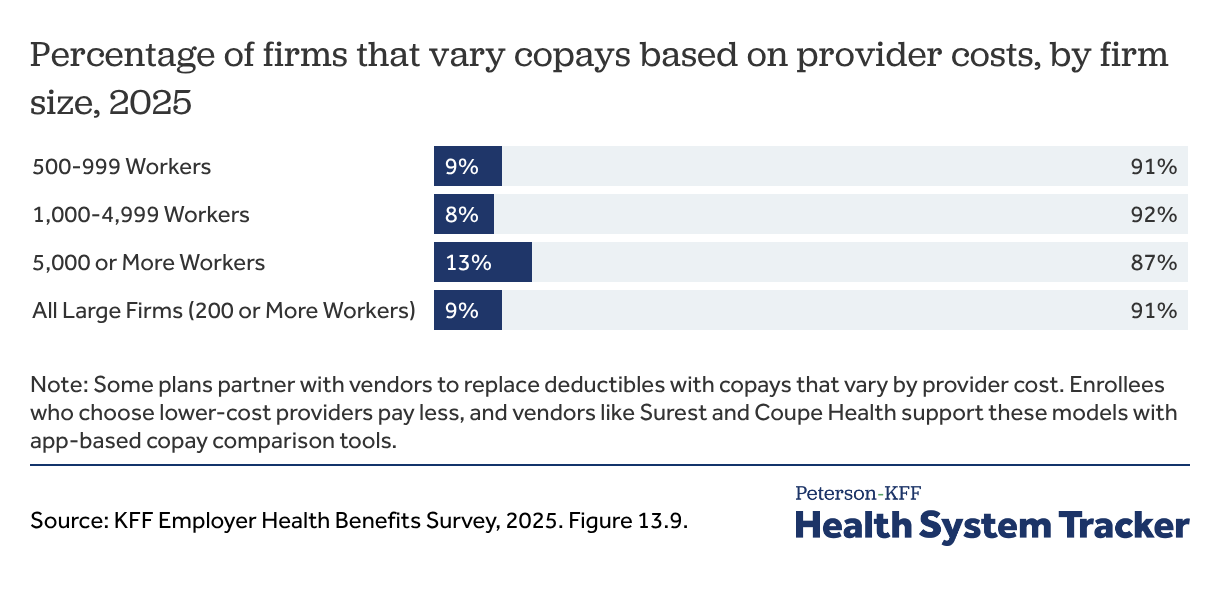

Around 1 in 10 firms offer variable copay plans, incentivizing employees to visit low- or no-copay providers

Some focus group employers expressed concern that reducing premium contributions by increasing cost-sharing could make it difficult for employees to afford needed care. As a response, several employers described offering a copayment plan, either as an alternative or as a substitute for a higher deductible plan offering. While there are different variations, these arrangements generally eliminate deductibles and set copayment amounts based on the provider chosen by the enrollee. Enrollees that choose lower-cost or higher-quality providers might face a lower copayment while those choosing higher-cost providers would pay more. Nationally, 9% of employers reported partnering with a vendor to offer a varying copayment arrangement.

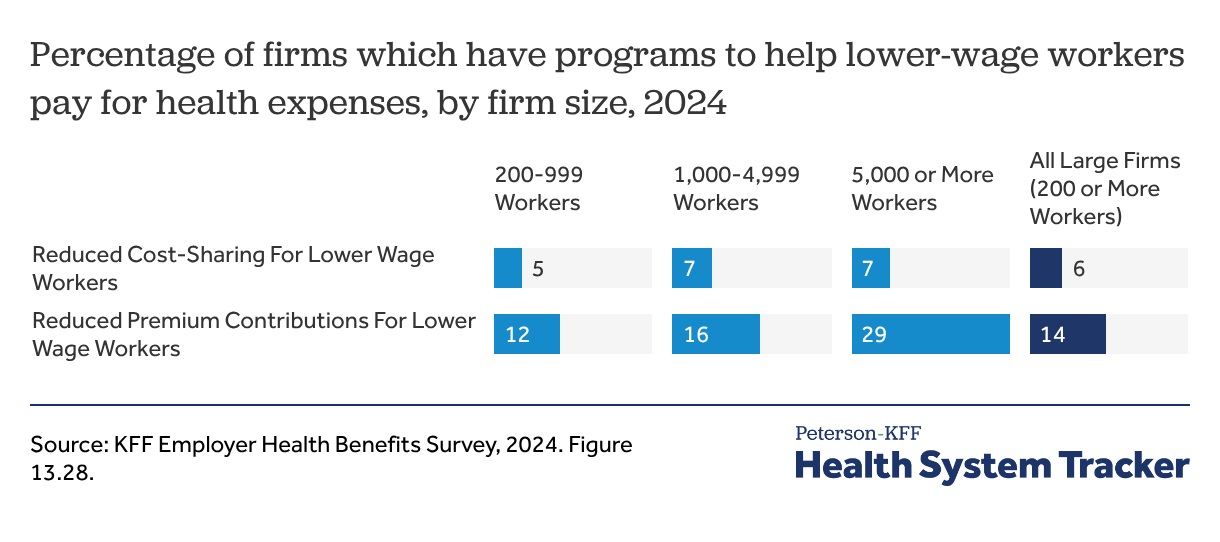

Firms with over 5,000 workers are twice as likely to offer reduced premium contributions for lower-wage workers, and few firms of any size offer reduced cost-sharing

Another approach that some employers take to improve affordability for lower-wage workers is to reduce what they need to pay for contributions or cost-sharing. Among employers with 200 or more workers offering health benefits in 2024, 14% offered a health plan with reduced premium contributions and 6% offered plans with reduced cost-sharing for lower-waged workers. Employers with 5,000 or more workers were more likely to offer these benefits.

