The term “surprise medical bill” describes charges arising when an insured person inadvertently receives care from an out-of-network provider. Surprise medical bills can arise in an emergency when the patient has no ability to select the emergency room, treating physicians, or ambulance providers. Surprise bills can also arise when a patient receives planned care. For example, a patient could go to an in-network facility (e.g., a hospital or ambulatory surgery center), but later find out that a provider treating her (e.g., an anesthesiologist or radiologist) does not participate in her health plan’s network. In either situation, the patient is not in a position to choose the provider or to determine that provider’s insurance network status.

In this analysis, we use claims data from large employer plans to estimate the incidence of out-of-network charges associated with hospital stays and emergency visits that could result in a surprise bill. We find that millions of emergency visits and hospital stays put people with large employer coverage at risk of receiving a surprise bill. For people in large employer plans, 18% of all emergency visits and 16% of in-network hospital stays had at least one out-of-network charge associated with the care in 2017. We also examine state and federal policies aimed at addressing the incidence of surprise billing. Our analysis finds a high degree of variation by state in the incidence of potential surprise billing for people with large employer coverage, who are generally not protected by state surprise billing laws if their plan is self-insured. For people with large employer coverage, emergency visits and in-network inpatient stays are both more likely to result in at least one out-of-network charge in Texas, New York, Florida, New Jersey, and Kansas, and less likely in Minnesota, South Dakota, Nebraska, Maine, and Mississippi.

Background

Surprise medical bills generally have two components. The first component is the higher amount the patient owes under her health plan, reflecting the difference in cost-sharing levels between in-network and out-of-network services. For example, a preferred provider health plan (PPO) might require a patient to pay 20% of allowed charges for in-network services and 40% of allowed charges for out-of-network services. In an HMO or other closed-network plan, the out-of-network service might not be covered at all.

The second component of surprise medical bills is an additional amount the physician or other provider may bill the patient directly, a practice known as “balance billing.” Typically, health plans negotiate discounted charges with network providers and require them to accept the negotiated fee as payment-in-full. Network providers are prohibited from billing plan enrollees the difference (or balance) between the allowed charge and the full charge. Out-of-network providers, however, have no such contractual obligation. As a result, patients can be liable for the balance bill in addition to any applicable out-of-network cost sharing.

Unexpected medical bills, including surprise medical bills, lead the list of expenses most Americans worry they would not be able to afford. Two-thirds of Americans say they are either “very worried” (38 percent) or “somewhat worried” (29 percent) about being able to afford their own or a family member’s unexpected medical bills.

Read more from

Surprise BIlls

See more briefs and data.

Large majority are worried about being able to afford surprise medical bills for them and their family

Four in ten (39%) insured nonelderly adults said they received an unexpected medical bill in the past 12 months, including one in ten who say that bill was from an out-of-network provider. Of those who received an unexpected bill, half say the amount they were expected to pay was less than $500 overall while 13 percent say the unexpected costs were $2,000 or more.

Eight in ten Americans (78%) support passage of federal legislation to protect patients from surprise medical bills. A majority (57%) continue to support such legislation even after hearing opponents’ arguments that it could lead to doctors and hospitals being paid less.

Incidence of surprise medical bills

To estimate the incidence of potential surprise medical bills, we analyzed large employer claims data from IBM’s MarketScan Research Database, which contains information provided by large employers about claims and encounters for almost 19 million individuals. By using a claims database, we can examine situations that are likely to result in a surprise out-of-network bill. For example, these data can be used to estimate how often an enrollee accesses services through an emergency room and receives services that are billed as out-of-network. The data can also show when an enrollee had an inpatient admission at an in-network hospital or other facility and yet receives covered services that are billed as out-of-network. The database does not provide complete information about surprise bills, however. In particular, the database contains only paid claims, not denied claims, and so, with respect to in-network inpatient stays, it may not reflect claims for services provided by out-of-network providers if the group plan (say, an HMO), denied those out-of-network claims. In addition, the MarketScan database reflects only the amount of allowed charges under a plan. As a result, the database cannot provide estimates of the dollar amounts of surprise bills – the difference between billed charges and allowed charges – involved in surprise medical bills. For more information, see the Methods.

Emergency services

In an emergency setting, patients are often unable to ensure they go to an in-network emergency room. The Affordable Care Act (ACA) provides partial protection for patients receiving out-of-network emergency care. The ACA requires all non-grandfathered health plans to cover out-of-network emergency services and to apply the in-network level of cost sharing to such services. Health plans are also required to pay a reasonable amount for the out-of-network emergency services.[i] However, the ACA does not prohibit balance billing by facilities or providers for emergency care. As a result, patients can and do receive surprise bills for emergency care from the emergency room facility and from providers who treat the patient in the ER. Surprise medical bills might also arise from the hospital and/or other treating providers if the emergency patient is subsequently admitted for inpatient care.[ii]

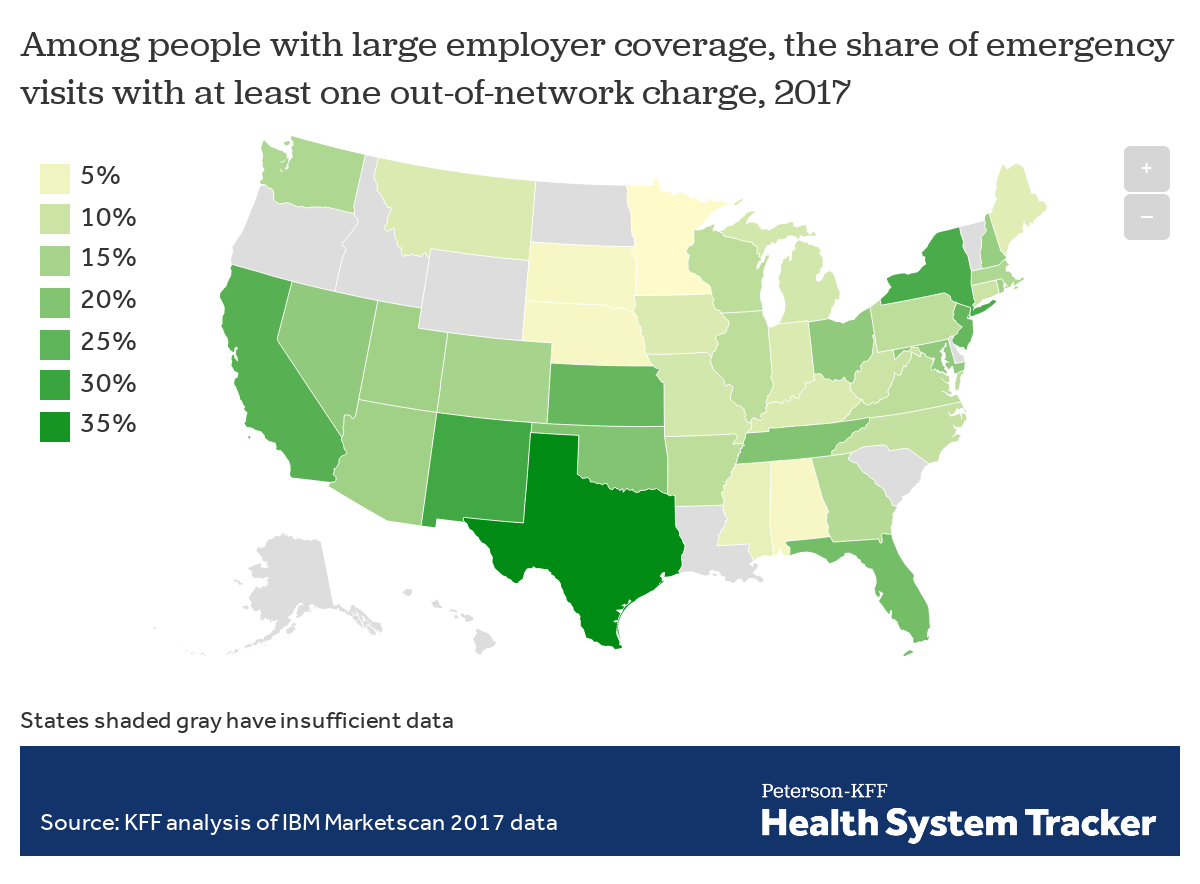

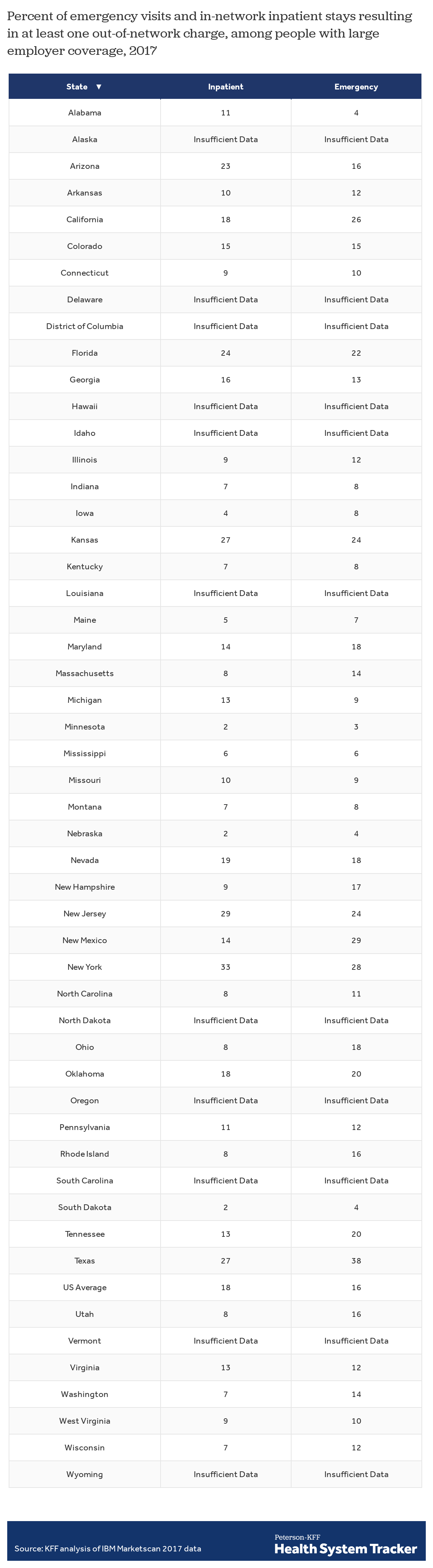

Of the emergency room visits in 2017 by people with large employer coverage, we estimate 18% had at least one out-of-network charge (from either the facility, the provider, or both) associated with the visit. This includes out-of-network charges from the emergency facility, emergency room providers, and provider and facility charges associated with a resulting inpatient stay, when applicable.

The rate of out-of-network billing in emergency settings for people with large employer coverage varies quite a bit from state to state. About a quarter or more of emergency visits in Texas (38%), New Mexico (29%), New York (28%), California (26%), Kansas (24%), and New Jersey (24%) resulted in at least one out-of-network charge in 2017, while the rate was under 5% in Minnesota (3%), South Dakota (4%), Nebraska (4%), and Alabama (4%). Emergency visits in urban areas (18%) are somewhat more likely to result in at least one out-of-network charge than are visits in rural areas (14%). The data used in this analysis are for large employers who typically self-insure and are therefore not subject to current state protections.