Several focus group participants discussed how their salary-based tiered plans worked.

“We actually contributed more of a percentage to the premium. So anybody who makes $25[per hour] or less has a lower premium cost, and then anybody $26 [per hour] and greater they have a higher premium cost-share.” -Human Resources Director, small services organization

“We have a tiered approach with our premiums that goes back four or five years. Lower-paid factory workers, their premiums will be lower than, say, someone on a professional side.” -Director of Total Rewards, large manufacturer

“We have salary-based premiums that are cut in four tiers. About half of our folks make under $65,000 a year, so there is a tier below $50,000 and then there’s a tier for $50,000 to $65,000 and you get a reduction for either plan you choose. There’s copay and cost-sharing reductions for going to see certain types of providers across the board. But then we’ve specifically targeted lower-wage employees, reducing the cost to cover kids explicitly. So if you cover the employee and spouse premium, it’s the same as the family premium. You’re trying to fundamentally make it cheaper to bring kids on your plan.” -Executive Administrator of the State Health Plan

Related Content:

Employers described facing challenges with these banded contributions.

“We have salary-banded contributions, so their [the lowest-waged workers’] contributions are actually in our lowest tier, but they are making less than our entry-level consultants. Their non-medical benefits, like their dental and vision, are voluntary. We tried to keep the healthcare plan as generous … but because we don’t have a large enough population… it’s not worth setting up all the one-off contracts.” – Senior Director of Benefits, large consulting agency

Employers’ decisions to offer coverage, and workers’ decisions to enroll in that coverage, are influenced in part by the availability of other sources of insurance, including public programs such as Medicaid and the ACA Marketplaces. Workers with incomes below 138% of the federal poverty level may qualify for Medicaid in states that have expanded eligibility if they meet applicable requirements. Those eligible for Medicaid may enroll in Medicaid alone, enroll in both Medicaid and employer-sponsored coverage, or choose between the two; in some cases, Medicaid serves as a secondary payer and reduces out-of-pocket costs for the employer plan. Among firms with 10 to 199 workers that do not offer health benefits, 34% say Medicaid is “very important” in providing coverage for their employees, compared with 29% of firms that do offer coverage.

Workers whose incomes are too high for Medicaid may seek coverage in the ACA Marketplaces, but they are generally ineligible for premium subsidies if they have an affordable offer of employer coverage. As a result, some lower-wage workers could face lower premium costs in the nongroup market if they did not have an employer offer. Among small firms that do not offer health benefits, 7% report that they do not offer coverage because their employees can obtain a better deal in the Marketplaces. In addition to offering programs targeted at lower-wage workers, some employers may attempt to facilitate employees qualifying for public programs in which they are eligible.

Methods

Survey data come from the U.S. Bureau of Labor Statistics, National Compensation Survey (NCS), Employee Benefits in the United States, March 2025. This dataset includes the civilian workforce only, and all industries. Additional tables come from the U.S. Bureau of Labor Statistics, Employer Costs for Employee Compensation, Historical Datasets from 2004-Present (June 2025), released on September 12, 2025. Civilian workforce includes private industry, state, and local government, but does not include federal workers, self-employed, or agricultural workers. Some data is also from the October, 2024 Survey of Household Economics and Decisionmaking (SHED) conducted for the Board of Governors of the Federal Reserve System. SHED data include adults under 65 with job-based coverage and adults who also report having coverage through Medicare or Medicaid. Finally, some data come from the 2024 and 2025 KFF Employer Health Benefits Surveys.

In the summer of 2025, KFF staff held five focus groups across the United States, speaking with human resources and benefits specialists to identify ways they were addressing health insurance for lower-wage workers. Four focus groups were held in person, conducted at The Alliance 2025 Spring Symposium in Madison, Wisconsin; 2025 TN SHRM Conference in Nashville, Tennessee; NC Business Group on Health’s Fall Forum 2025 in Greensboro, North Carolina, and the Austin SHRM Annual Conference in Austin, Texas. One focus group occurred virtually with the Midwest Business Group on Health.

The authors would like to thank SHRM, and particularly SHRM Tennessee and SHRM Austin, as well as the Midwest Business Group on Health, the NC Business Coalition on Health, and The Alliance for their assistance in organizing the focus groups.

The Peterson Center on Healthcare and KFF are partnering to monitor how well the U.S. healthcare system is performing in terms of quality and cost.