On average, 18% of emergency visits result in at least one out-of-network charge, but the rate varies by state

Most of the potential surprise out-of-network emergency charges observed in this study were from doctors and other out-of-network professionals, rather than from the hospital or emergency facility. Most people with large employer coverage use in-network emergency facilities. Nationally in 2017, 78% of emergency visits by people with large employer coverage were at an in-network facility.

Emergency visits that lead to an inpatient admission are more likely to result in an out-of-network charge (26%) than outpatient-only emergency visits (17%). This is in part due to out-of-network charges that occur after admission, but also due to a higher likelihood of out-of-network emergency professional charges in these cases.

Inpatient care

Surprise medical bills also arise from inpatient admissions, generally when patients are admitted to an in-network hospital or other facility for care. Even within an in-network facility, out-of-network charges for professional services can occur. That is because the doctors who work in hospitals often do not work for the hospitals; rather they bill patients separately and may not participate in the same health plan networks that cover the in-network facility.

The ACA protections for emergency services, described above, do not apply to non-emergency services, including non-emergency surprise medical bills, so in non-emergency admissions, the patient not only is at risk of being balanced billed by the provider, but also faces higher cost sharing under her insurance plan for the out-of-network claims. If the patient’s health plan is a Health Maintenance Organization (HMO) or an Exclusive Provider Organization (EPO) that does not provide any coverage for non-emergency care received out of network, the surprise medical bill claim may not be covered by the health plan at all.

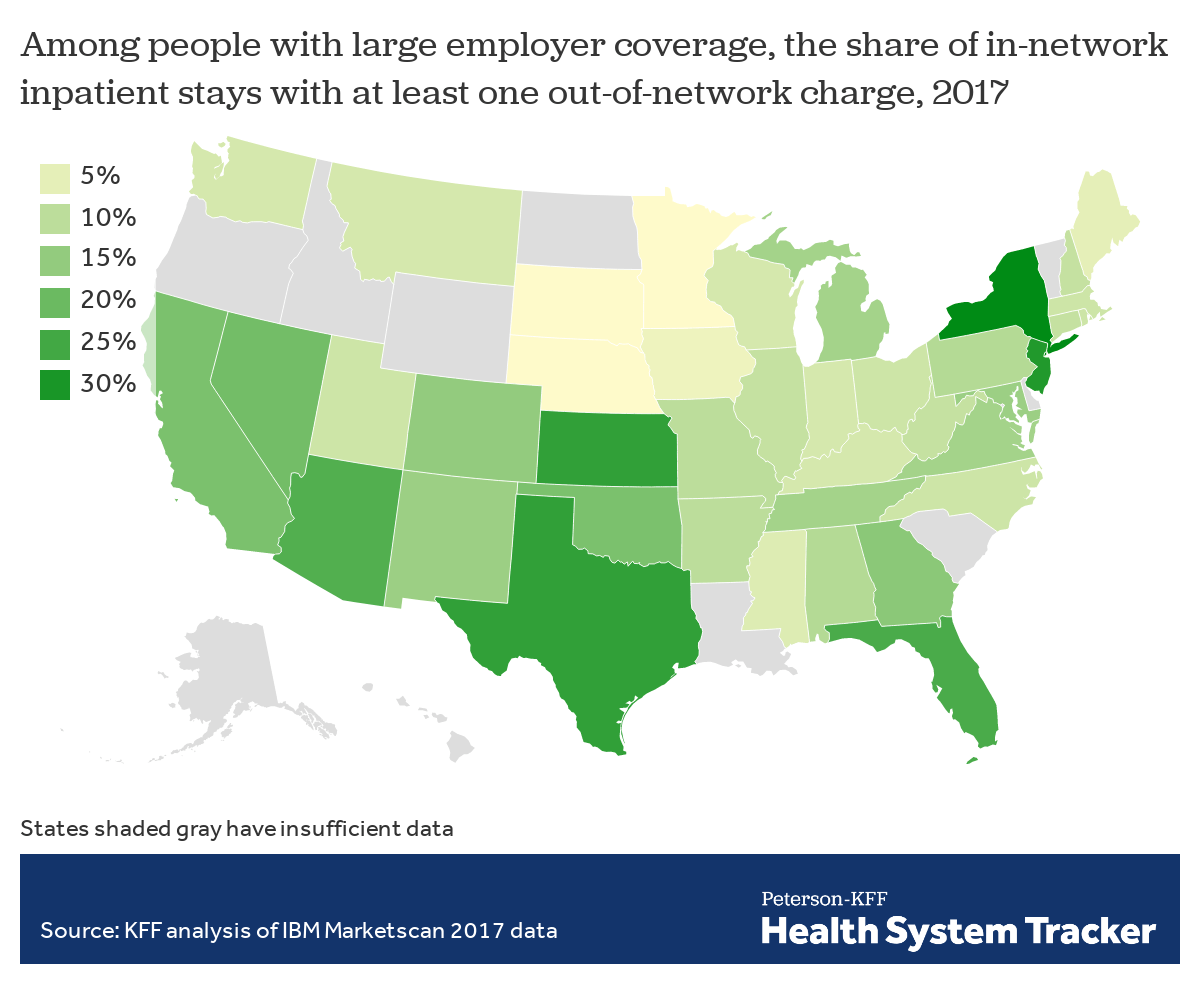

In 2017, among people with large employer coverage who had inpatient stays, the vast majority (90%) were at in-network facilities. Even when patients were admitted to in-network facilities, though, 16% of these stays resulted in at least one out-of-network charge for a professional service. As described above, in many of these cases, the patient not only is at risk of being balanced billed by the provider, but also likely faces higher out-of-pocket costs under her insurance plan for the out-of-network claims.

The rate of out-of-network charges for services at in-network inpatient facilities ranged from 2% of in-network inpatient stays in South Dakota, Nebraska, and Minnesota, to about a quarter or more in New York (33%), New Jersey (29%), Texas (27%), and Florida (24%). Inpatient stays in urban areas (16%) are somewhat more likely to result in at least one out-of-network charge than are stays in rural areas (11%).

On average, 16% of in-network inpatient admissions result in at least one out-of-network charge, but the rate varies by state

State action on surprise medical bills

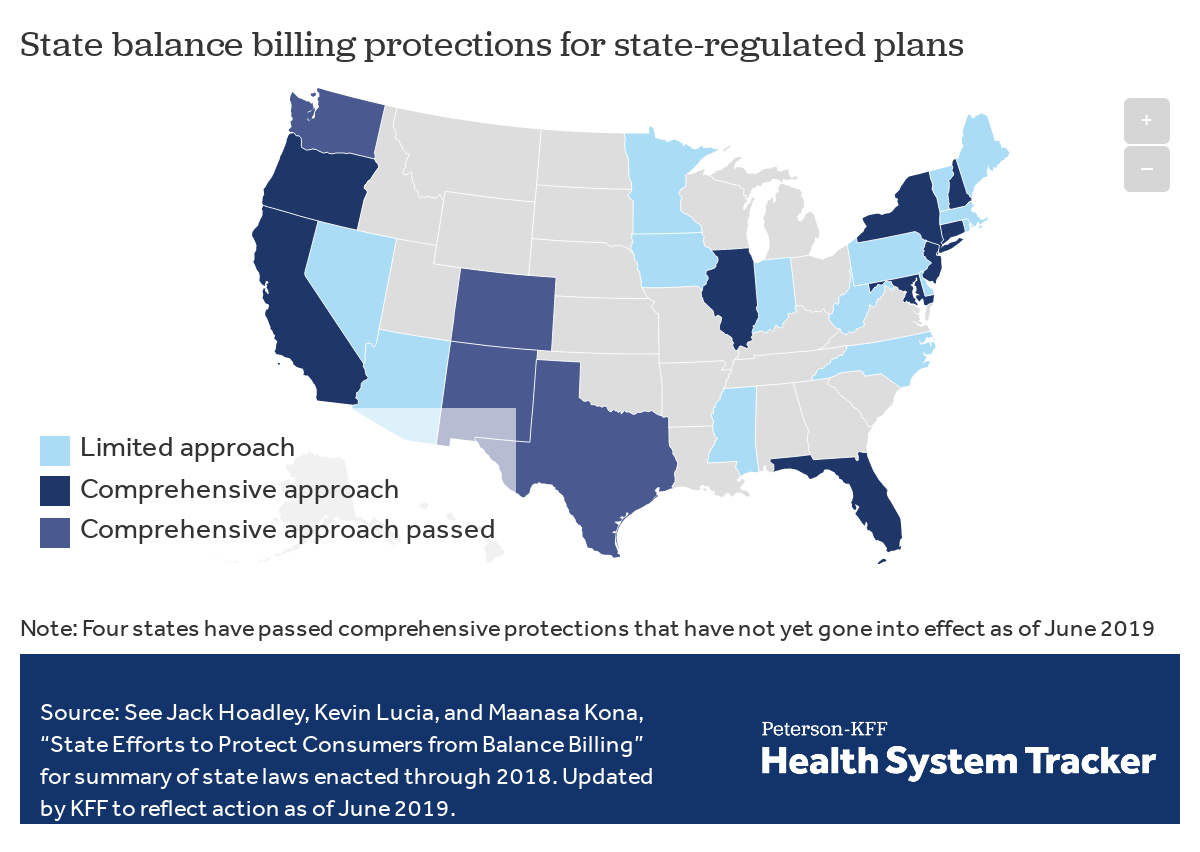

States have begun to enact laws to protect some patients from surprise medical bills, though, as discussed below, these state laws generally do not apply to people with large employer coverage whose employers self-insure. At least nine states have enacted and implemented laws taking a comprehensive approach to surprise bills (California, Connecticut, Florida, Illinois, Maryland, New Hampshire, New Jersey, New York, and Oregon). Four more states – New Mexico, Washington, Colorado, and Texas enacted new surprise medical bill laws in 2019 that have not yet taken effect.[iii]

States vary in their approach to surprise bills

The comprehensive state laws share common features:

Hold patients harmless

Comprehensive state laws hold consumers harmless against surprise medical bills. The hold-harmless protection generally involves two types of requirements – one for state-regulated health insurers, and one for providers. Insurers are required to cover out-of-network claims and apply in-network level of cost sharing for surprise medical bills. In addition, laws prohibit providers from balance billing patients covered by state-regulated plans; instead, the out-of-network provider is limited to collect no more than the applicable in-network cost-sharing amount from patients in cases of surprise medical bills.

State laws may also require notice to consumers about their rights and protections. New York, for example, requires state-regulated insurers to include prominent, standardized notice on the explanation-of-benefits (EOB) statement summarizing consumer rights regarding surprise medical bills. Notices also give consumers information about where they can file complaints or receive help. In California and New Mexico, out-of-network providers also are required to include prominent notice in billing invoices and other written communications pertaining to surprise medical bills that the consumer is not liable to pay more than the in-network cost sharing amount.

Resolve payment for surprise bills

After indemnifying the patients, comprehensive state laws then provide for resolution of the payment amount for surprise medical bills. Approaches vary, with some states adopting a payment standard for all applicable surprise medical bills, while other states establish a dispute resolution process that insurers and providers can use to arrive at a payment amount for each surprise medical bill. States sometimes use a combination of both approaches.

California’s surprise medical bill law, for example, requires state-licensed managed care plans to pay out-of-network providers the greater of 125% of the amount Medicare fee-for-service would pay, or the average contracted amount the managed care plan pays for the same/similar service in that geographic region.

New York’s law uses a binding arbitration process to resolve payment disputes. The formal process is used infrequently, however, because the law incentivizes insurers and providers to reach agreement on their own. Under the New York system, the insurer and provider first negotiate to settle the surprise medical bill. If they can’t agree, an arbitration process can be invoked; each party submits its best offer and the arbiter decides which offer wins. The losing party must pay the cost of arbitration, which typically can be $300 to $500. This so-called “baseball style arbitration” process incentivizes both plans and providers to try to resolve surprise bills informally, if at all possible. State regulators indicate most surprise bills subject to the New York law are resolved informally; New York’s formal dispute resolution process was used for 1,096 claims in 2017.

Limits to state law protections

All states have limited jurisdiction to protect privately insured residents from surprise medical bills due to the Employee Retirement Income Security Act of 1974, or ERISA. This federal law preempts state regulation of employer-provided health benefit plans. That means states are preempted from requiring employer plans to cover out-of-network surprise bills; they are also preempted from requiring these plans to apply in-network cost sharing to out-of-network surprise bills; and they are preempted from requiring these plans to settle payment disputes with out-of-network providers over surprise bills using state-established payment rules or procedures. Though ERISA allows states to regulate the group health insurance policies that some employers buy from insurance companies, 61% of covered workers (and 81% of those in large firms) are covered under self-insured group health plans that are beyond the reach of state regulation. Our estimates of surprise medical bills under large group health plans largely reflect consumers whose plans would not be subject to state law.

In addition, a number of states have enacted less comprehensive protections against surprise medical bills for the plans they regulate. Some states, for example, require only that consumers be notified by their health plan (or hospital) that they might encounter surprise medical bills, but do not impose other requirements on health plans or providers that would shield consumers from the cost of surprise medical bills. Some state laws protect consumers against surprise medical bills for emergency care, but do not apply to bills from out-of-network providers rendering care in in-network hospitals. Some state surprise bills laws apply to HMOs but not to other state-licensed insurers.

Federal legislation

Because ERISA preempts states’ abilities to regulate self-insured plans, federal action would be necessary to address certain aspects of surprise bills for people enrolled in these plans. On May 9, 2019, President Trump called on Congress to enact bipartisan legislation to end surprise medical bills. The President called for a prohibition on balance billing for all emergency care and for services from out-of-network providers that patients did not choose themselves. He also said that surprise bill protections should apply to all types of health insurance, including group and non-group.

Bi-partisan, bi-cameral support emerging

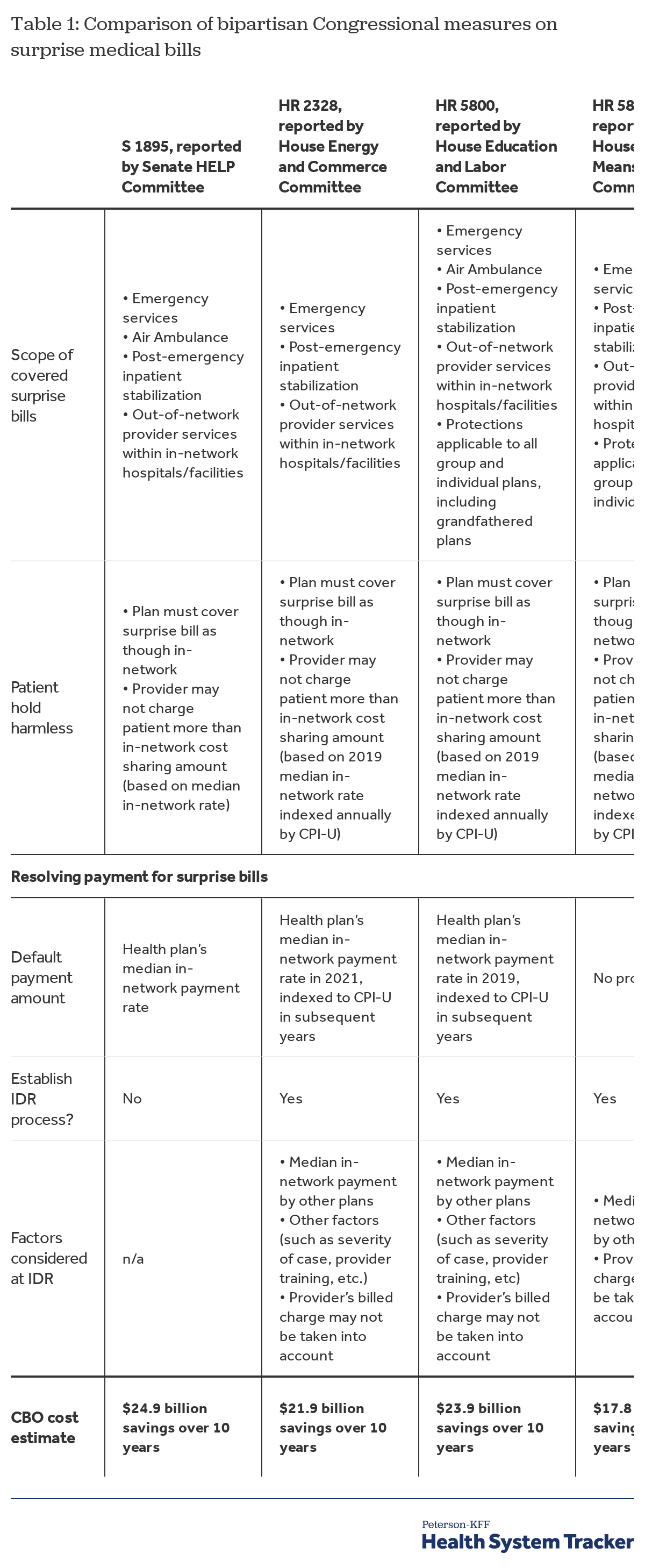

Federal legislation to prevent surprise medical bills is moving in Congress with bipartisan and bi-cameral support. In July 2019, the House Energy and Commerce Committee approved by voice vote a bipartisan bill, H.R. 2328, with provisions to prevent surprise medical bills. That month, the Senate Health Education Labor and Pension (HELP) Committee also voted on a bipartisan basis to approve S. 1895 with provisions to prevent surprise medical bills.

In February 2020, two other House Committees announced they would mark up surprise medical bill legislation that also enjoys bipartisan support in each committee. In advance of the committee votes, the House Ways and Means Committee and the House Education and Labor Committee each released discussion drafts of this legislation.

All four bills are very similar in scope of covered surprise medical bills. All would apply to out-of-network emergency claims. All would also apply to post-stabilization inpatient services provided to patients who are admitted to the hospital from the emergency room. The HELP Committee and Education and Labor Committee bills would apply to air ambulance services. In addition, the Education and Labor Committee bill authorizes the Secretary to apply surprise bill protections for ground ambulance services after receiving recommendations from an advisory committee of experts and stakeholders relating to this benefit. Finally, all of the Committee bills would cover non-emergency services provided at in-network hospitals and other facilities by out-of-network physicians and other providers.

All of the Committee bills also provide similar protections to consumers from surprise medical bills. Both would hold patients harmless by requiring health plans and insurers to cover the out-of-network surprise bill and apply the in-network level of cost sharing. Both measures would also prohibit out-of-network facilities and providers from balance billing on surprise medical bills. And both bills would apply to individual health insurance plans, as well as to group health plans, whether fully-insured or self-insured – thus reaching private plans that states are preempted from regulating.

Differing approaches to payment resolution

Still to be resolved, however, are differences in approaches to resolving payment for surprise medical bills. The Committee bills take different approaches.

Senate HELP Committee – The HELP Committee bill requires that the payment rate for out-of-network surprise medical bills will be the insurer’s median in-network payment rate for the same service in the same geographic area. The Congressional Budget Office (CBO) estimates federal budget savings of $24.9 billion over 10 years from this approach to determining payment rates for surprise bills. One key assumption in the CBO estimate is that the default payment rate for out-of-network surprise bills will have the effect of limiting rates that insurers pay for in-network services. Another key assumption is that the distribution of payment rates for surprise bills today is highly variable and skewed; setting a default payment at the median rate will have the effect of bringing down the highest in-network payment rates and generally causing payment rates for all surprise bill services to converge around the median rates. Federal deficit savings would be generated if overall insurance costs decline; this could reduce the amount of federal subsidies for private insurance through the Marketplace, the tax subsidy for employer-provided health benefits, and the amount of the medical expense deduction taken by individuals on federal income tax returns.

House Energy and Commerce Committee – The Energy and Commerce committee bill also requires a default payment rate for surprise medical bills equal to the insurer’s median in-network payment rate, and includes two additional material changes. First, the median in-network rate would be defined as the rate in 2019, indexed by inflation (CPI-U) in subsequent years. Because medical care payment rates historically have risen faster than the inflation rate, CBO estimates this indexing provision would generate greater federal budget savings. Second, the Energy and Commerce bill requires establishment of an Independent Dispute Resolution (IDR) process that providers or insurers could use if dissatisfied with the default payment and if the default payment rate is higher than $1,250. Each party would submit its payment offer to the IDR entity, which would choose the most appropriate offer. To reach this determination, the IDR entity could consider various factors – including the median in-network insurer charges, the severity of a case and the provider’s unique specialty training, but not the provider’s billed charge. Upon reaching a determination, the party whose offer was not selected would be required to pay a fee to cover the cost of IDR for that claim. CBO estimates overall savings would decline as a result of the IDR process, both due to its administrative costs and to the likelihood that payment for some surprise bills would increase above the median in-network payment rate as a result. Overall, CBO estimated the Energy and Commerce bill would yield $21.9 billion over 10 years.[iiii]

HELP and Energy and Commerce Compromise – Since these two Committees voted on legislation last summer, their leaders continued discussion and, in December of 2019 tentatively announced agreement on a compromise with respect to payment for surprise bills that both Committees could support. The compromise would follow the Energy and Commerce version, except a lower $750 threshold would apply for surprise bills to be eligible for the IDR process.

House Education and Labor Committee – Recently, the House Education and Labor Committee, with primary jurisdiction over ERISA-governed group health plans, released their proposal for surprise medical bill protection. To resolve payment amounts for surprise bills, Education and Labor follows the HELP/Energy and Commerce compromise approach. Surprise bills initially would be paid at the health plan’s median in-network rate (which would be based on the 2019 median rate indexed annually by CPI-U). Out-of-network facilities and providers not satisfied with this amount could request review under an IDR process if the median in-network payment amount is $750 or more. The IDR entity could consider the same information (and would not be allowed to consider the provider’s undiscounted billed charge) and the losing party would pay the IDR fee. CBO estimates of the impact of this proposal were not available at this writing.

House Ways and Means Committee – Finally, the House Ways and Means Committee outlined a somewhat different approach to resolving surprise medical bills. Ways and Means also would designate the plan’s median in-network rate as the amount that would be used to determine patient cost sharing for the surprise out-of-network bill. Like the Energy and Commerce bill, Ways and Means would constrain the median-in-network rate, basing it on the 2019 rate indexed annually by CPI-U. This median rate would be re-based every five years.

The Ways and Means proposal does not require use of this benchmark rate to determine initial payment for the claim, however. Instead, Ways and Means would require negotiations between health plans and providers to reach an agreed-upon payment amount for each surprise bill. At the end of 30 days of negotiation, either party could request review under an IDR process. No claims dollar threshold amount would apply. The IDR process would otherwise generally follow rules as prescribed in the Energy and Commerce bill. That is, the IDR entity would consider each party’s offer, taking into account the median in-network charge but not the provider’s billed charge. The IDR entity would then select one offer and the losing party would pay the IDR fee. CBO estimates of the impact of the Ways and Means proposal were not available at this writing.

Importantly for the consumer, under all of the Committee bills, the amount of patient cost sharing for the surprise medical bill is determined up front, based on the health plan’s initial in-network payment rate for the service. That means if the out-of-network provider subsequently seeks and wins a higher payment amount through negotiations or the IDR process, the patient’s cost sharing for the surprise medical bill claim would not be increased.

Roe-Ruiz bill – Notably, all four of these Committee bills are materially different from an altogether different approach to resolving payment for surprise medical bills outlined in yet another with bipartisan support, HR 3502, sponsored by Rep. Ruiz (D-CA) and Rep. Roe (R-TN). No default payment amount would be established for surprise medical bills under this measure. Instead, insurers and providers would first engage in negotiations over the payment amount for each surprise medical bill. If no agreement is reached, the dispute would be taken to an IDR process that would take into account both the median-in-network payment rate and the 80th percentile of actual billed charges. Although no formal CBO estimate on this bill has yet been published, one news report indicates CBO would find it would cost “double digit billions” of dollars in increased federal spending over the next 10 years.

Table 1 compares key provisions of the four Committee measures and HR 3502 and their resulting cost impact on the federal government.

Finally, several of the committee measures include other provisions to protect consumers and promote transparency. All four Committee measures require health plans to periodically update their provider directories for accuracy. The Ways and Means Committee bill requires plans to follow continuity of care requirements, giving patients in-network level of temporary (up to 90 days) coverage for care when their in-network provider leaves the health plan network while treatment is ongoing. The Ways and Means Committee bill also requires that ACA external appeal protections apply to enrollees who dispute the way their plan handled surprise medical bills. Under Obama Administration regulations published in 2011, ACA external appeal rights under most plans only apply to claims denied or limited on the basis of medical necessity determinations and related clinical-judgement determinations.

Discussion

We find that millions of emergency visits and hospital stays left people with large employer coverage at risk of a surprise bill in 2017. Our analysis of large employer health plan claims finds that potential surprise medical bills are a common problem – affecting 18% of emergency care visits and 16% of in-network inpatient stays. The rate of these potential surprise bills varies from state-to-state, with Texas, New York, Florida, New Jersey, and Kansas having among the highest rates of out-of-network charges associated with both emergency care and in-network hospital stays among people with large employer coverage. Minnesota, South Dakota, Nebraska, Maine, and Mississippi, by contrast, had among the lowest rates of out-of-network charges for both emergency and in-network hospital care for people with large employer coverage. The incidence of surprise medical bills in small group or non-group health plans may be different and was beyond the scope of this study.

By definition surprise bills are beyond the ability of consumers to anticipate or avoid; and surprise bills generate expenses that health insurance does not cover and that can be financially burdensome to patients. States have started taking action – establishing requirements for both the health plans and the providers they regulate in order to shield consumers from surprise medical bills. However, ERISA preemption means state laws cannot reach the vast majority of consumers with private coverage through employer-based plans. The high rates of surprise medical bills that we observe in California and New York, which have adopted comprehensive state statutes, demonstrate the limits of state regulation of surprise bills.

National consensus on surprise medical bill protections seems to be emerging. There is strong bipartisan support among the public to address surprise bills. Members of Congress are working in a bipartisan manner to develop legislation and the President has urged enactment of a federal law to protect patients from surprise medical bills. The insurance industry, employer organizations, and hospital and physician groups have also urged measures to protect patients from surprise medical bills.

However, how much providers should be paid for surprise medical bills remains a contentious issue that, unless resolved, could derail patient protections.

In particular, health insurers and employer groups have recommended a federal payment standard as a less complex and costly approach to resolving millions of surprise medical bills each year. On the other side, hospital and physician groups have urged reliance on negotiation or mediation to resolve surprise bills, and generally opposed use of a fixed payment standard. They argue a fixed payment standard might not be sufficient, might incentivize insurers to rely on default payments rather than contract with providers to join networks, and might lead to broader federal rate setting for provider payments. This summer, an organization called “Doctor Patient Unity,” backed by venture capital owners of physician group practices and freestanding emergency departments, invested millions of dollars in television ads opposing surprise billing legislation.

Estimates from CBO illustrate that a surprise bill payment standard based on median in-network rates would, in fact, put downward pressure on provider payments. Conversely, a system based on mediation could increase payment rates. Since the federal government subsidizes private insurance through the ACA marketplace and in employer-based plans, this has significant implications for the federal budget as well.

It remains to be seen whether disagreement over how to resolve payment amounts for surprise bills can be resolved, or if it will halt progress on legislation to protect consumers from these bills.

Appendix

Methods

We analyzed a sample of medical claims obtained from the 2017 IBM Health Analytics MarketScan Commercial Claims and Encounters Database, which contains claims information provided by large employer plans. We only included claims for people under the age of 65. This analysis used claims for almost 19 million people representing about 22% of the 86 million people in the large group market in 2017. Weights were applied to match counts in the Current Population Survey for enrollees at firms of a thousand or more workers by sex, age, state and whether the enrollee was a policy holder or dependent. Weights were trimmed at eight times the interquartile range.

The advantage of using claims information to look at out-of-pocket spending is that we can look beyond plan provisions and focus on actual payment liabilities incurred by enrollees. A limitation of these data is that they reflect cost sharing incurred under the benefit plan and do not include balance-billing payments that beneficiaries may make to health care providers for out-of-network services or out-of-pocket payments for non-covered services.

Inpatient claims were aggregated by admission and outpatient claims were aggregated by the day (‘outpatient days’). Each claim on the inpatient and outpatient services files has a variable (‘ntwkprov’) that indicates whether or not the provider or facility providing the service was in the health plan’s network.

We defined an emergency room visit as an outpatient day or admission that included at least one claim in the emergency room (as defined by “stdplac”). Some admissions may include an emergency room claim, and an out-of-network service that took place outside of the emergency room. In total, there were 15 million ER visits, six percent of which were associated with an inpatient admission.

In-network admissions were defined as admissions that included an in-network room and board charges. Some in-network admissions may include out-of-network facility charges. In total, there were about 3.5 million in-network admissions. Data are not presented for states with fewer than 3,000 unweighted emergency room visits or 500 in-network admissions or where an insufficient number of data contributors submitted information.

Endnotes

[i] Federal regulations require health plans to pay the greater of 3 amounts for out-of-network emergency services (net of the applicable in-network cost sharing): (1) the amount negotiated with in-network providers for the emergency service; (2) the amount the plan typically pays for out-of-network services (such as the usual, customary, and reasonable charge); or (3) the amount that would be paid under Medicare for the emergency service.

[ii] Section 2719A of the Public Health Service Act defines emergency services in the same way as the federal Emergency Medical treatment and Labor Act of 1986 (EMTALA). However, the application of EMTALA to patients admitted as inpatients from the emergency room has been disputed and litigated. Federal courts have taken different views as to a hospital’s “stabilization obligation” under EMTALA when it comes to inpatients. See, for example, https://www.everycrsreport.com/files/20101228_RS22738_a6cc21b68c20d1982533d6249774e019179ef6a5.pdf

[iii] See Jack Hoadley, Kevin Lucia, and Maanasa Kona, “State Efforts to Protect Consumers from Balance Billing” for summary of state laws enacted through 2018. In the 2019 legislative session, New Mexico enacted a new law protecting residents from surprise medical bills, both for emergency and non-emergency services, under state-regulated health insurance. The law takes effect January 1, 2020. It requires state-regulated health plans to provide in-network level of coverage for surprise medical bills and prohibits providers form balance billing patients. The law also provides that surprise out-of-network bills will be paid at the 60th percentile of the insurer’s allowed charge for the service performed by an in-network provider, but no less than 150% of the applicable 2017 Medicare payment rate. The state of Washington also enacted a surprise medical bill law in 2019. Similar to the New Mexico law, Washington requires state-regulated plans to cover surprise medical bills for both emergency and nonemergency services at the in-network level of cost sharing and prohibits providers from balance billing patients. The Washington law establishes a mediation process that health plans and providers must use to resolve the amount of each surprise medical bill if the plan and providers cannot successfully negotiate an amount on their own. Colorado’s new law also becomes effective January 1, 2020. It applies to emergency and non-emergency surprise bills, requiring state-regulated health plans to provide in-network level of coverage for such bills and prohibiting provider balance billing. The law establishes payment rate benchmarks for surprise bills, based on the health plan’s payment rate for comparable in-network providers or based on a measure of the in-network payment rates by all plans in the state’s all-payer-claims database. Out-of-network providers can appeal these payment rates to a mediation system in certain circumstances. Finally, a new law enacted in Texas will apply to surprise medical bills beginning January 1, 2020. The Texas law requires state-regulated plans, including state employee and teacher plans, to cover surprise medical bills for both emergency and nonemergency services, including diagnostic lab and imaging services ordered by an in-network physician. Plans must cover out-of-network surprise bills with in-network level of cost sharing and providers are prohibited from balance billing patients. Texas requires plans to make an initial direct payment to the out-of-network provider for the surprise bill. The provider can then request an independent dispute resolution process. For hospitals and other facilities, this is a mandatory mediation process that the facility and insurer must use to resolve the amount of the surprise bill. If agreement cannot be reached, either party can bring a civil action in court. For other providers, Texas will make a mandatory arbitration process available. The arbitrator will make a binding determination of the payment amount for the surprise bill. A mandatory informal settlement conference is required before either mediation or arbitration begins. Under both processes, the fees for mediation or arbitration must be split evenly between the health plan and the facility/provider.

[iiii] The other bi-partisan Senate bill, S 1531, is similar to the Energy and Commerce Committee bill in terms of the scope of covered surprise bills and the hold harmless patient protections it would require. To resolve payment for surprise bills, S. 1531 would establish a default payment rate for surprise bills equal to the insurer’s median in-network payment rate, but would not index that payment rate to inflation. S. 1531 also would establish a similar IDR process that would take into account the median in-network payment and other factors, but not the provider’s billed charge. S 1531 does not set a claims threshold to limit eligibility of surprise bills for the IDR process. Under both S 1531 and the House Energy and Commerce reported bill – and similar to New York State’s IDR process for resolving surprise bills, the losing party would pay the cost of the IDR process. CBO has not published a cost estimate for S 1531.

The Peterson Center on Healthcare and KFF are partnering to monitor how well the U.S. healthcare system is performing in terms of quality and cost.